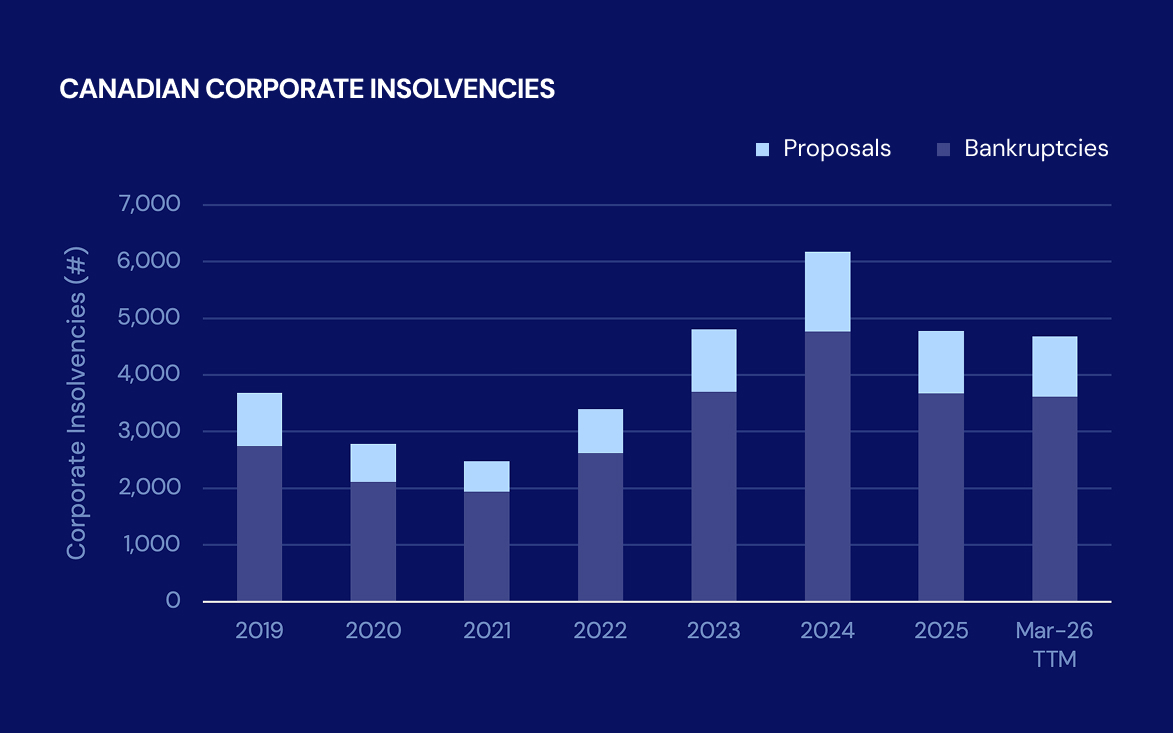

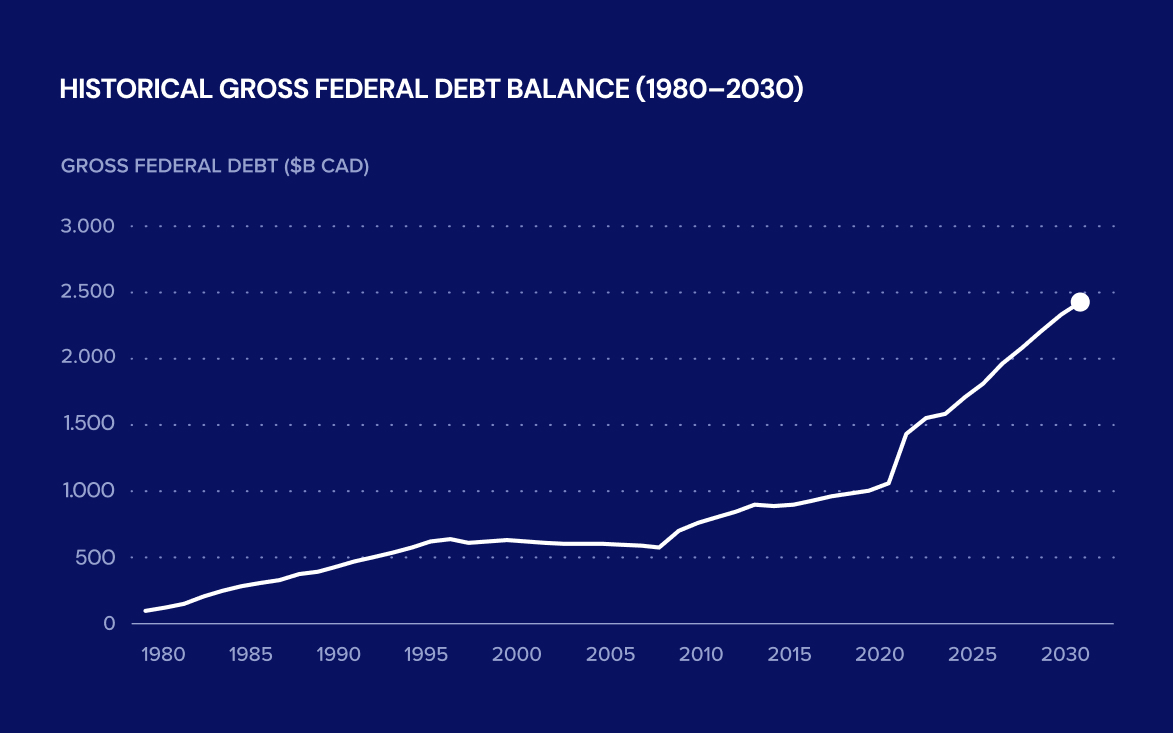

Debt Capital is available, but is getting harder to obtain.

The Canadian credit landscape continues to evolve, with private lenders gaining ground and traditional banks exercising greater caution. In this brief update, we highlight key market trends in lending activity, credit growth, capital availability, and bank loan book composition.

