Business Borrowing in Canada Is Getting Harder

1 | What's happening with global private credit

A decade of breakneck growth in private credit has given way to a wave of investor withdrawals, and several of the world's largest funds have limited redemptions to cope.

2 | How it affects Canada

Canadian investors are pulling back in the same way, and several domestic funds have already gated, tightening access to non-bank lending right as the economy needs risk capital to flow.

3 | Impact on borrowing

Volatility is making capital harder to access across the board, banks and private lenders alike.

- Fewer approvals— fewer dollars going out the door

- Lower risk appetite — safer bets only

- Stricter criteria — more proof required

- Higher rates — risk gets priced up

- Tougher terms — more covenants, more security

- Harder renewals — rollovers no longer automatic

- Strict enforcement — faster and more aggressive response to covenant breaches

4 | What you can do about it

"Accessing capital will be harder than it's been in years, so being prepared rather than reactive is your best chance of securing a loan."

1. Evaluate your capital stack

Review your debt ratios and current capital structure with your CFO or advisor

2. Identify your operational risks

The ones that put new financing or existing lines at risk.

3. Align capital with strategy

Make sure your plan is one you can actually finance

4. Get your advisors involved

Organize your financials, line up legal, share your plan and listen to

5. Start before you need it

Model what you need, the structure you can carry, and what the market will bear.

6. Address breaches before they happen

Talk to your existing lenders early.

The Debt Digest lands in your inbox each month.

What is private Credit?

Private credit is lending that comes from outside the conventional banking system. The money is raised largely from institutions and wealthy investors, pooled into funds that lend to businesses over multi-year horizons. It has grown over the past decade into one of the most important sources of capital in the economy, alongside banks and reaching companies the banks can't.

Why it matters.

Lending runs on a simple trade between risk and rate. Banks sit at the low end, offering the cheapest money because they lend under strict criteria and a narrow mandate, which leaves many capable companies on the outside. Private credit fills the space above them, funding higher-risk ventures, fast growers, and turnarounds that banks pass on, and charging higher rates to match the added risk.

Why is it in the news?

The investors behind these funds are typically promised the ability to withdraw their money long before the loans come due, and that mismatch is the problem. A run of unsettling economic news this year, slowing growth, sticky inflation, trade and tariff tension, the impacts of AI, and rising doubts about whether private credit had simply grown too fast, pushed investors to pull their capital back. The funds couldn't sell multi-year loans fast enough to meet the requests, so several of the largest funds restricted withdrawals to protect themselves, and the loss of confidence that followed now reaches well beyond the funds themselves.

