Loan books are growing, but so are bad loans.

With a flurry of recent developments at Canada’s Big 6 Banks, including RBC’s acquisition of HSBC, National Bank’s announcement to acquire CWB, and the Bank of Canada reducing the policy rate by 25 basis points, it appears the sector is positioned for strength. However, with credit loan loss provisions increasing yet again in Q2 2024 (the eighth consecutive quarter of such increases), it appears the ‘higher-for-longer’ interest rate environment continues to have negative implications for indebted Canadian consumers and business owners.

Key takeaways this month:

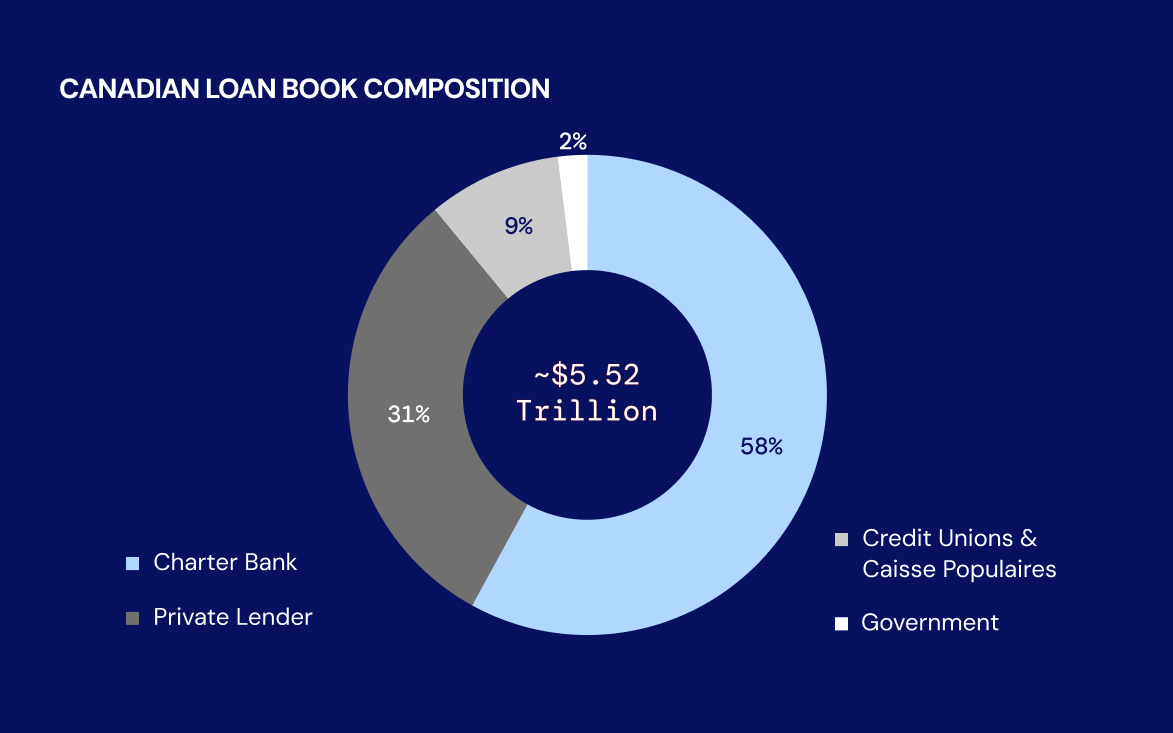

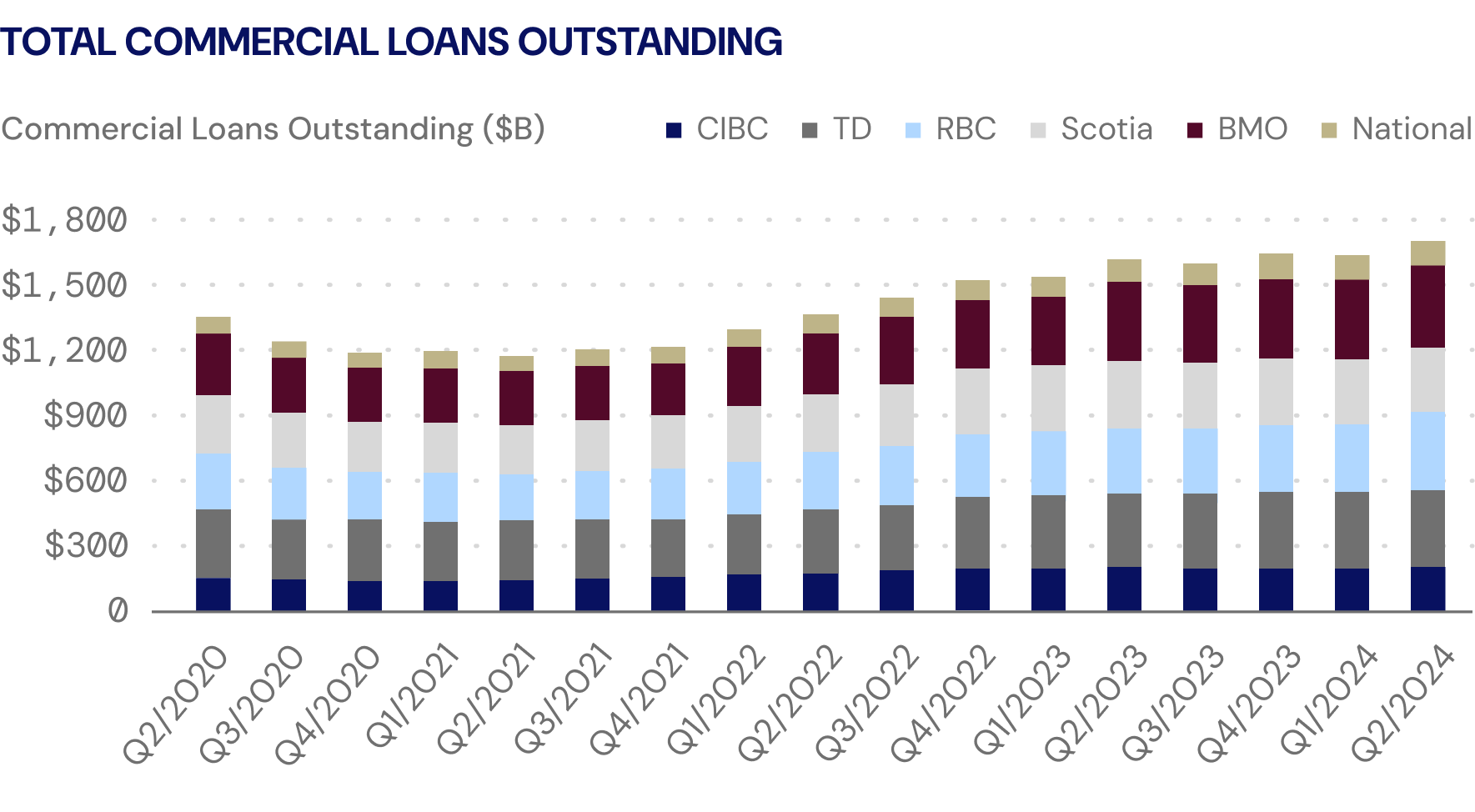

- Commercial Loans Continue To Grow: Contrary to popular belief, the commercial loan environment in Canada continues to experience modest growth of 1.2% Q/Q (4.2% if you include RBC’s acquisition of HSBC).