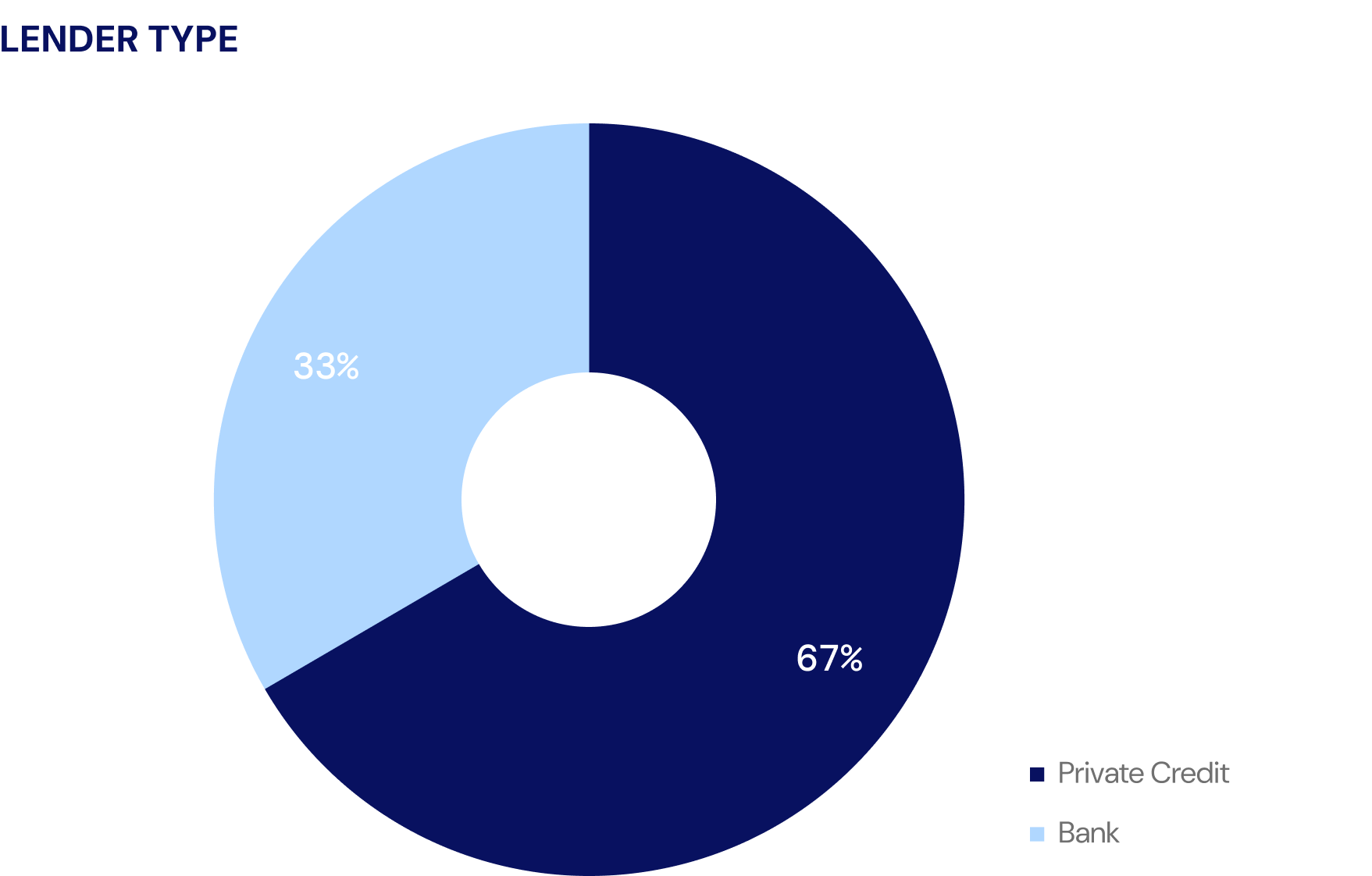

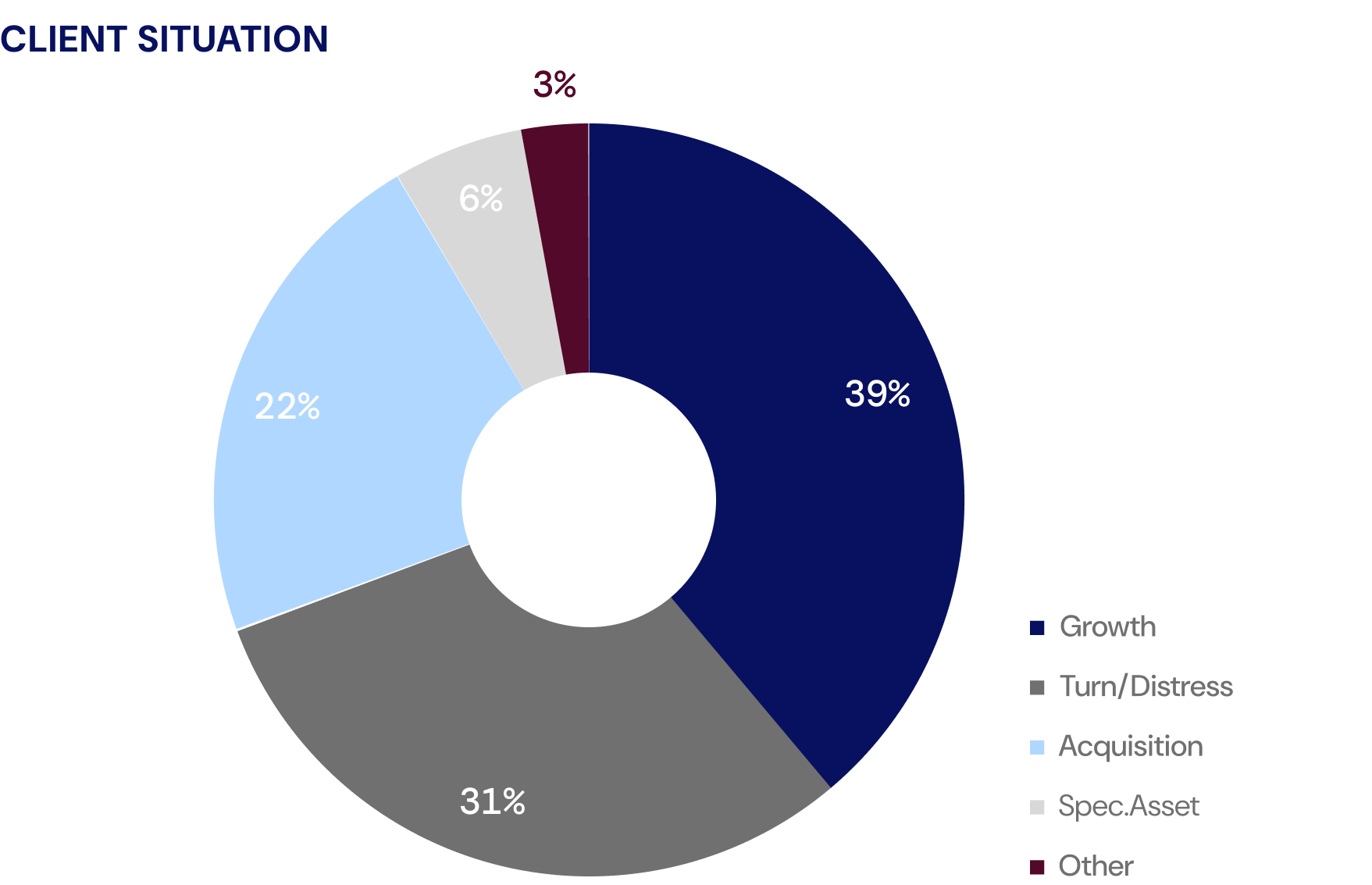

In addition, for the first time ever, we provide a snapshot of Diamond Willow’s history including industries financed, lender types, deal sizes, and client situation.

Key Takeaways this Month:

- Banks Are Tight With Capital, but Private Credit Continues to Pick Up the Slack: The bank’s loan books are stalling while Private Credit continues to grow, although 2024 was the slowest growth year in over a decade.

- Canadian Bank’s Credit Loss Provisions Continue to Rise: Although small on a total basis (thanks to Canada’s good banking regulations), loan loss provisions are up 50% year-over-year and something we have witnessed firsthand with Special Loans groups reaching out more and more for our assistance.