GLOBAL INSTITUTIONAL PRIVATE CREDIT GROWTH

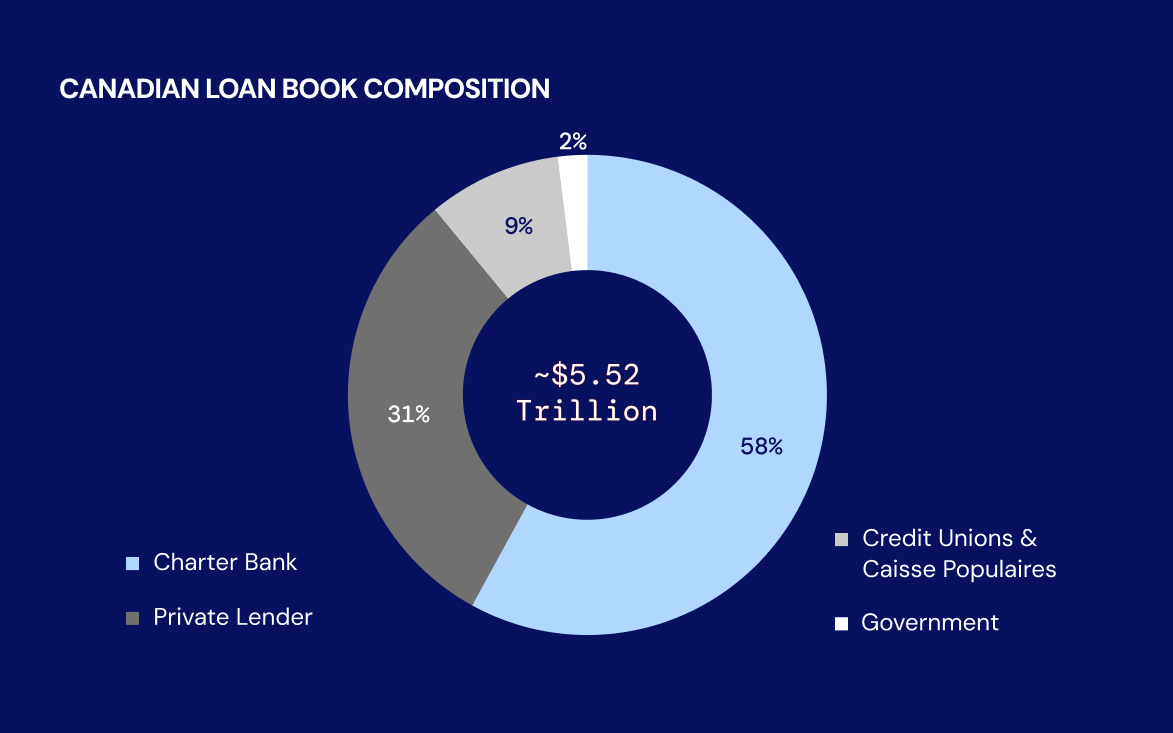

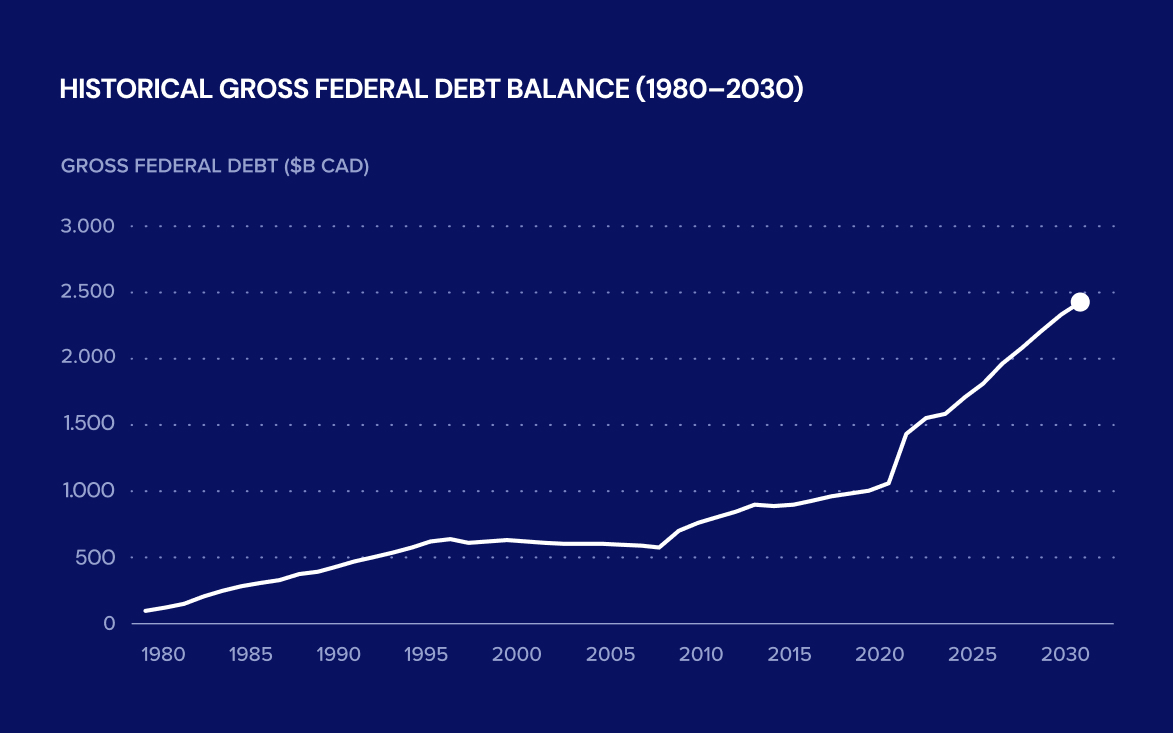

How it affects the Canadian economy

Canada's exposure runs through real estate rather than through corporate and software lending, which dominate the US. Real estate accounts for 51% of our entire credit market, and private credit is woven deep into it, so the same global pressures arrive here through a more concentrated door. Several Canadian funds have limited redemptions, returning, on average, 5.8% less than investors requested.

