Recent economic data has made a strong case to start easing policy rates in Canada.

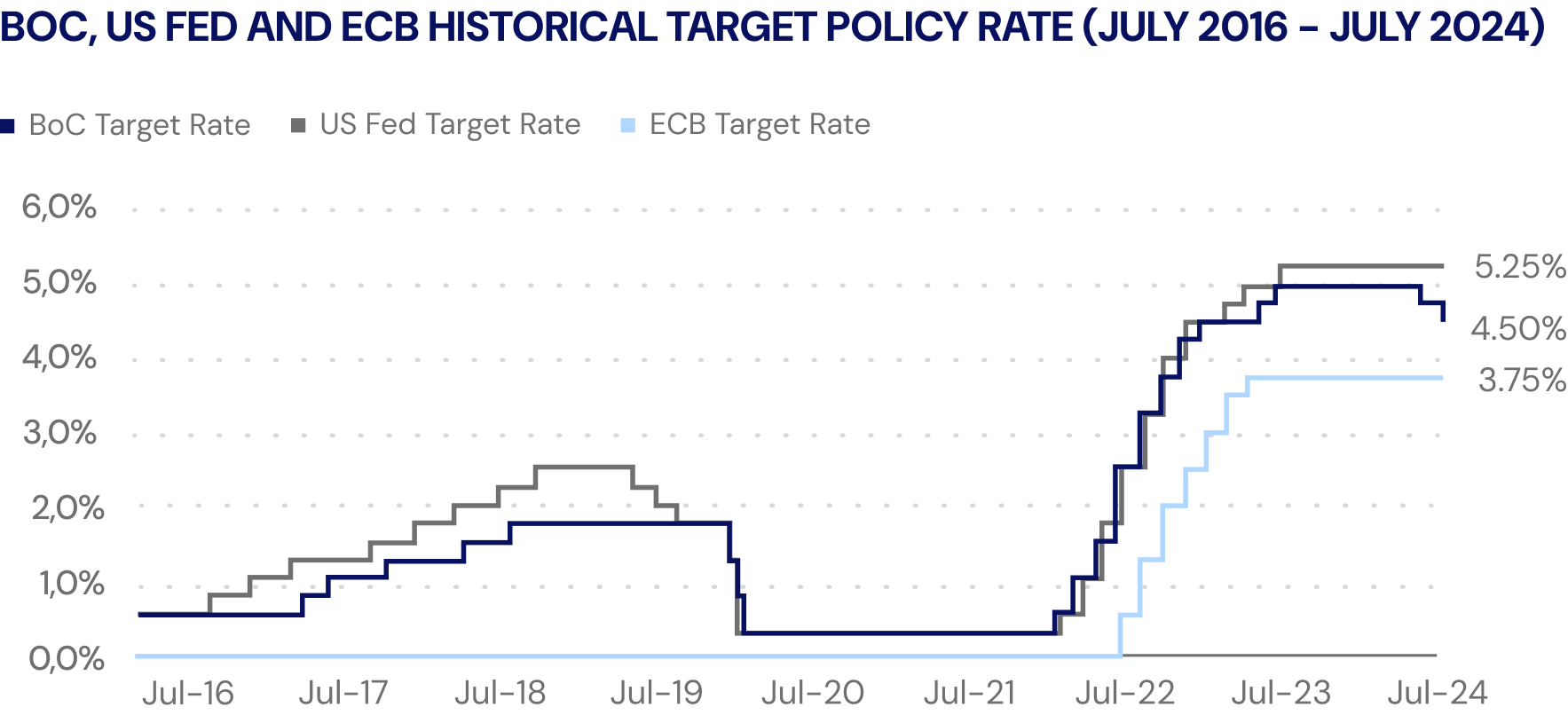

The BOC recently cut its key policy rate to 4.5% (from 4.75%), leading the US and ECB who have yet to cut. June 2024 CPI data, which came in at 2.7%, rising unemployment rates, and a reduction in non-essential consumer spending seem to be the driving force behind the decision to cut. There is still work to do to get inflation down to the target 2% but the trend seems to be the BOC’s friend. It is going to be interesting to watch the Bank of Canada over the next few months.

