2025 Canadian Bank Loan Book Analysis

2025 was a banner year for the Canadian Big 6 Banks, who all posted solid loan growth with stable credit profiles. Despite strong performance, real estate continues to dominate loan books, presenting a material risk and reinforcing the need for greater diversification. This note breaks down those loan books by sector which hopefully ties to your business’ financing requirements and the estimated $110 billion of investment Canada expects over the next decade. We see increased opportunities for both traditional lenders and alternative credit to deploy capital across a broader range of sectors.

Key Takeaways this Month:

- Lots And Lots Of Real Estate: Banks hold $2.3 trillion of the $3 trillion in Canadian real estate exposure. This highlights a critical concentration risk and makes the case for greater lending diversification.

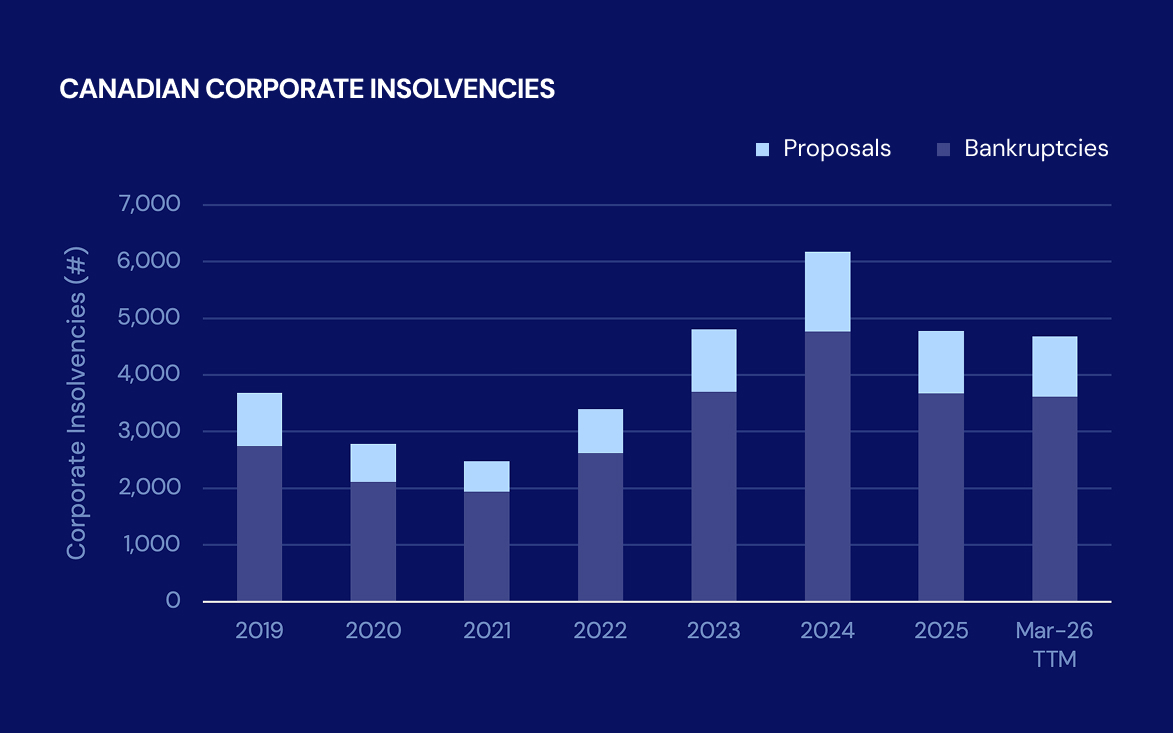

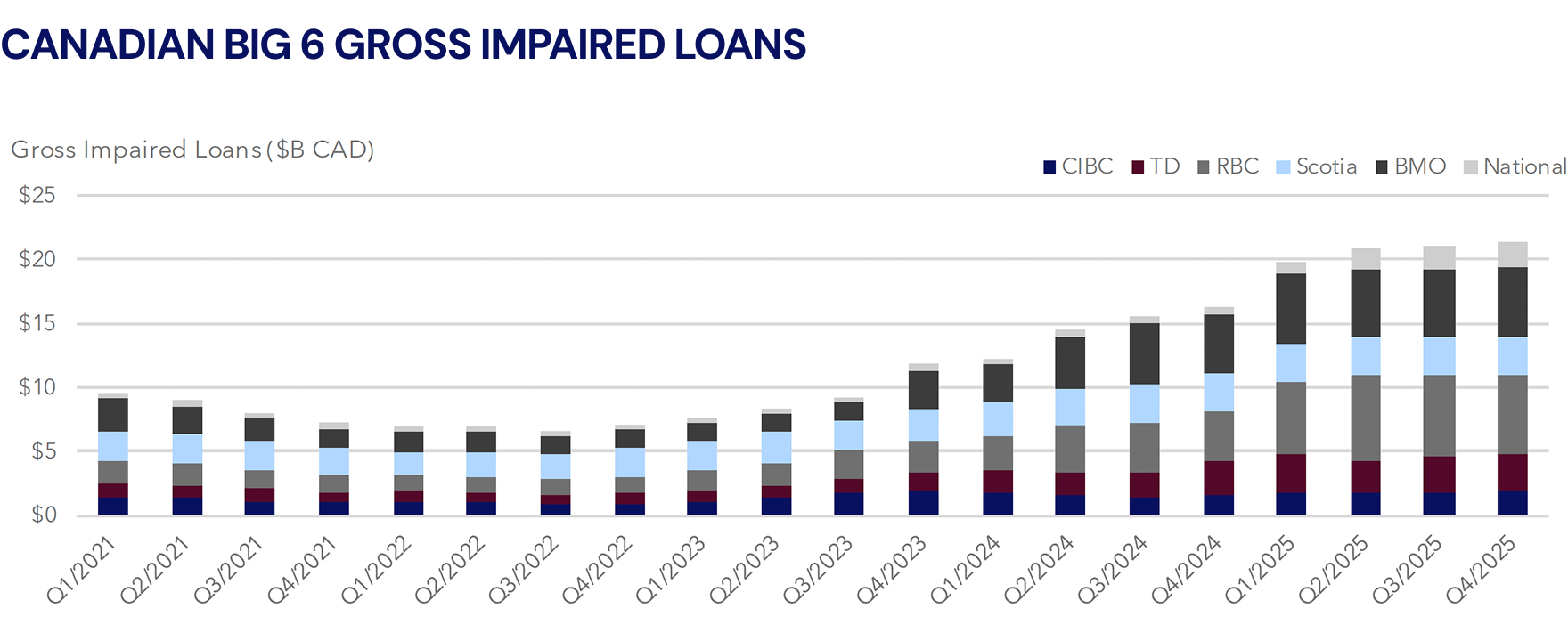

- The Big 6 Delivered Big Results: Canada’s Big 6 Banks grew their loan book by 4.1% in 2025. Impaired loans however are at elevated levels which we expect will keep special loans and insolvency professionals busy in 2026.