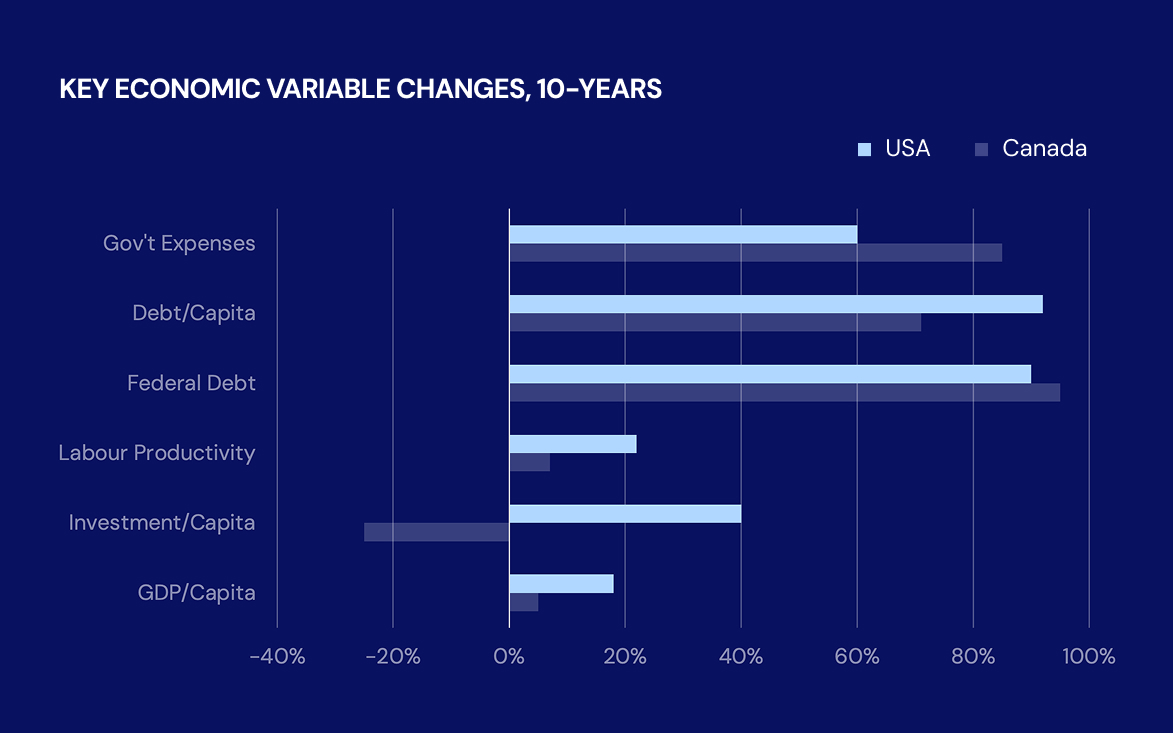

- Diligence Requirements Have Increased as a Result of Global Economic Risks: Our experience raising debt capital for corporations across Canada makes it clear the diligence requirements to raise debt capital are more robust than ever. This is thanks to the U.S. tariffs and global volatility created by President Trump, and the uncertain economic outlook.

Diamond Willow tracks every lender operating in Canada with a network of 500 lenders spanning all situations.

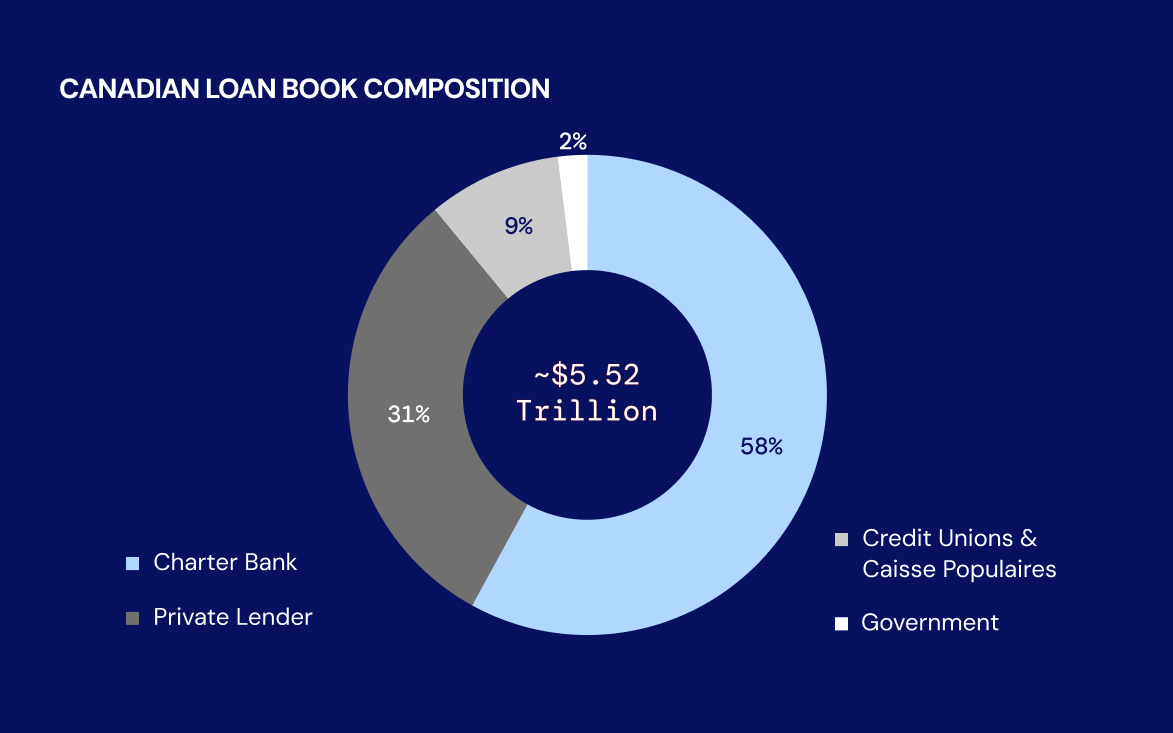

The Canadian loan book: Who’s lending?