Key Takeaways this Month:

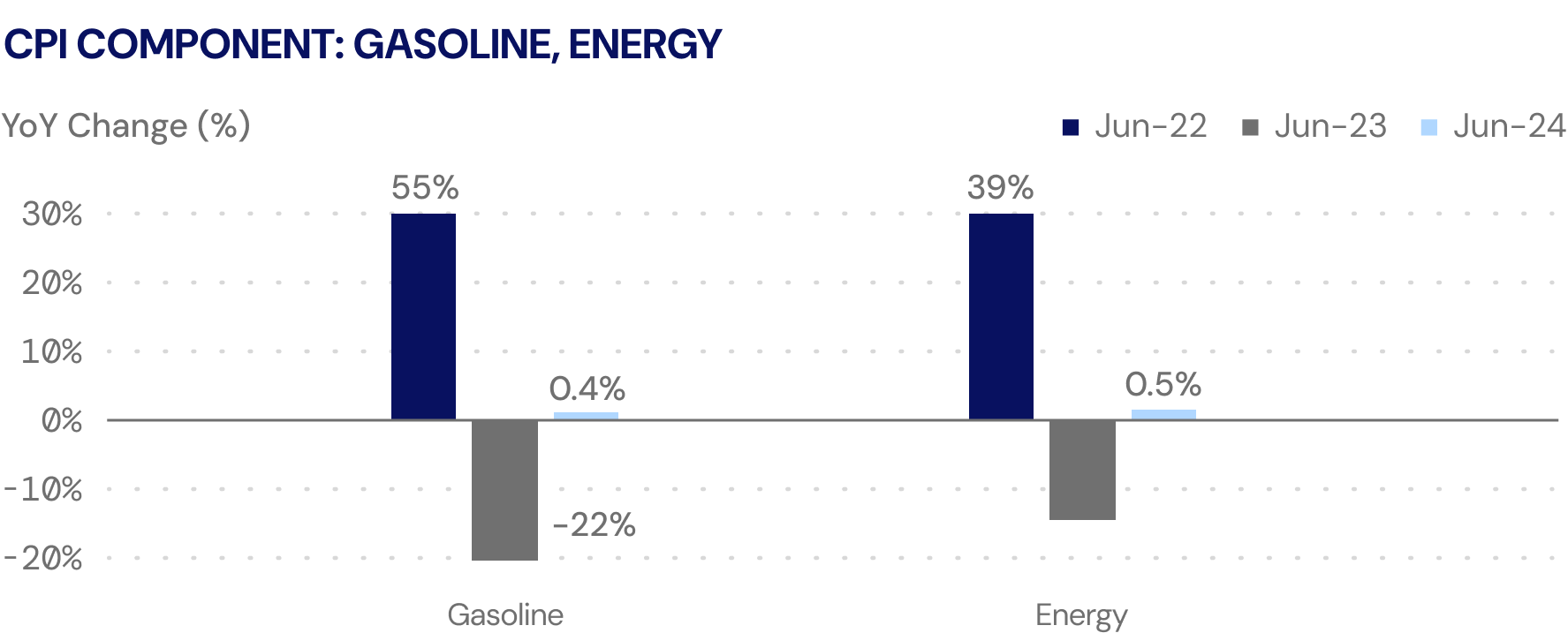

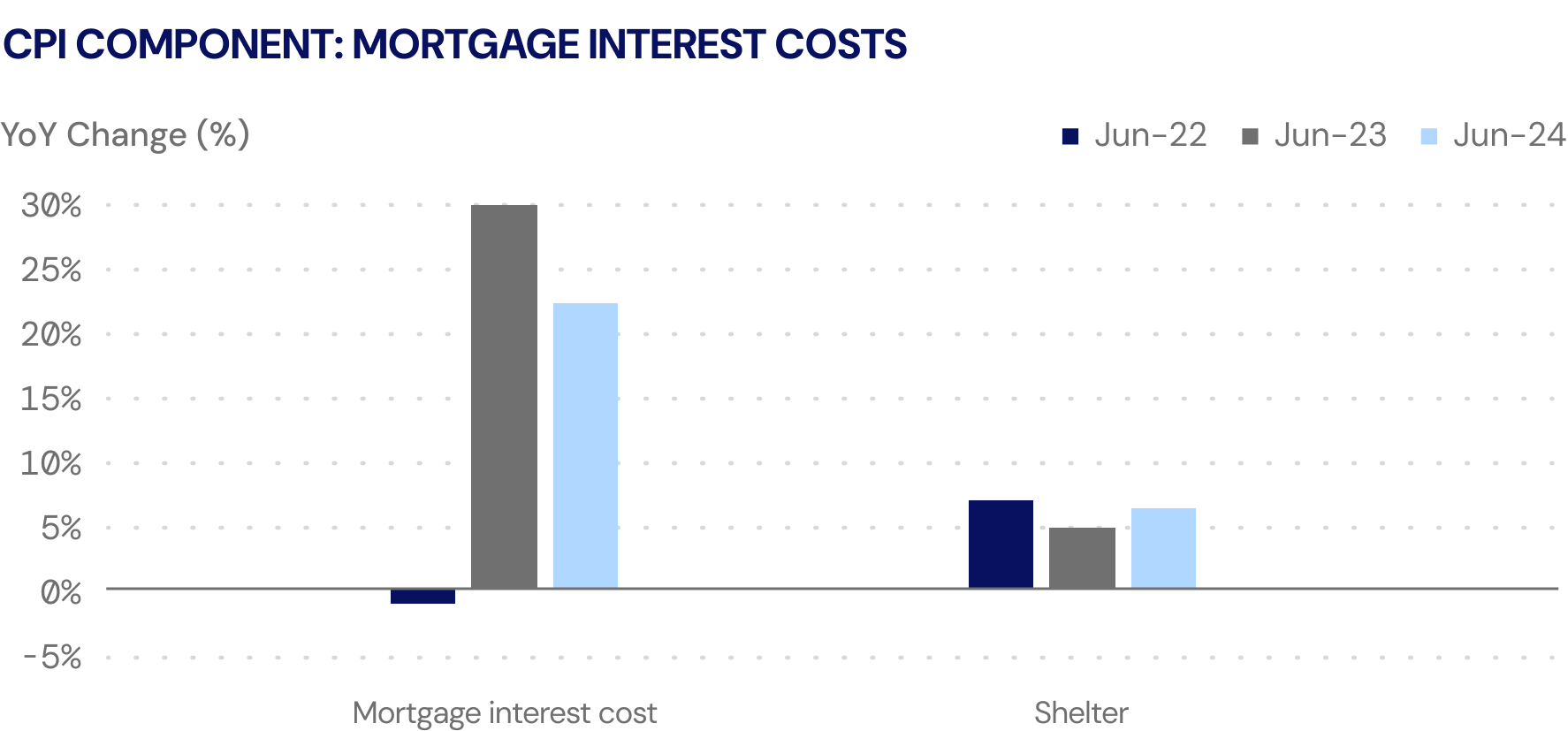

- Inflation Is Slowing But Staying Sticky: While inflation has declined from its highs in 2022, certain components continue to remain persistently sticky. Namely, mortgage interest costs remain at 22%.