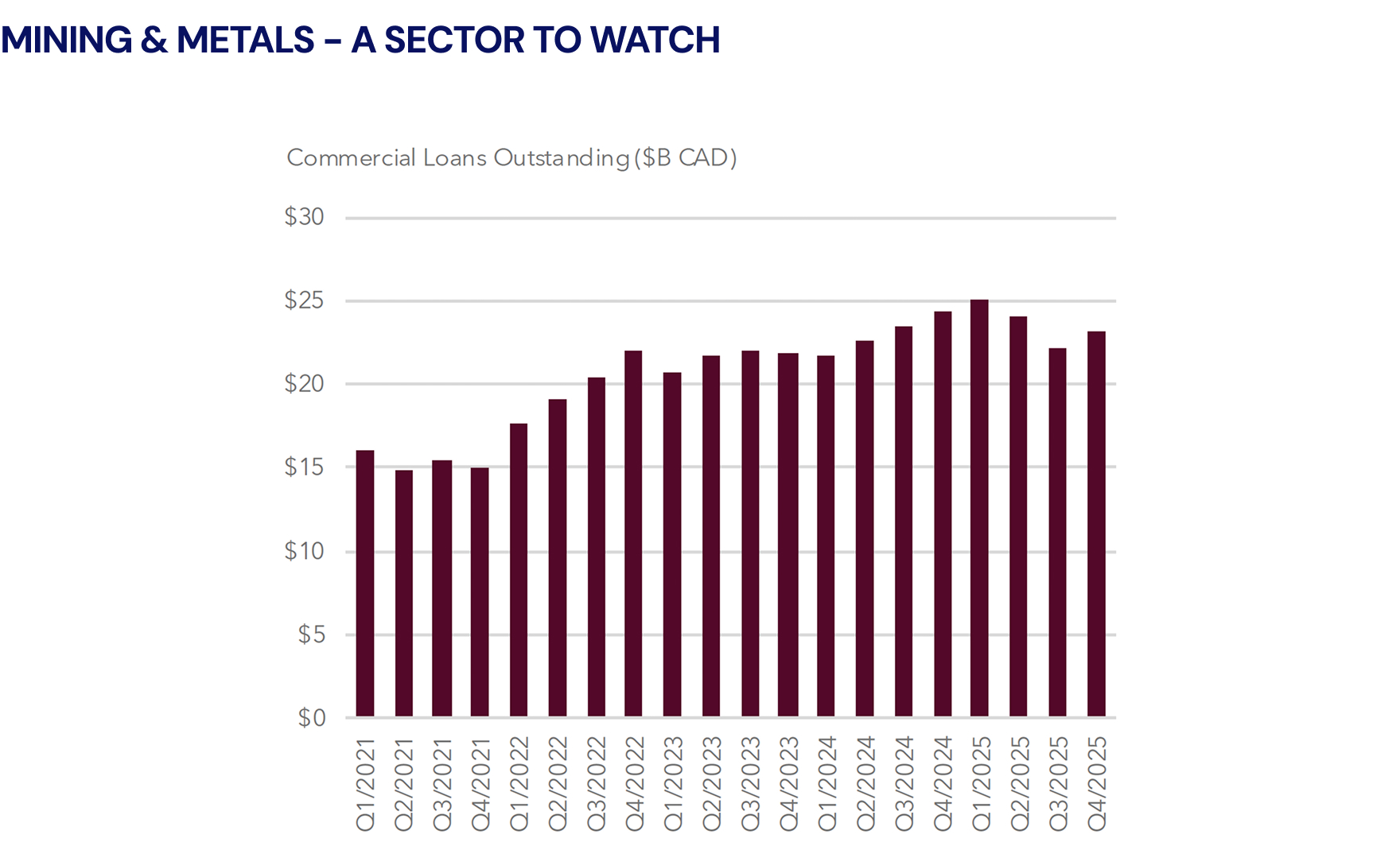

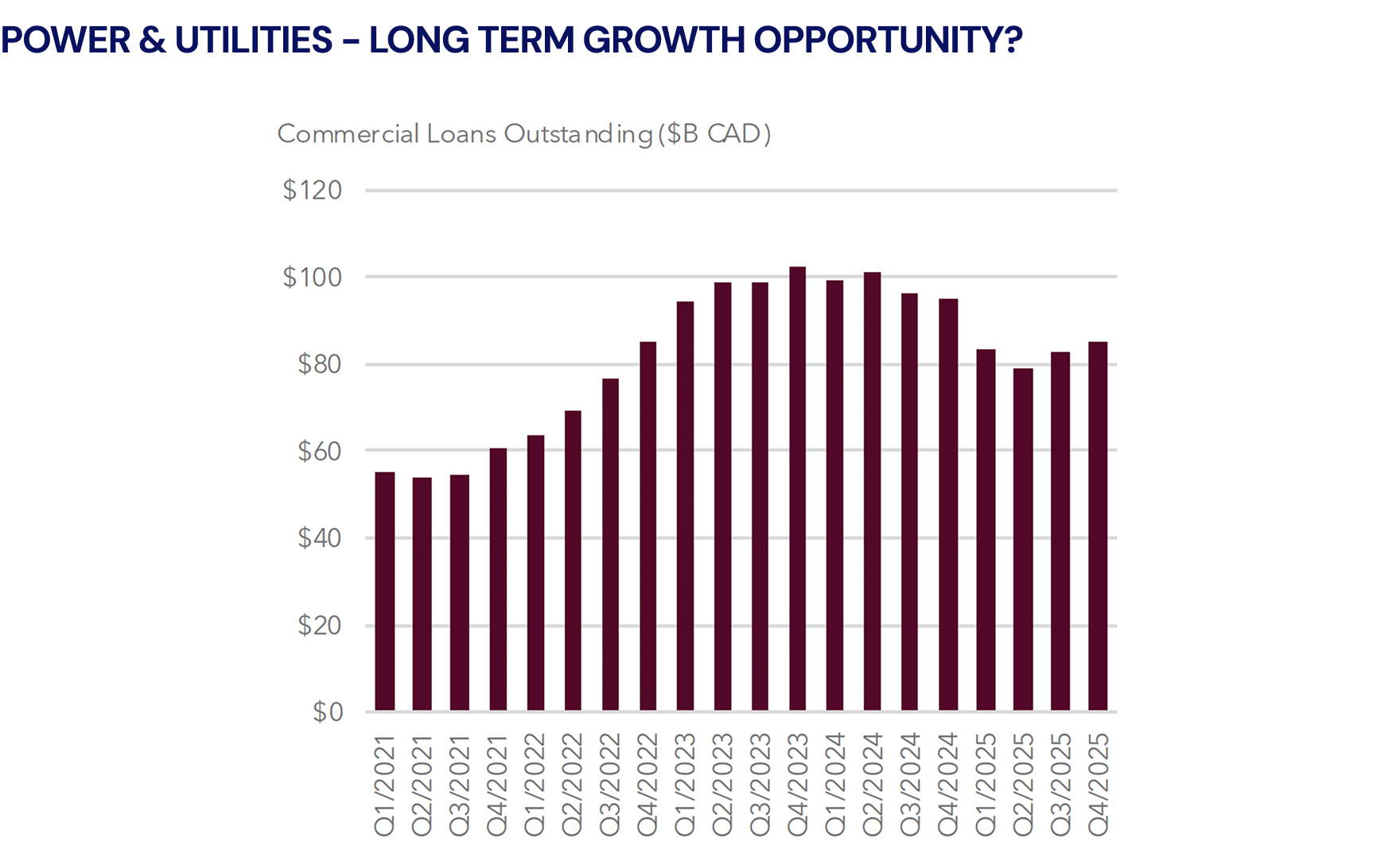

- Sectors To Watch Going Into 2026: Recent announcements from the Major Projects Office have allocated $110 billion to various sectors, including power, mining and industrials. We expect there will be opportunities for private capital as Banks have trimmed their sector exposure.