Canadian net debt issuance is up 7% in the Mar-25 TTM period compared to 2024.

Net Debt Issuance Recovering: Net debt issuance is up 7% in the Mar-25 TTM period (compared to 2024) and loan growth is accelerating (growing at 5.2% YoY, compared to 2024’s average of 4%). We attribute this trend in loan growth to lower interest rates, continued improvement in the Canadian inflationary environment and the exceptional loan growth in private lenders.

.png)

Canada’s big banks lead in lending, but private lenders saw strong loan growth at 7.2% YoY.

Banks Dominate, but Privates Want their Piece of the Pie: While Canada’s major banks continue to dominate with about 60% of the loan book, private lenders, holding 29%, are rapidly expanding their presence. In the 12 months ending March 2025, chartered banks issued $120 billion in loans (up 3.9% YoY), while private lenders followed closely with $103 billion, marking a stronger 7.2% annual growth.

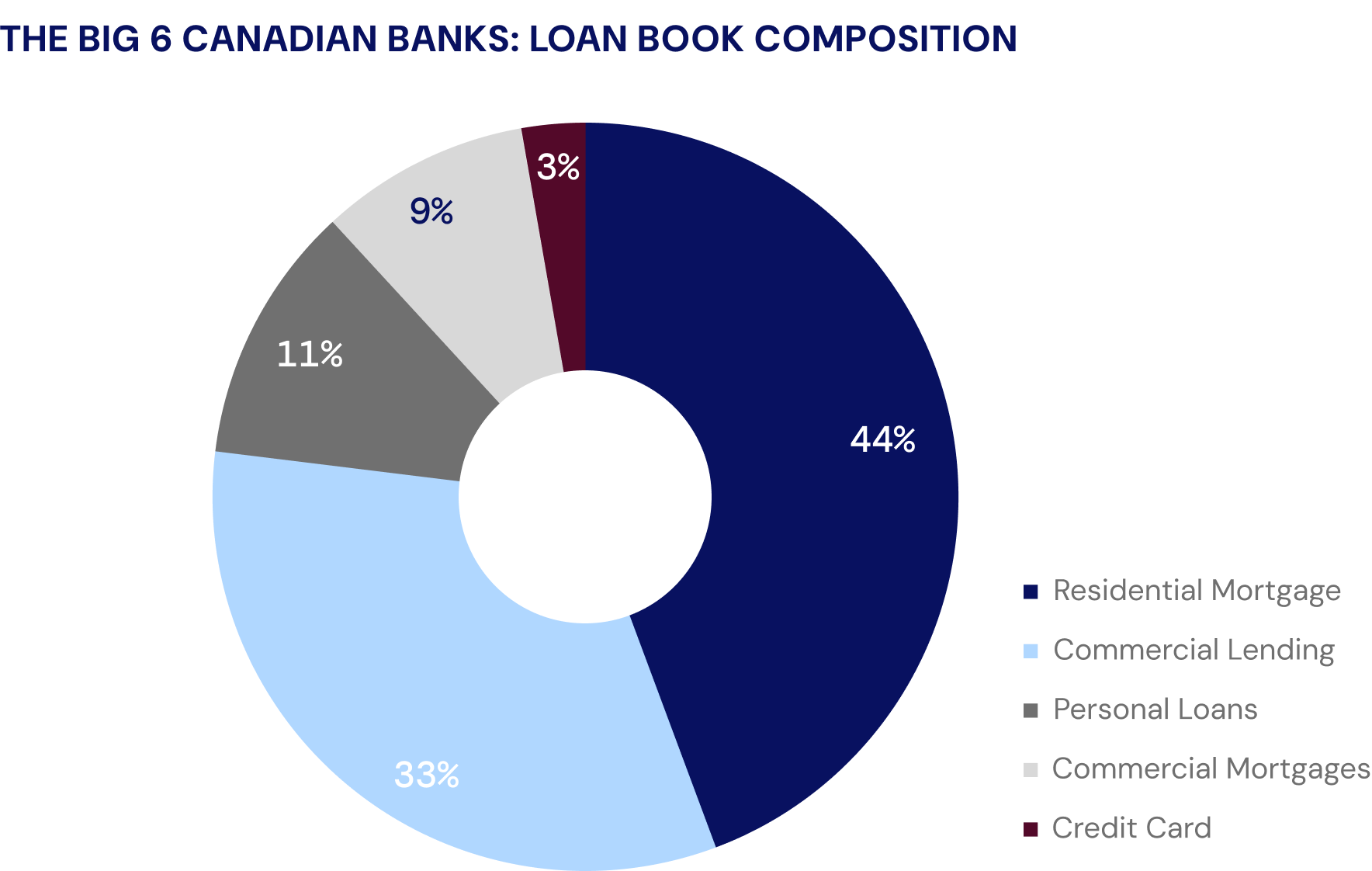

Residential mortgages dominate the Canadian Banks loan books.