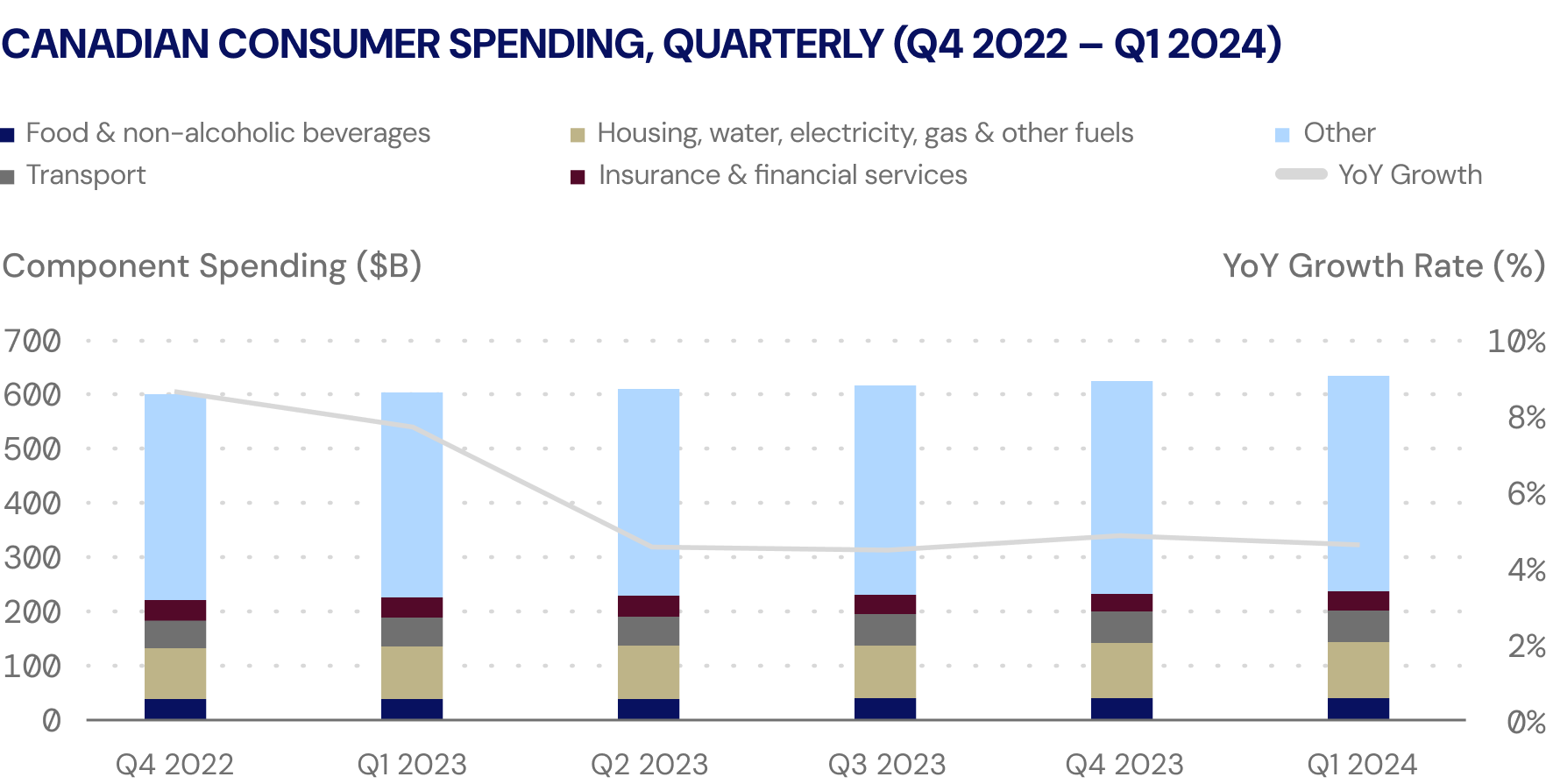

- Consumer Spending is Moderating: Consumer spending on non-essential goods has been decelerating while inflation on essential goods continues to force Canadians to spend more than desired.