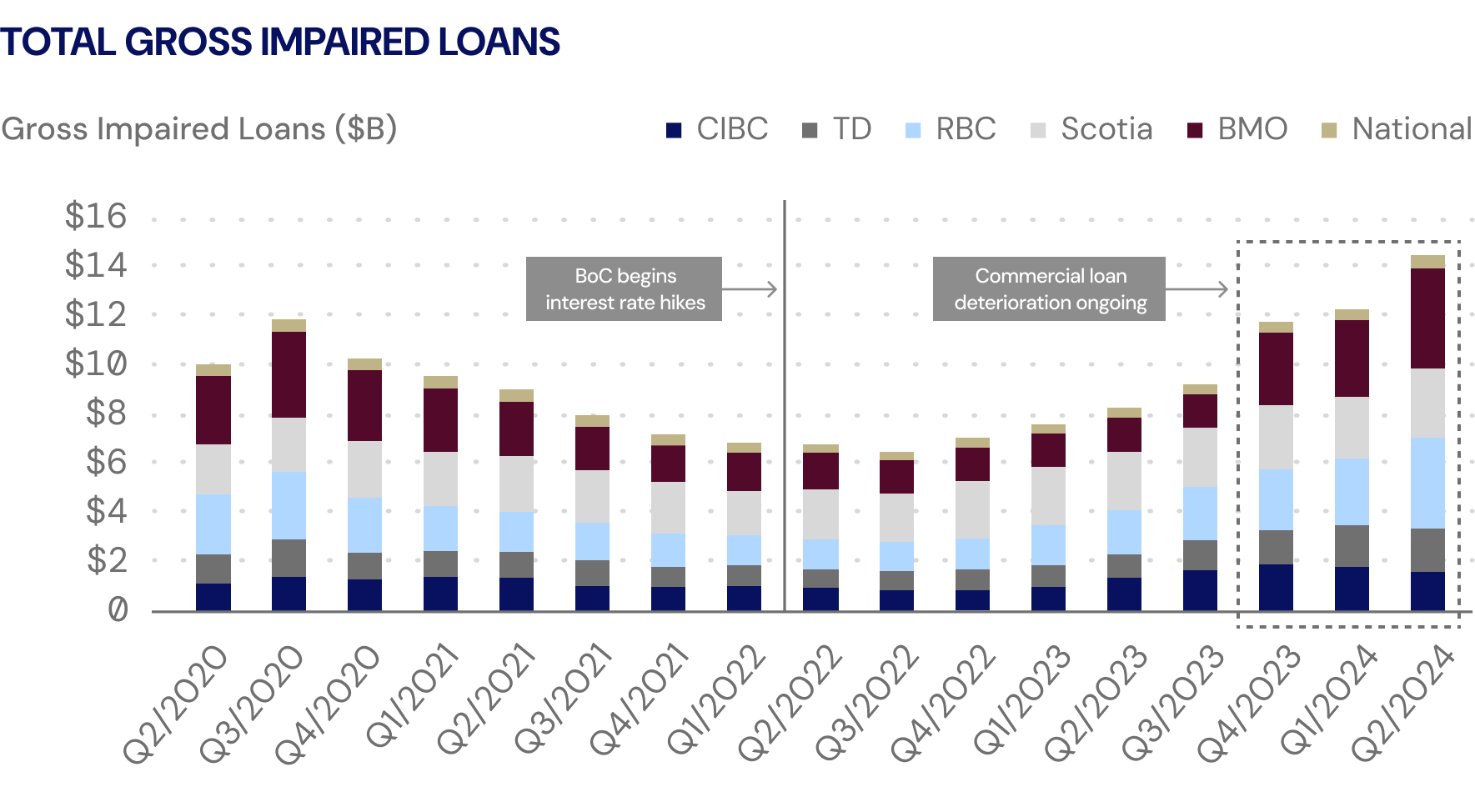

- Gross Impaired Loans and Credit Loss Provisions Ramping: Gross Impaired Loans and Credit Loan Losses have increased for the seventh and eighth consecutive quarters, respectively, with impaired loans now representing 0.85% of the national loan book or $14 billion.