Mortgages Dominate at the Big 6: The loan books of the Canadian Big 6 Bank’s continue to be dominated by residential and commercial mortgages, now accounting for 54% of their total lending activity (as of Q2 2025). This equates to approximately $2.3 trillion, which means that any material increase in mortgage defaults would have catastrophic consequences. The Big 6 have continued to diversify their exposure into commercial loan products (accounting for 33% of all lending) but have done so cautiously.

Commercial loan growth slowed materially in Q2 2025 (0.1% QoQ and 3.3% YoY).

Commercial Loan Underwriting Slows: In Q2 2025, the Canadian Big 6 grew commercial loan books by 0.1% (up 3.3% from Q2 2024), continuing a trend of decelerated loan growth since Q3 2024 where commercial loan growth last peaked at 10.3% YoY. Loan book growth is down compared to Q2 2024 (9.5% YoY growth) and Q2 2023 (13.5% YoY growth). Continued macroeconomic uncertainty appears to be playing a central role in this limited growth as Canadian banks appear to be extending credit to commercial operators more cautiously compared to the past.

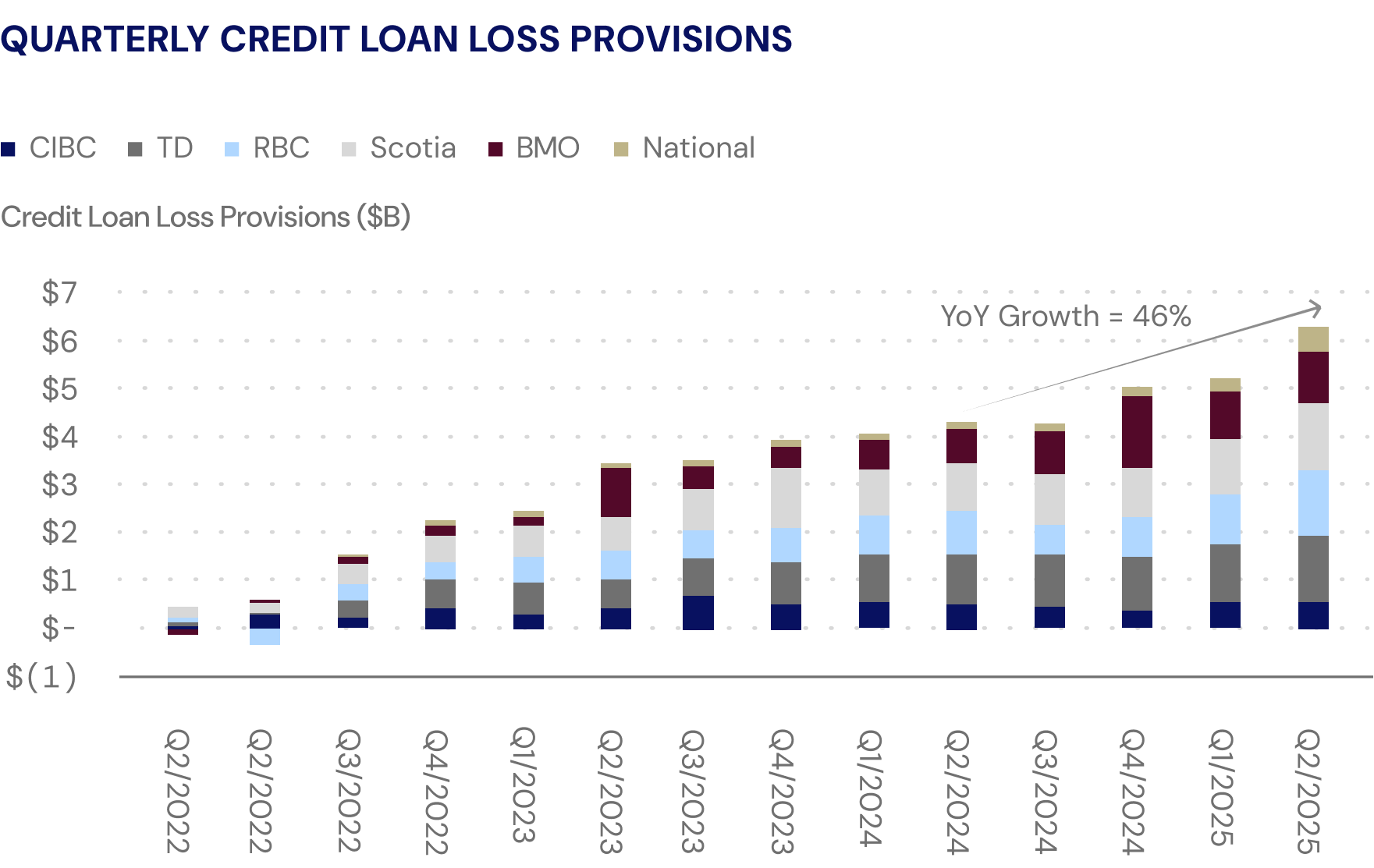

Credit loan loss provisions are up 46% YoY in Q2, signaling the banks are prepping for economic uncertainty.