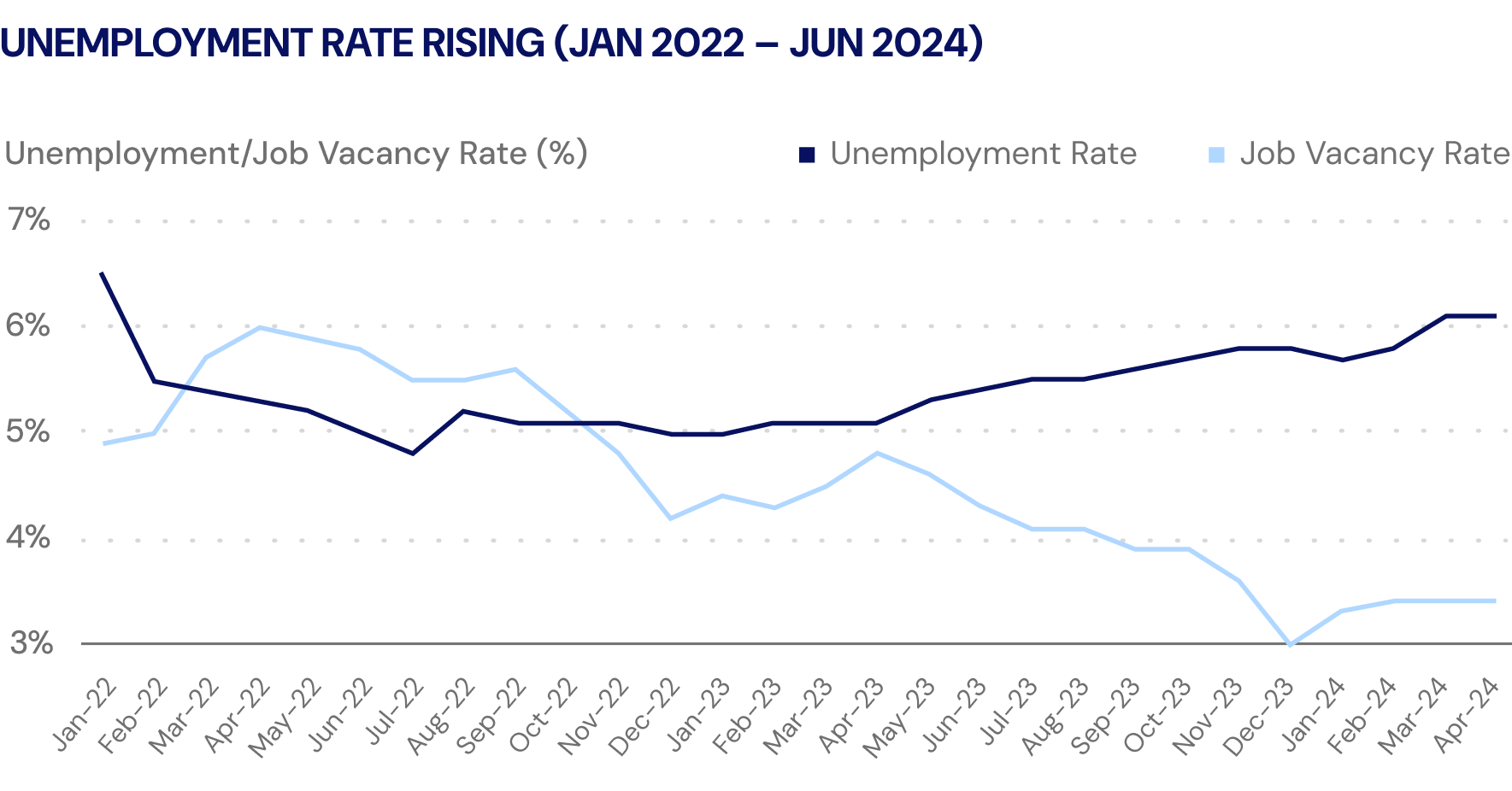

- The Labor Market Is Balancing: In response to the BoC’s 2022 rate hike campaign, Canada’s labor market has shown some signs of balance with the unemployment rate reaching 6.4% (as of June 2024) and job vacancies decreasing by 28% YoY in June 2024.

After an extensive rate hiking cycle, the BoC has begun cutting its target rate.