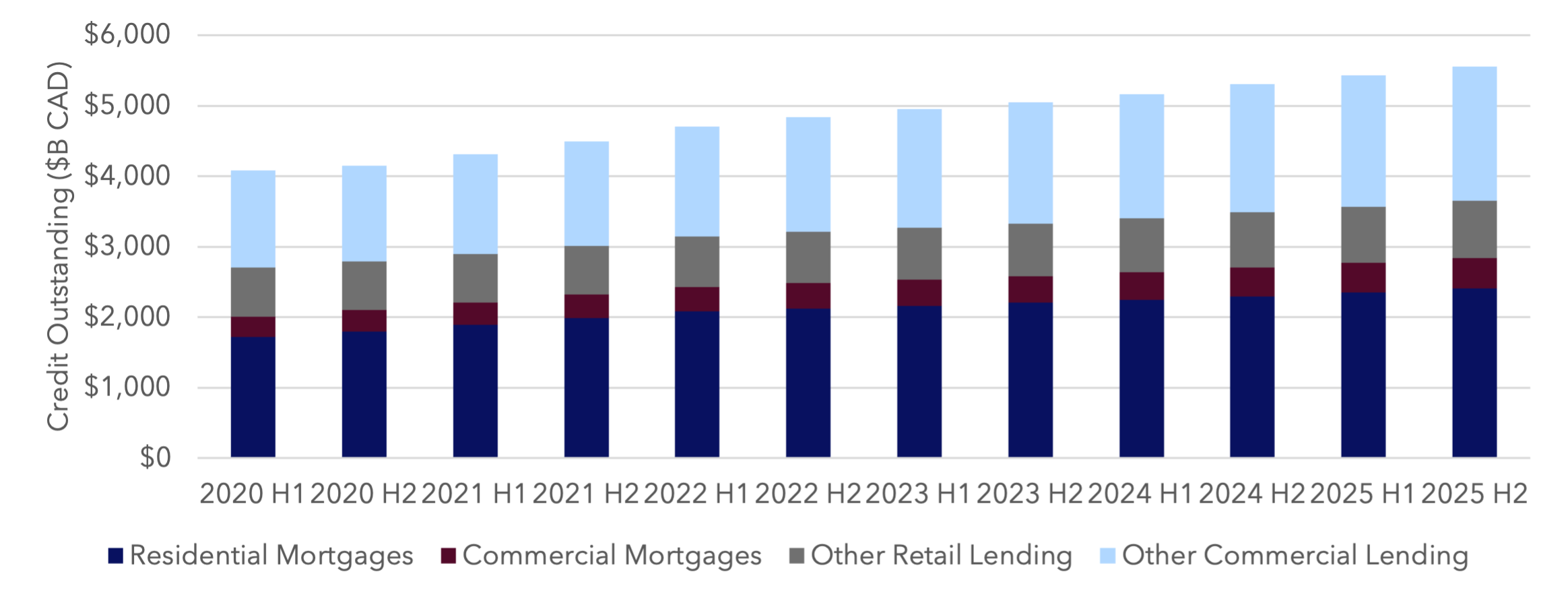

CANADIAN CREDIT MARKET COMPOSITION

This system matters more to Canada than most people realize. It's how companies fund new projects and buy businesses from a retiring generation of owners, and it's often how a company proves itself before a bank will step in.

Once that performance is established, the bank refinances at a lower rate, and that move down the cost curve is where real growth takes hold. Remove the private credit that makes the first step possible, and the whole chain that carries a business from ambition to stability comes apart.

Which sectors will be hit hardest?

Real estate and construction

They depend most on private capital, since banks tend to fund only the late, lower-risk stage of a project. Canadian private credit is concentrated here, which is exactly where redemption pressure is building.

Technology

These companies borrow against recurring revenue, not hard assets. With US private credit heavily exposed to software and AI reshaping the sector, lenders are scrutinizing these stories most closely.

Energy, manufacturing, and agriculture

All three run on financing and thin margins, so they feel a cautious market quickly, especially where they already rely on private lenders.

What this means for your business

Accessing new debt

- Lending criteria are tighter across the board.

- Bank financing is harder to secure, even though banks have room to lend.

- Private capital is more selective about the stories it will back.

- Lender options are thinner, especially in higher-risk industries.

- Expect higher rates, tougher terms, and more of your own equity in the deal.