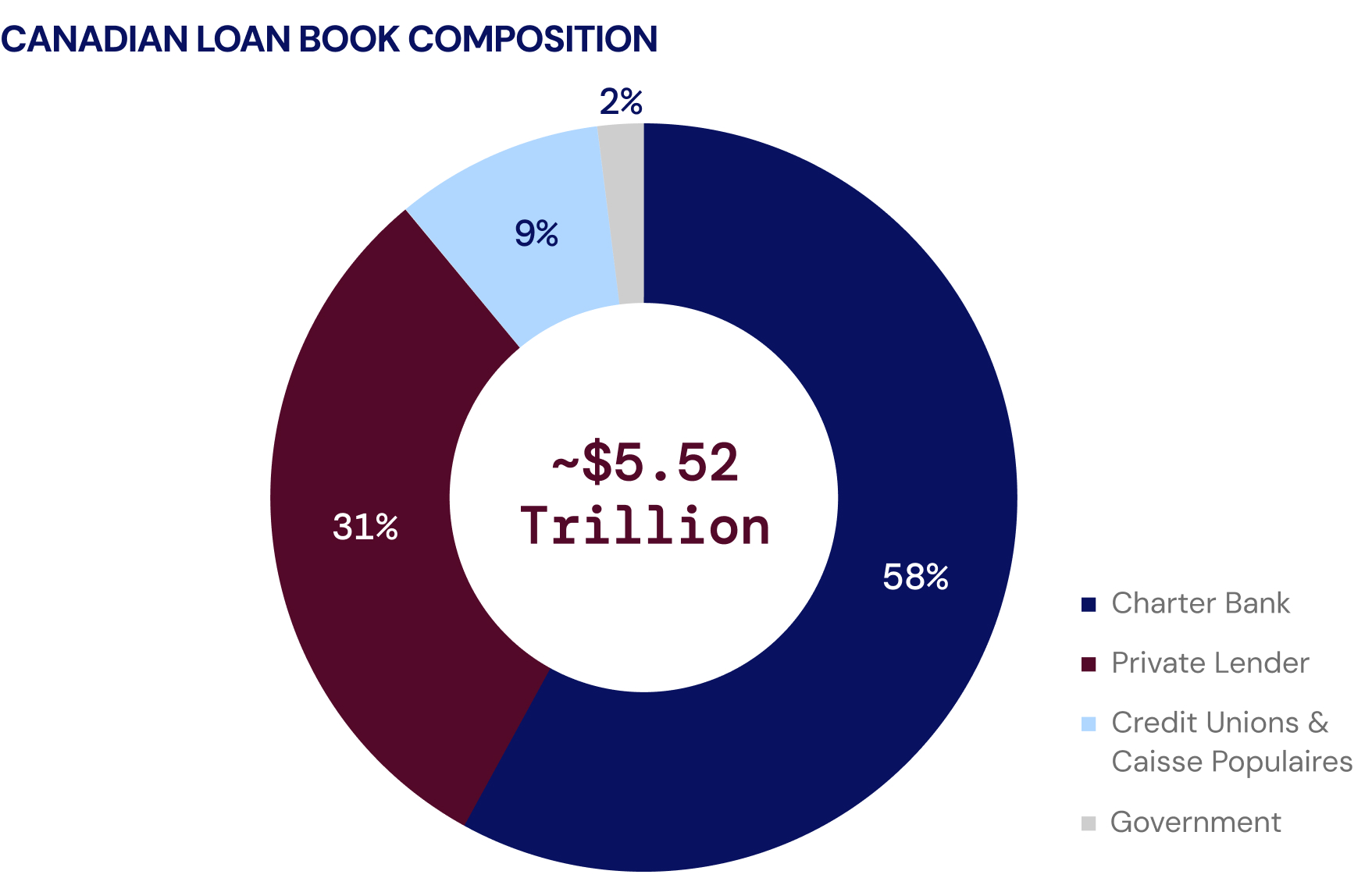

Of the $5.5 trillion in outstanding credit in Canada, 58% are on the balance sheets of chartered banks. These chartered banks hold ~$2.3 trillion of real estate, highlighting a material concentration risk and making the case for greater diversification in lending exposure.