Loan Loss Provisions Up, But Decelerating: The Canadian Big 6 continue to set aside larger provisions for bad loans – up to $7 billion in Q2 2025 (20.9% increase QoQ, 246% increase YoY). While this level is not unprecedented, it may signal the Big 6’s decreasing risk appetite for new loan growth. This level of credit loan loss provisions has not been seen since COVID, where it peaked at $11 billion.

Private credit markets: Show me the money!

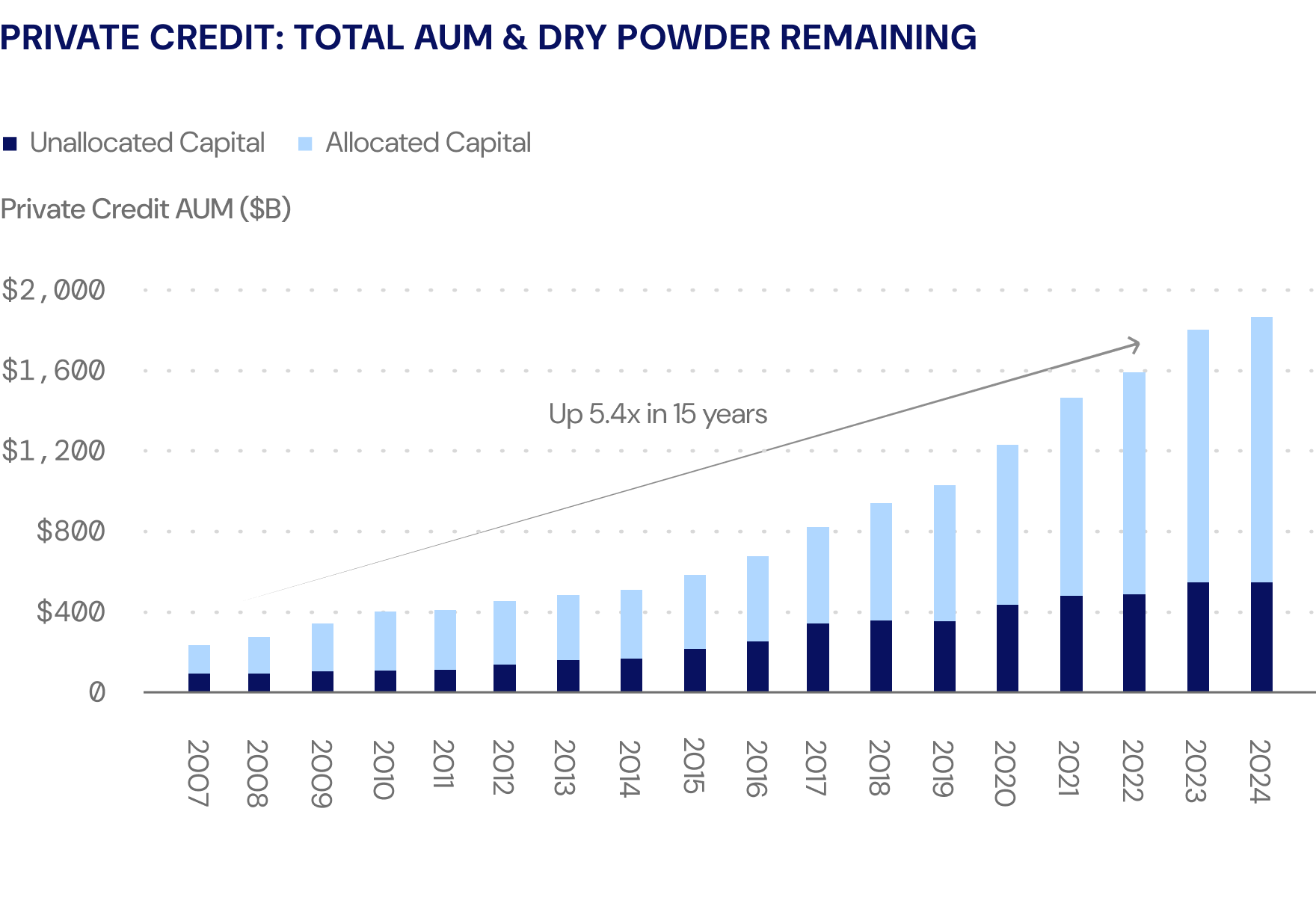

Private Credit is flush with $557 billion of cash globally and ready to lend.