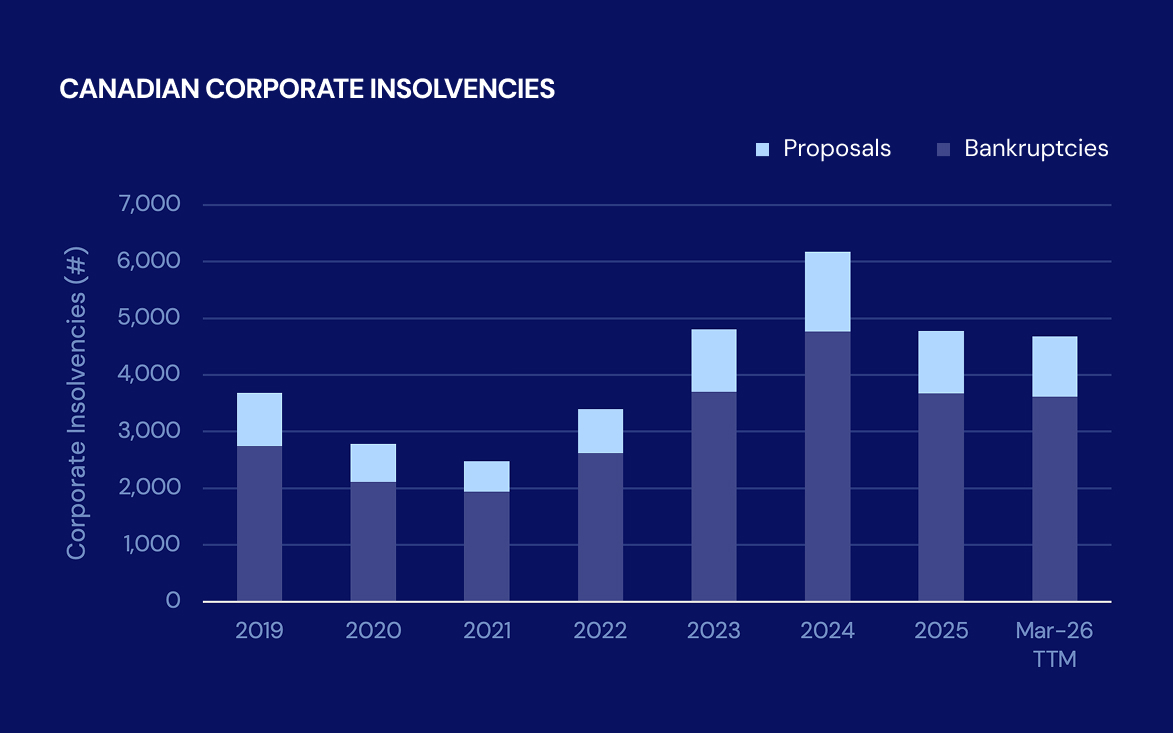

Managing existing loans

- Lenders have less tolerance for a miss than they did a year ago.

- More facilities are being called or not renewed.

- Lenders are quicker to enforce their rights when a loan goes offside.

- More struggling borrowers are ending up in forced restructurings or insolvency.

Actionable Intelligence

1. Identify your exposure

Know the signals a lender will act on before they raise them with you.

- A renewal or maturity within the next 12 to 18 months

- A fully drawn or overdrawn operating line

- Debt above four times EBITDA, or coverage slipping below 1.25

- A single lender relationship with no backup

- Customer, supplier, or sector concentration that a cautious lender will flag

2. Understand your options

Find out what the market will actually offer you now, while you still have room to negotiate.

- Talk to your advisors and model a few scenarios against today's terms

- Learn the structure that your cash flow can realistically carry

- Line up financing ahead of the need, not at the deadline

- Get ahead of a covenant breach by talking to your lender early

- Keep more than one lender in play, so no single relationship controls you

3. Adjust your strategy

A tighter market changes what your plan can support, so pressure-test it before you raise, not during.

- Align the capital plan with what the business can actually execute

- Sequence growth so each step is fundable on its own

- Cut or fix the parts of the business that weaken the story

- Build the performance record now that a lender will want to see later

Nish Sampath

Nish runs Switch Advisory, a fractional COO firm that helps mid-market companies turn a strategy on paper into one the business can actually execute. We asked him what a seasoned COO tells a CEO heading into a market like this, and his answer comes down to execution and what it earns you.

"You have to get the whole organization aligned long before you go looking for capital. Your three-to-five-year objectives, your strategic plan, what each department is accountable for, and the reporting that connects it all have to point the same way, and you need real visibility into the numbers that matter. That's what keeps you on a performance track, and staying on that track is what keeps your financing options open when you need them for growth, an acquisition, or a restructuring.

The reason it pays off comes down to cost. If you're carrying higher-rate private credit, the sooner you prove you can execute, the sooner you can refinance at a lower rate, so hitting your numbers early brings costs down. And if you're funded at a bank, staying in good standing through a rough stretch protects your continuity and keeps you clear of the disruptions that catch unprepared operators off guard. A forecast gets you a conversation. A track record is what a lender actually lends against."

What lenders don’t tell you.

1. Structure matters

A decline is usually about fit, not the quality of your business, so one lender's no is not the market's answer.

2. What kills a deal

Thin or late financials, surprises in diligence, and a single-lender approach with no competition to keep them honest.

3. What gets approved

A clean, prepared file, a forecast backed by a track record, and the right lender matched to your story.

4. How to optimize terms

Run a competitive process and match the structure to your cash flow, so you keep the option to move back to a bank later.

Grant Daunheimer

"The road ahead is tough for an economy already struggling, and credit is harder to find. Execution is the one thing fully inside your control, and right now, it is the single most important thing you can show a lender.

If you advise business owners, this is the moment to be in front of them. Share this with the clients who need to see it, and have an honest conversation about the risk ahead before it becomes urgent. The earlier they prepare, the more options they keep, and the more useful you are to them when it counts."

Forward this to someone who needs it, and start the conversation.

The Debt Digest lands in your inbox each month.