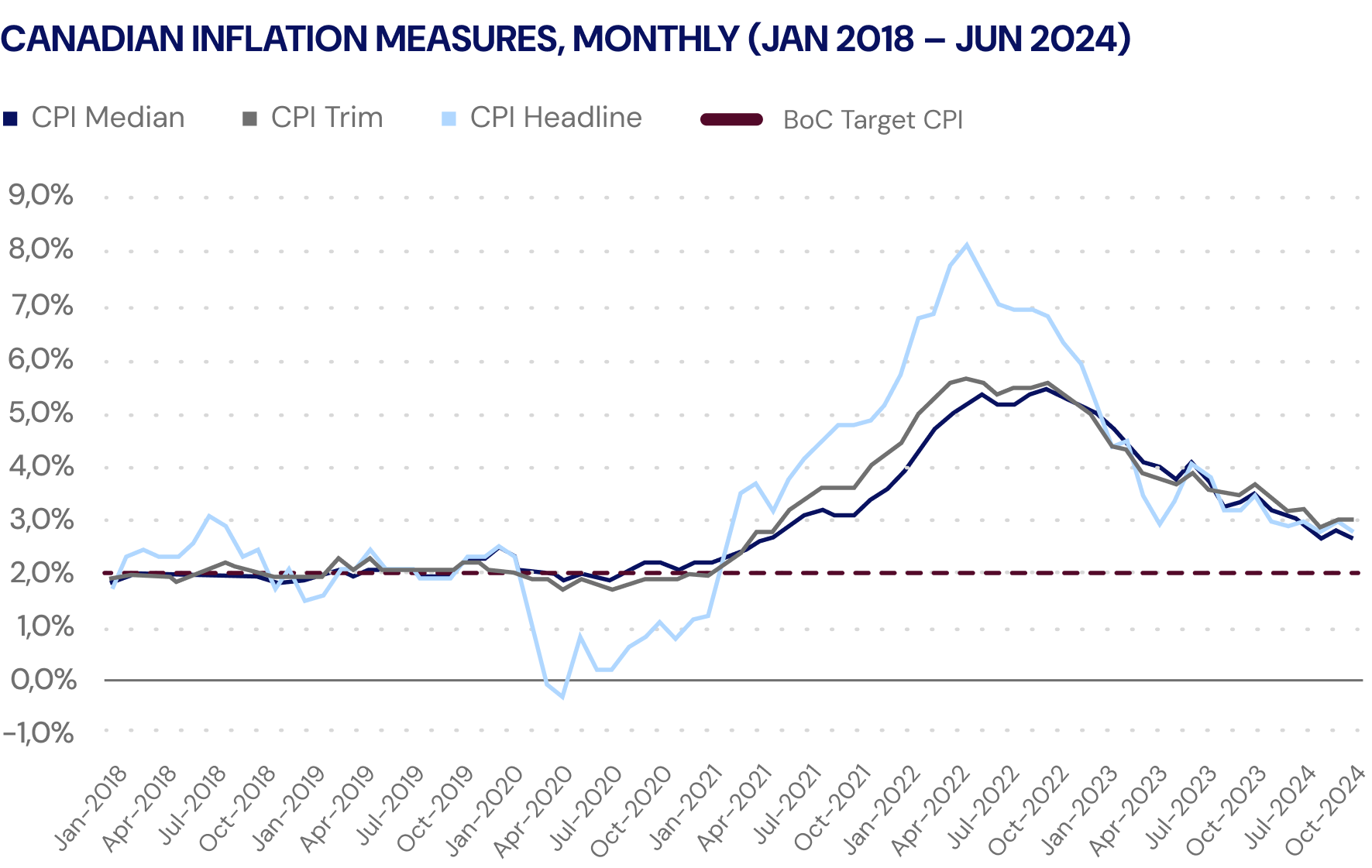

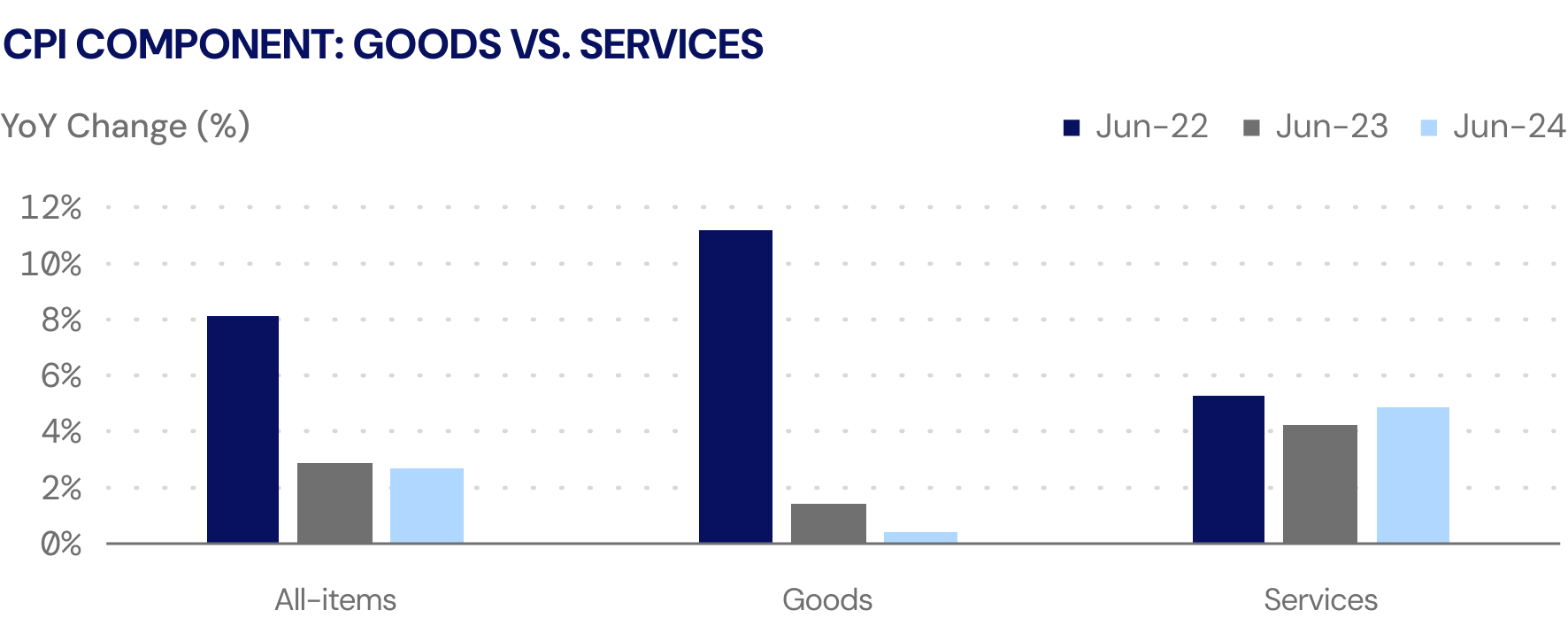

While inflation cooled to 2.7% in June, some elements of inflation remain persistently sticky.

Inflation Is Cooling, But Shelter Costs Remain Elevated: After a slight uptick in May 2024 (+2.9%), inflation continued to moderate downwards to +2.7% YoY in June 2024. The deceleration in inflation has largely been explained by the slowdown in Goods (+0.3%), but there are several components of inflation that continue to be sticky. Namely, mortgage interest costs continue to remain elevated at 22%!