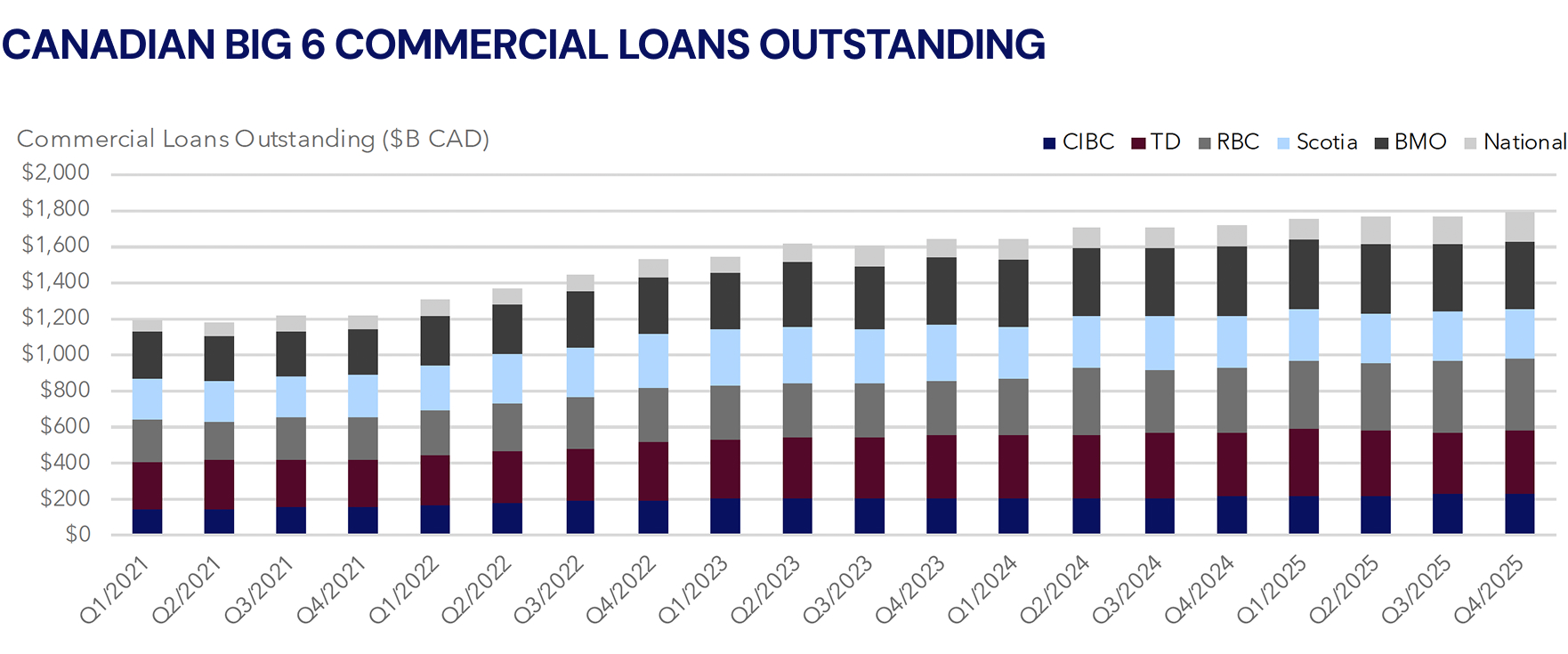

Led by solid loan growth (4.3%YoY), Canada’s big banks closed out 2025 with strong earnings beats and rising profits across the board

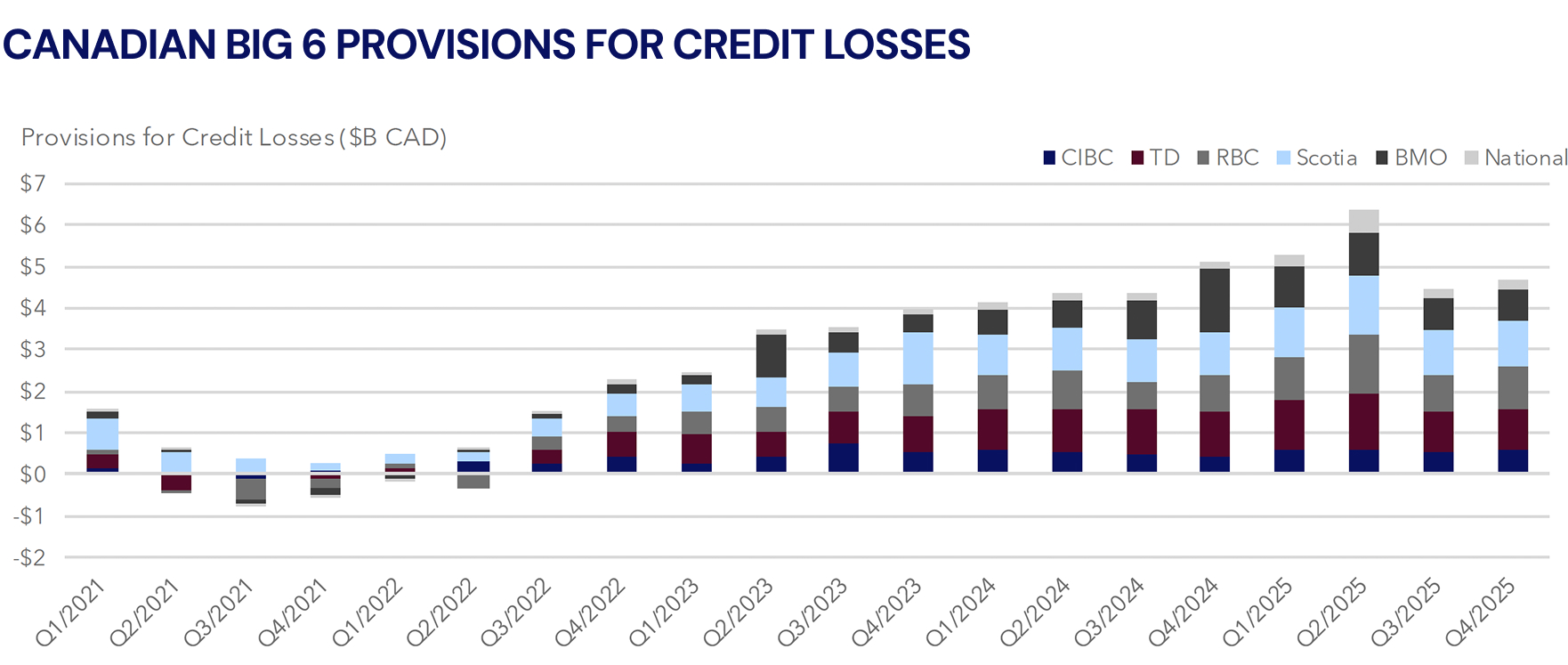

Special Loans & Insolvency groups should be busy in 2026 – Gross Impaired Loans grew materially in 2025 and now represent 1.2% of all commercial loans outstanding (vs. 0.7% historical average)

Provisions for Credit Losses grew at a modest 5.3% QoQ in Q4/2025 and currently represents 0.3% of all commercial loans outstanding (which is in line with the 0.2% historical average)