Private Debt Markets are Primed and Ready to Go: Over the past 15 years, the global private credit market has expanded nearly 5.4x to reach $1.83 trillion (as of September 2024). In Canada, DWA actively tracks over 450 private lenders, categorized by lending type, security, rates, and size. Demand remains strong, with no shortage of private capital appetite - a trend backed by the $557 billion in global dry powder ready to deploy.

If you want the money you have to pay for it.

Talk to your lender about variable versus fixed rate strategies as they impact cost, pre-payment penalties, re-financing issues, etc.

Diamond Willow Advisory

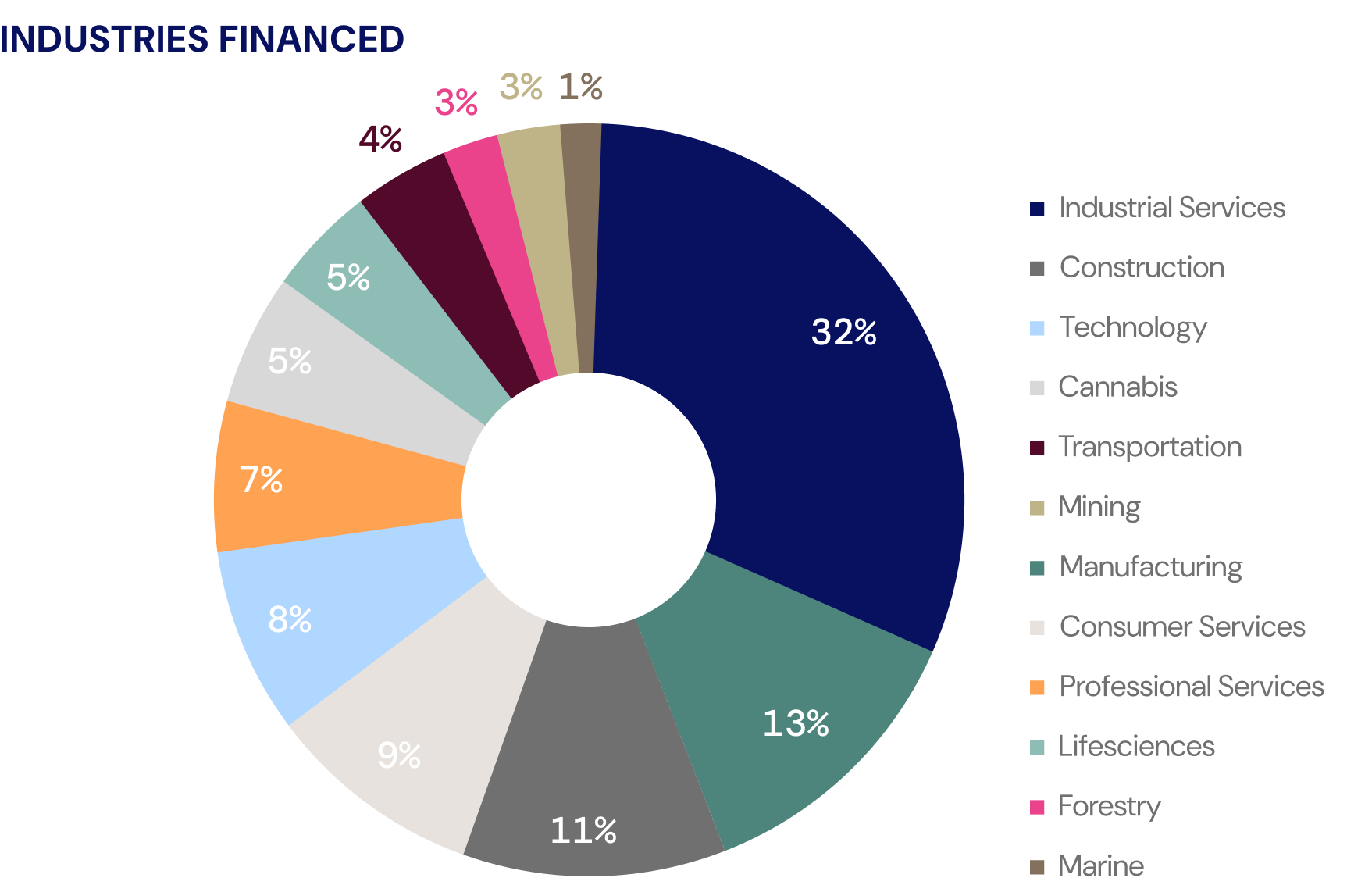

Diamond Willow has worked in a diverse suite of sectors across Canada.

Clients often pre-shop the banks, which can limit our ability to explore these options.

Our typical deal size has increased over time and is typically $5 - $30 million.

Our clients are typically growing fast, acquiring, turning around, or have specialized assets.

Sources: Statistics Canada, Bank Earnings Reports, Bank of Canada, PitchBook, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.