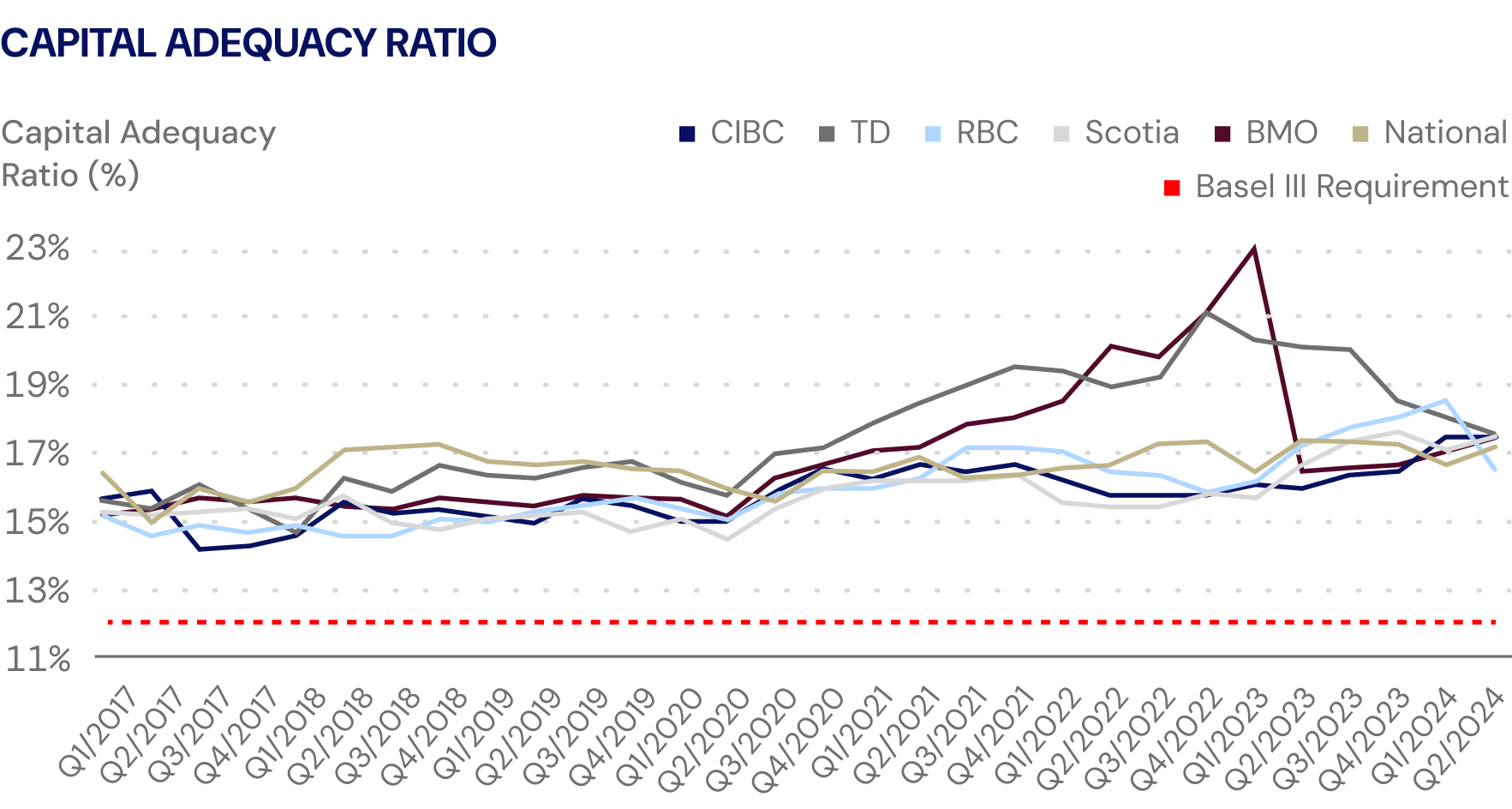

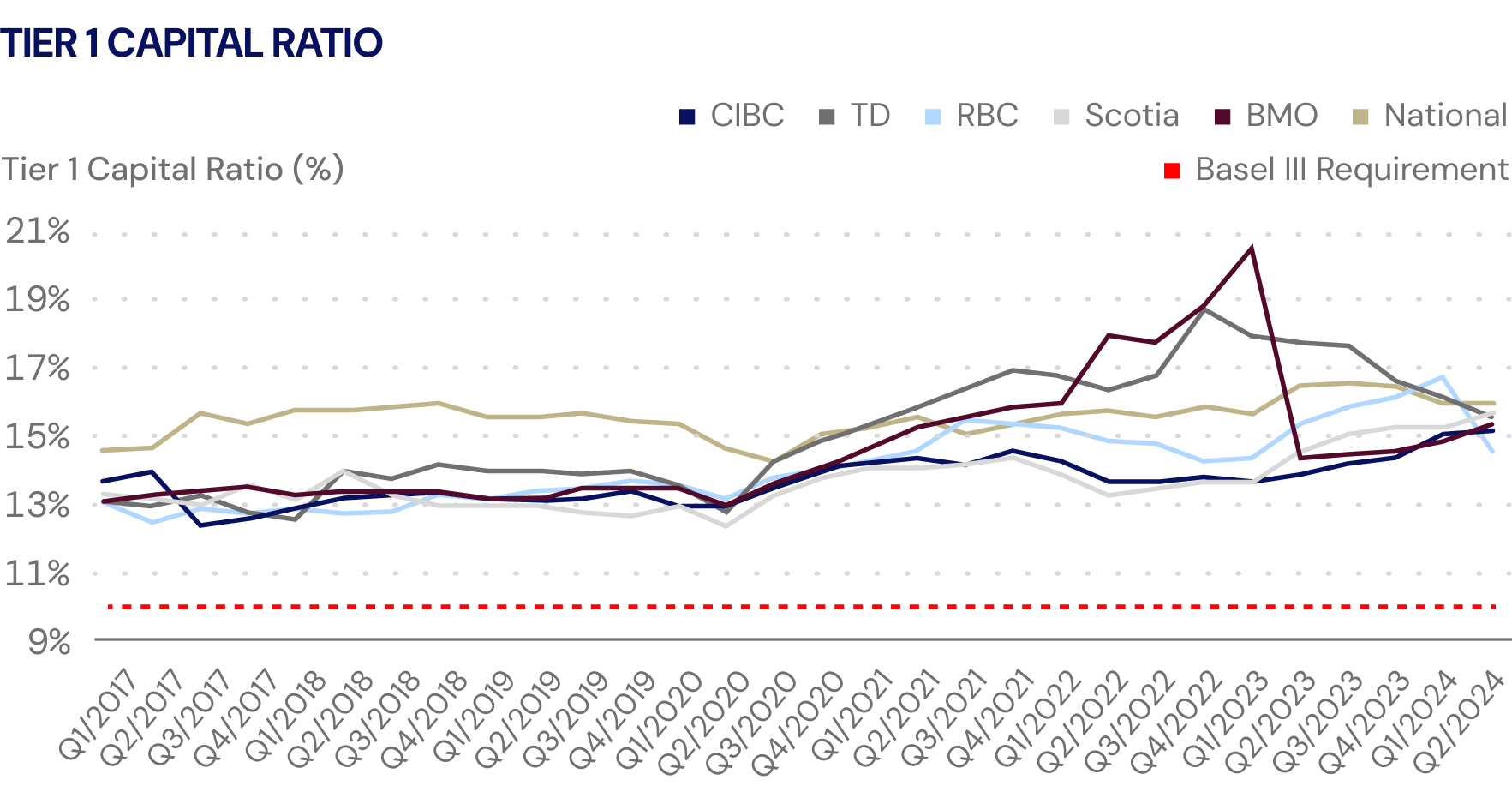

- Capital Buffers Are Comfortable: In response to the BoC’s 2022 rate hike campaign, Canada’s Banks increased their capital adequacy to ensure they remained onside with stringent regulations.

Q2/24 commercial loan growth increased 1.2% (4.2% including RBC’s acquisition of HSBC)

Q2/24 gross impaired loans rose 17.6% Q/Q and 112% since Q2 2022 when the BoC began interest rate hikes.

Gross Impaired Loans Continue To Remain Elevated: Gross impaired loans continue to accelerate (most notably 17.6% Q/Q in Q2 2024) as credit conditions continue to remain tight in response to the Bank of Canada aggressive rate hiking cycle in 2022. This represents the seventh straight quarter of growth in gross impaired loans, which currently represent 0.85% of the national commercial loan book or $14 billion.