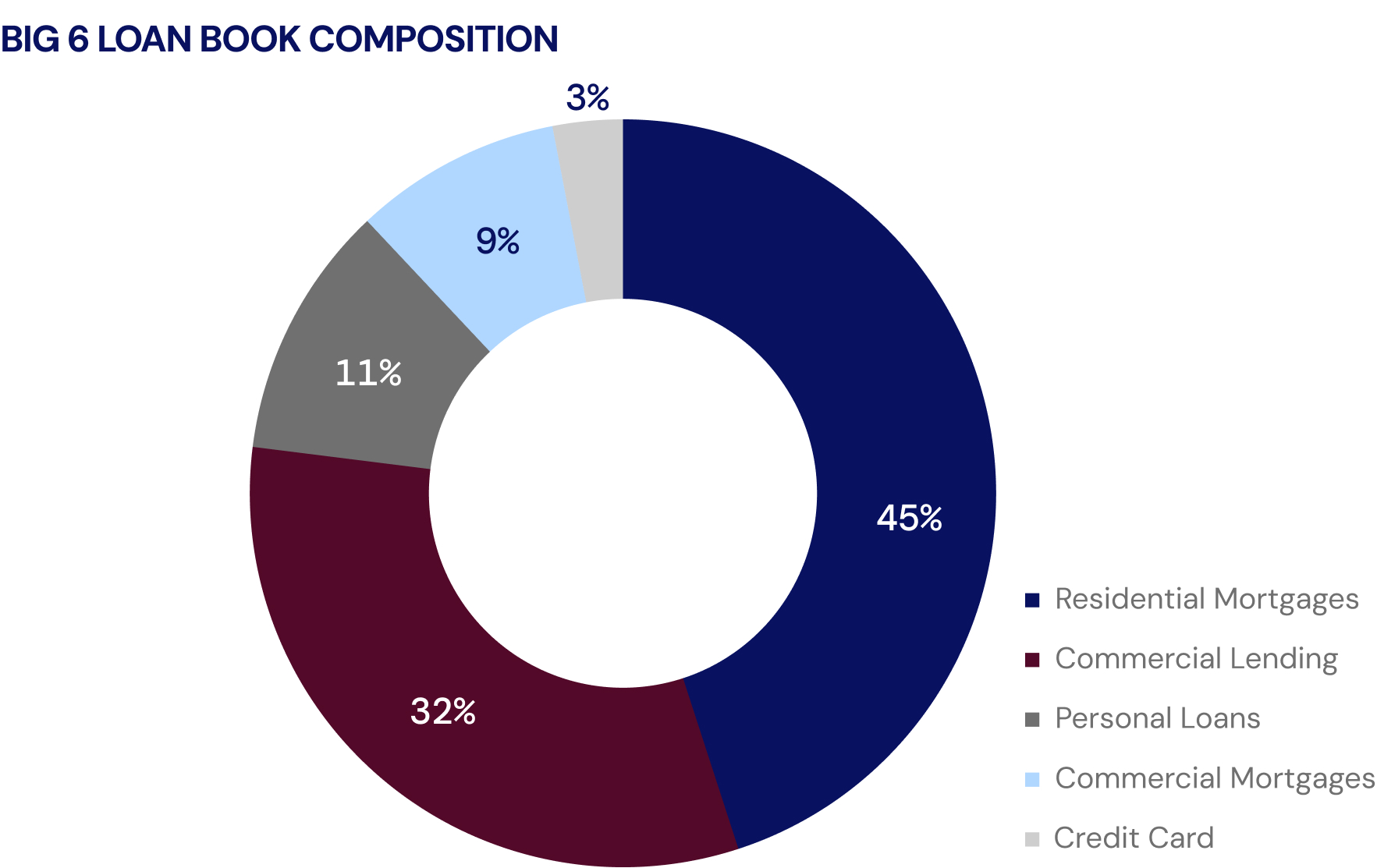

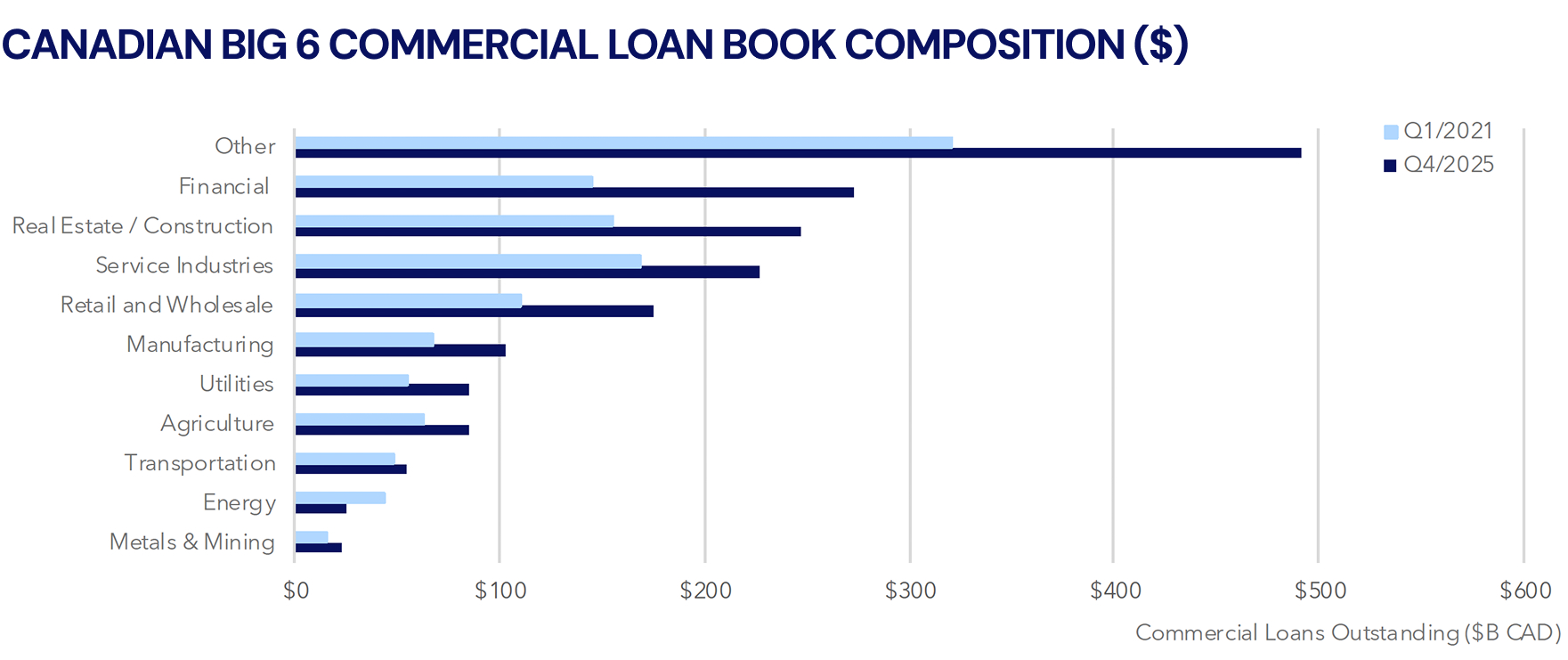

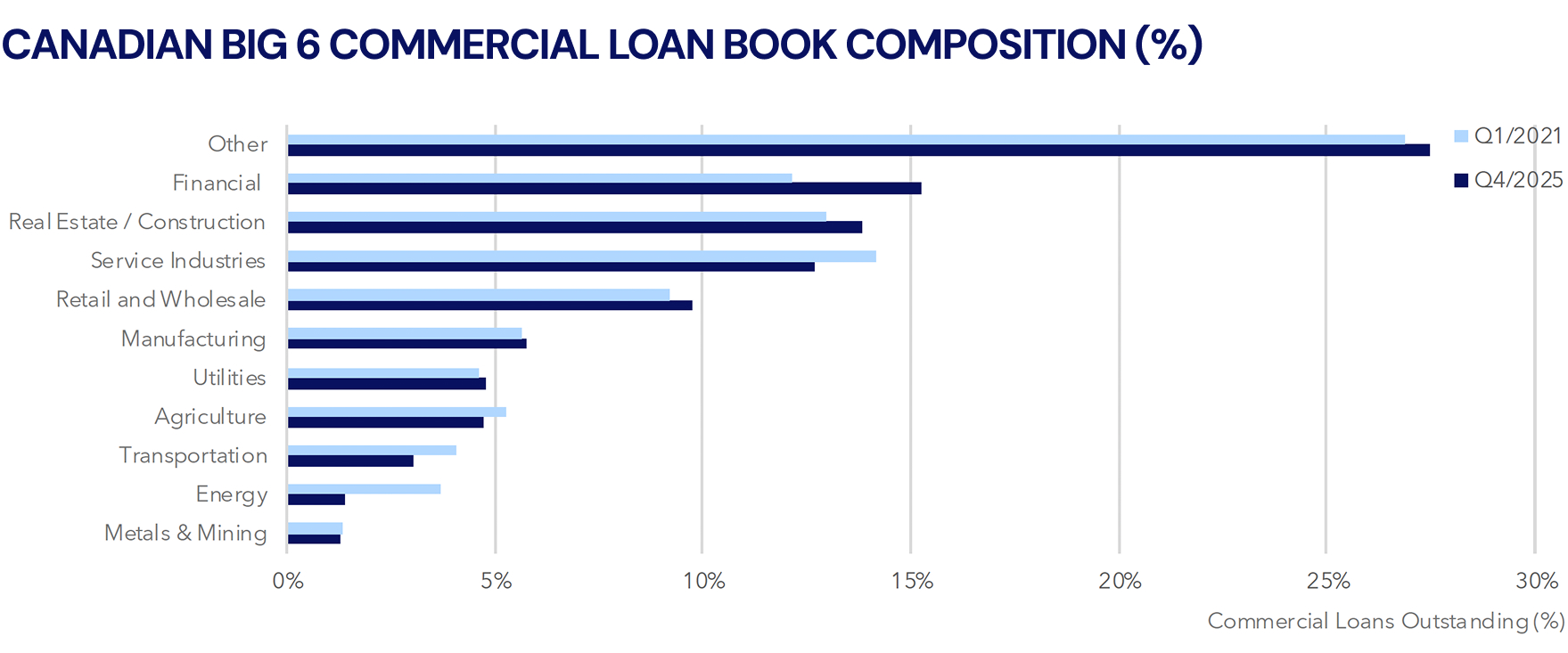

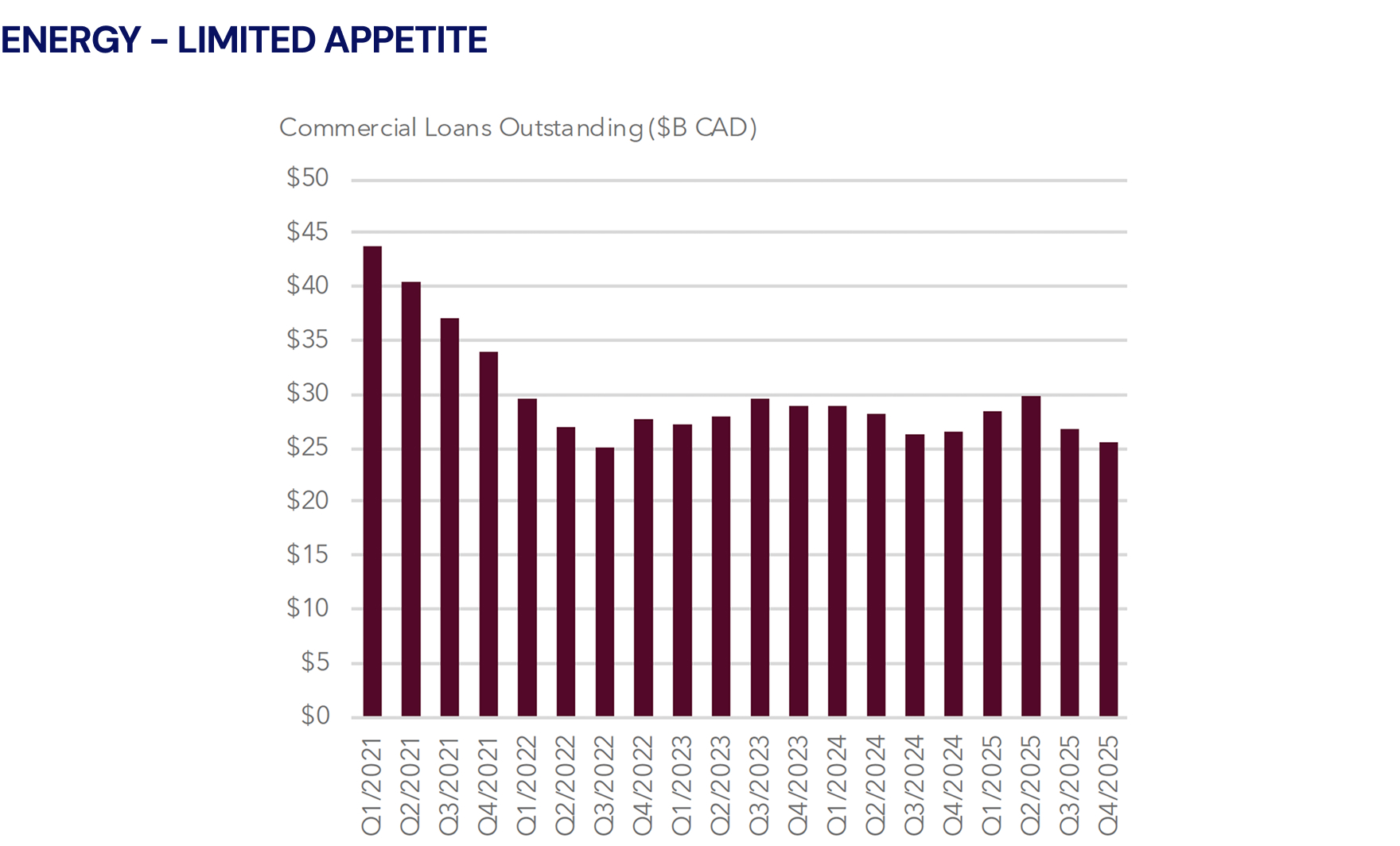

Big 6 lending has shifted toward Financial and Real Estate/Construction, now 29% of overall loan books (vs. 25% in Q1/2021), while Energy exposure has fallen to 1% (vs. 4% in Q1/2021)

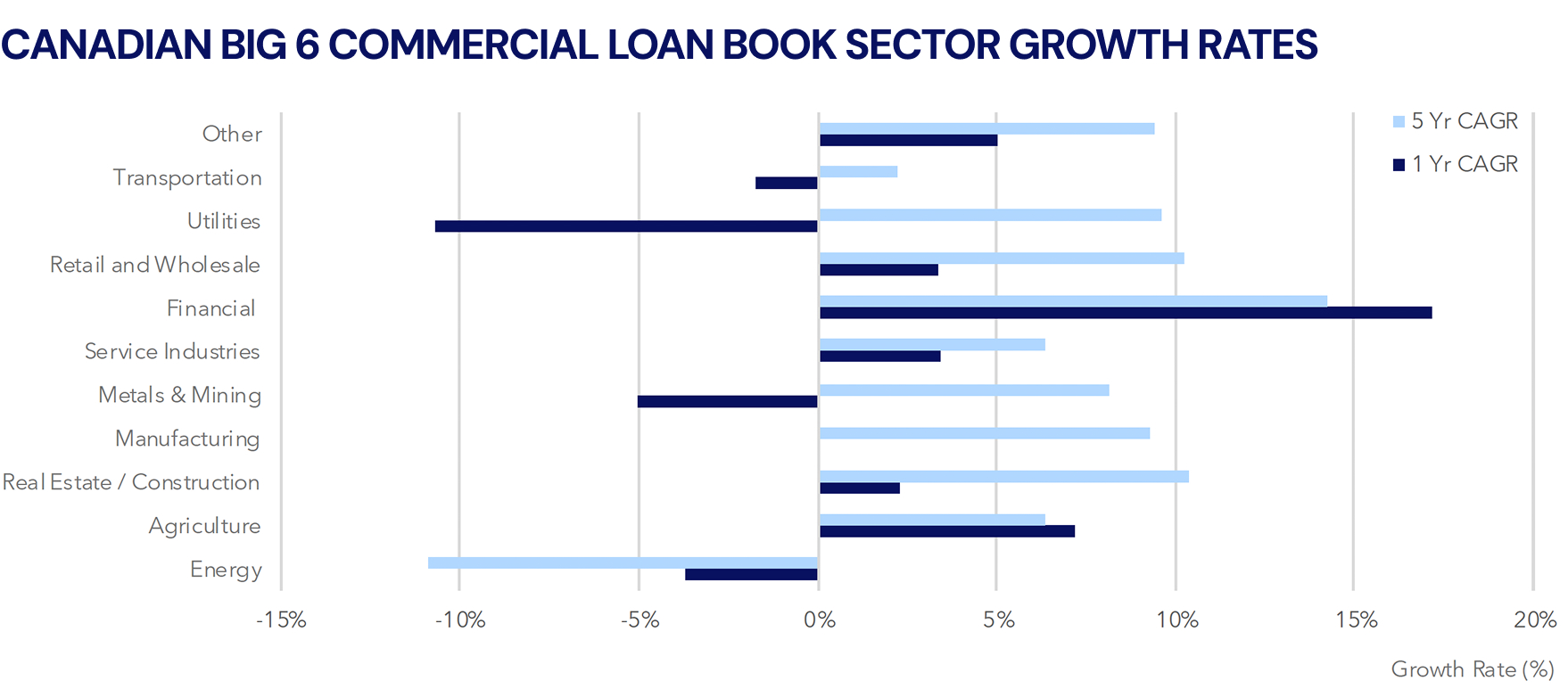

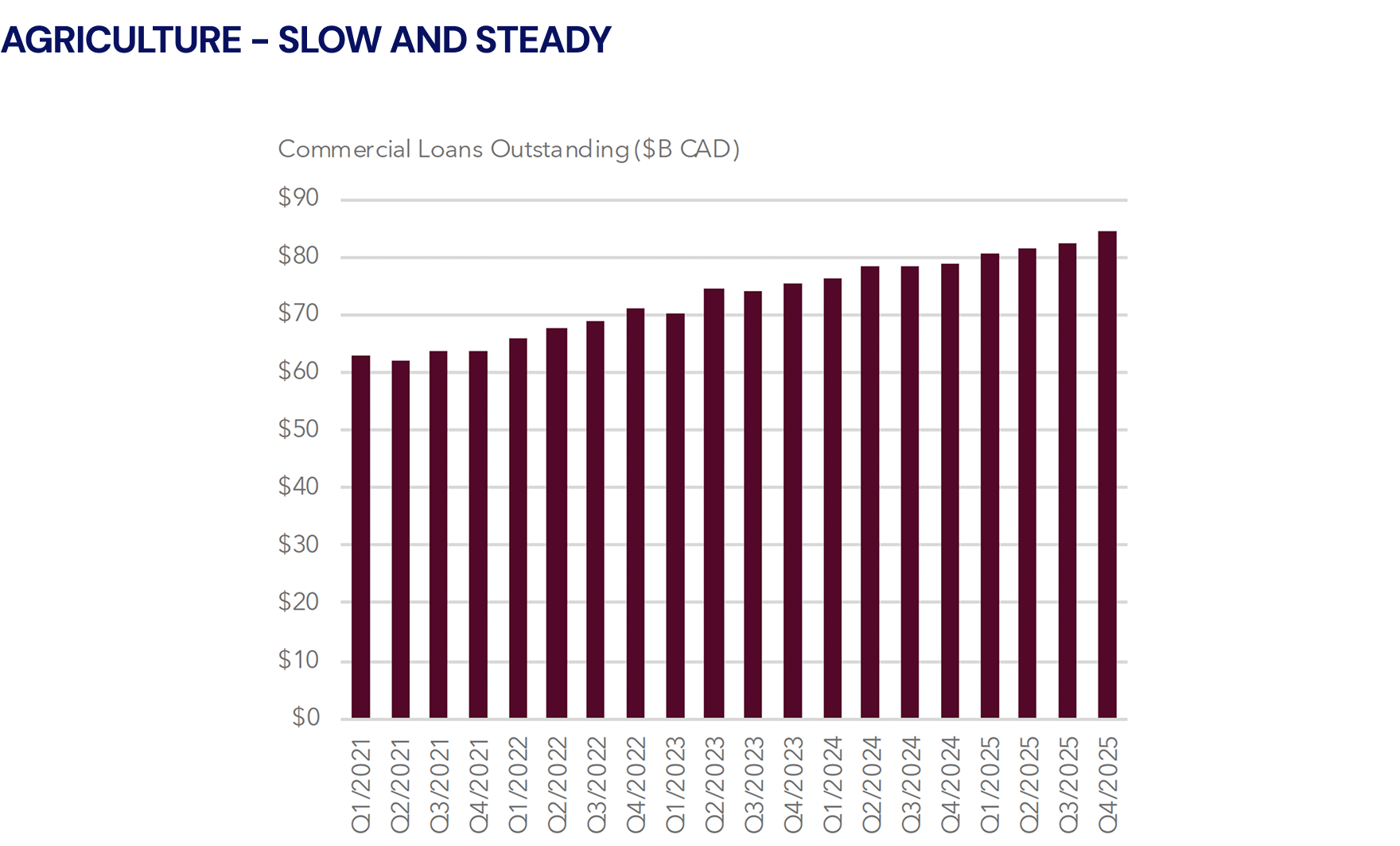

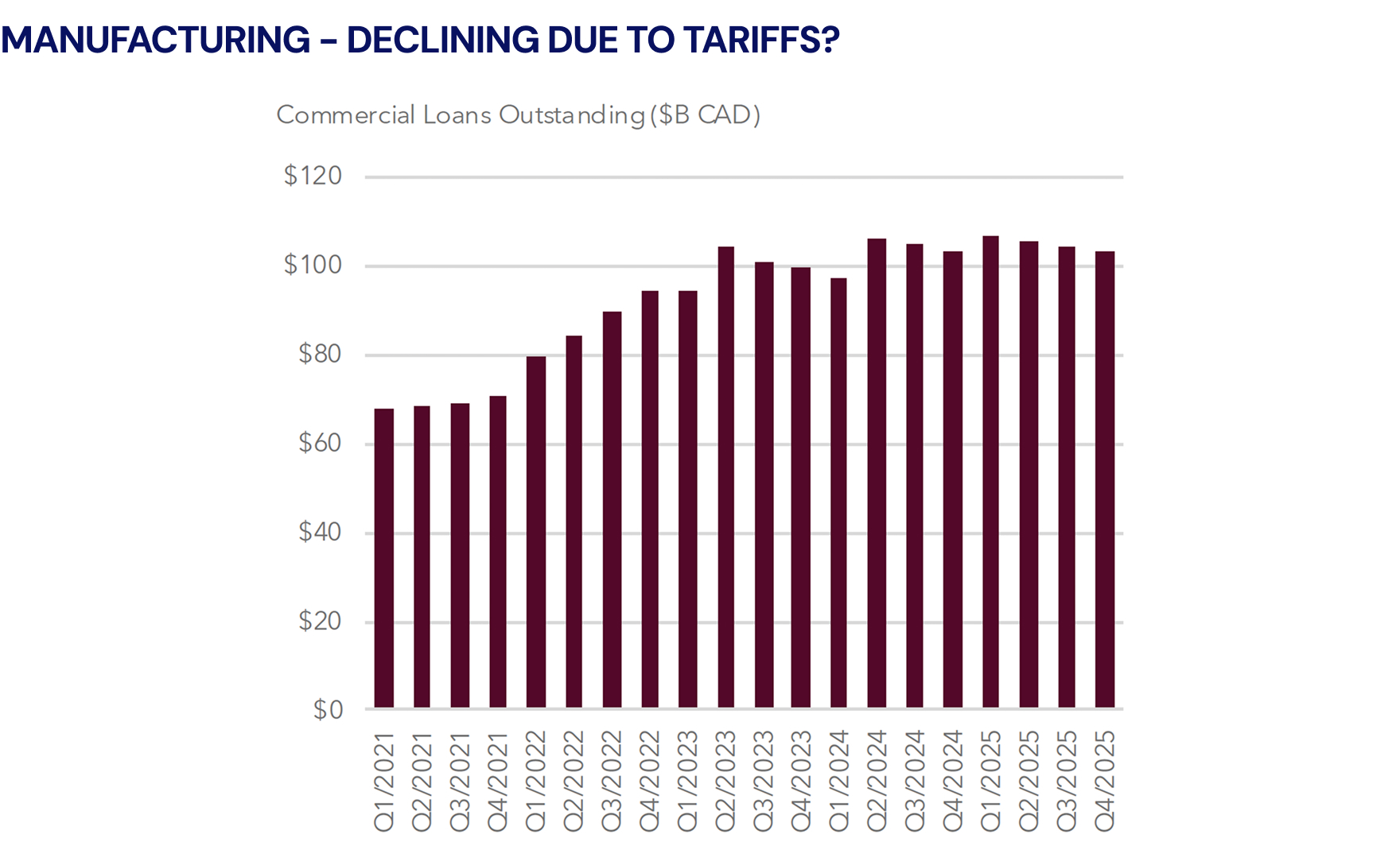

Most sectors are growing YoY, but Metals & Mining (-5%), Utilities (-11%), and Transportation (-2%) show short-term softness; Energy continues its structural decline (-4%)

Canadian Big 6 Key Sector Commercial Loans Outstanding

Based on recent announcements, we expect a surge of capital flowing into mining, power generation, and industrial services in 2026 and beyond (but are cautiously optimistic on energy). Over the next five years, the Government of Canada has earmarked more than $110 billion for these sectors, signaling a structural shift in national priorities. Traditional financial institutions appear to have stalled their appetite for these sectors, with loan books shrinking 1–10% in 2025.

This widening gap between capital need and capital supply presents a compelling opportunity for alternative lenders and investors to step in.

Source: Bank financial reporting, Diamond Willow

The Debt Digest lands in your inbox each month.