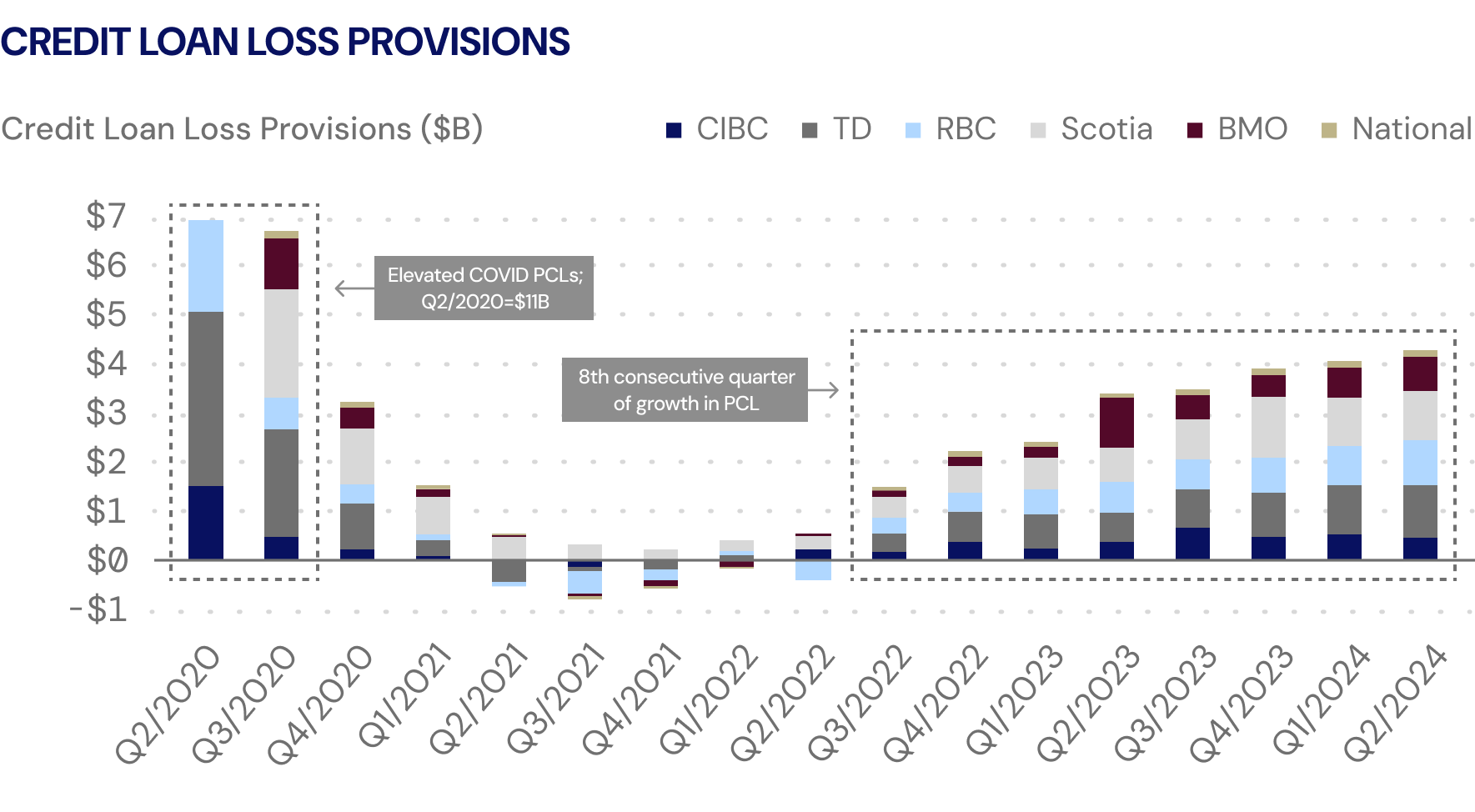

Credit Loss Provisions have increased for 8 consecutive quarters.

Are The Banks Running Out Of Sandbags?: Provisions for credit loans losses have increased for a staggering eighth consecutive quarter, increasing 5.8% Q/Q in Q2 2024 and now accounting for 0.3% of the national commercial loan book. While still depressed from COVID levels, which reached $11 billion in Q2 2020, the rise of credit loan loss provisions signals the Canadian Banks are anticipating continued challenges for borrowers while interest rates slowly decline.

Canada’s Banks are maintaining capital ratios well above those required by regulators (BASEL III).

Is Capital Well Positioned Or Sidelined?: Following the Bank of Canada rate hike campaign in 2022, Canada’s Big 6 responded by ensuring they had adequate capital to withstand any projected economic hardship. The initial 25 basis point rate cut by the BoC on June 5th is expected to provide some relief and allow the Big 6 to increase their appetite for loans, however the magnitude and speed that the BoC is able move is largely uncertain. Until then, it appears a large amount of the Big 6’s capital will remain sidelined to preserve their capital flexibility.

Sources: Earning Reports, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.