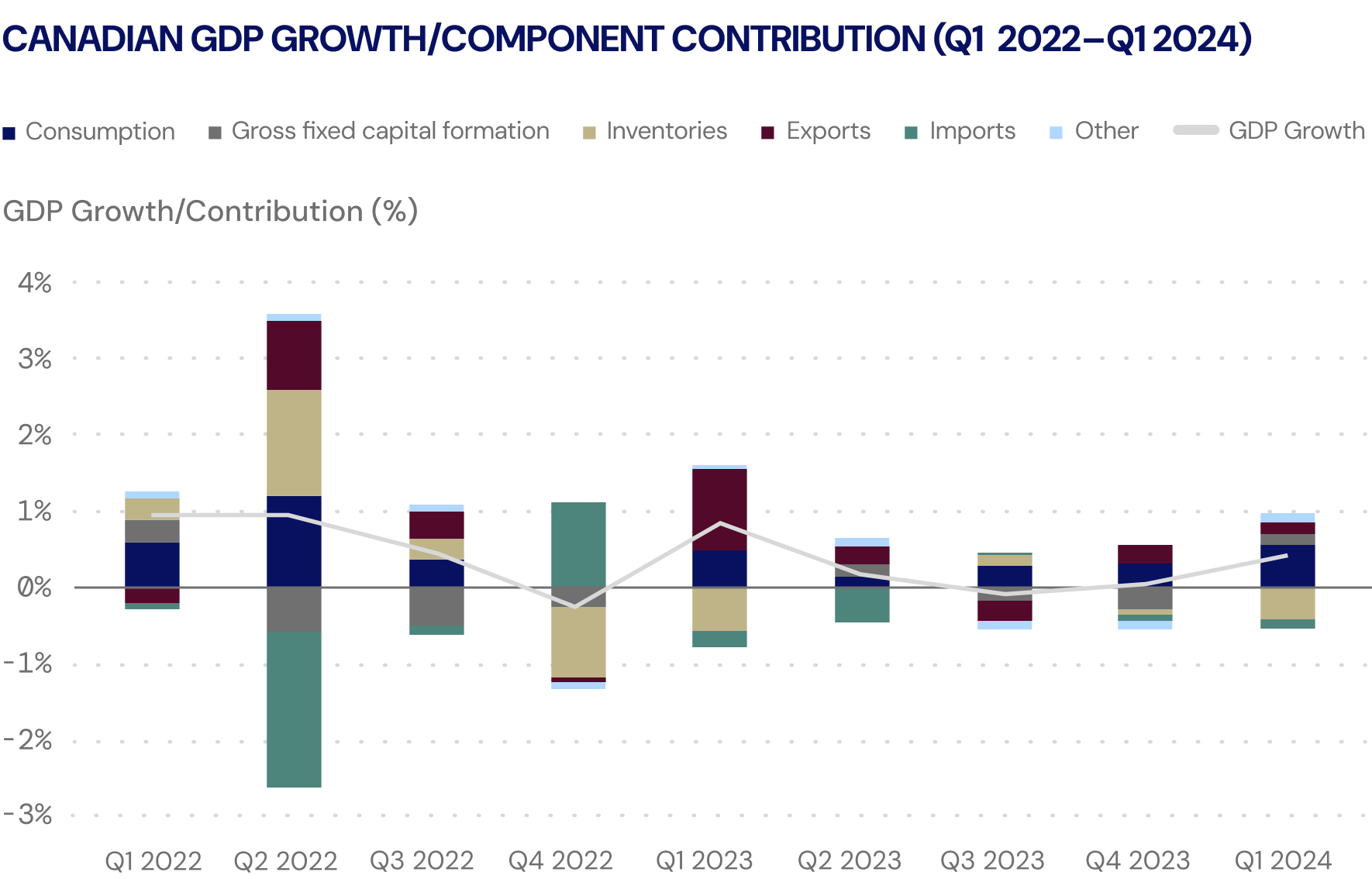

Canadian GDP grew by 0.4% in Q1 2024, largely supported by consumer spending (0.6% QoQ growth).

GDP Assessment A Mixed Bag: On the surface, quarterly GDP growth may appear quite depressed but certain components, namely consumer spending (+0.6% QoQ), continue to remain elevated despite the BoC’s aggressive interest rate hikes. This provided a good indication that the BoC’s actions successfully curtailed demand in the Canadian economy, which continues to experience moderate growth. Early indications from April’s flash estimate for GDP provided solid growth (+0.3%) and the BoC has expressed that a ‘soft-landing’ is possible.

The Labor Market appears to be balancing with an unemployment rate of 6.4%.

Balance Appears To Be Returning To The Labour Market: Over the past 12 months, a total of 165,500 FT jobs were added to the Canadian economy (compared to 312,400 FT jobs in 2023), signaling that the labor market is likely re-balancing itself. Overall, the labor market has appeared to moderate with the unemployment rate increasing to 6.4% (as of June 2024) and job vacancies now, on average, being 28% below levels seen in 2023 (~605,000 job vacancies in April 2024 vs. ~840,000 in April 2023).

Consumer spending has flattened but is still up YoY.

Consumer Spending Lukewarm: While Canadian consumer spending continues to grow at 4.6% YoY (as of Q1 2024), it has decelerated considerably since the BoC embarked on their rate hiking cycle in 2022. Essential spending such as Food, Housing, Transportation, Insurance and Financial Services continue to put strain on the pocket-books of Canadians – on average, these costs are increasing by 6.2% YoY but accounts for 60% of consumer spending. Non-essential spending is decelerating at an expedited rate.

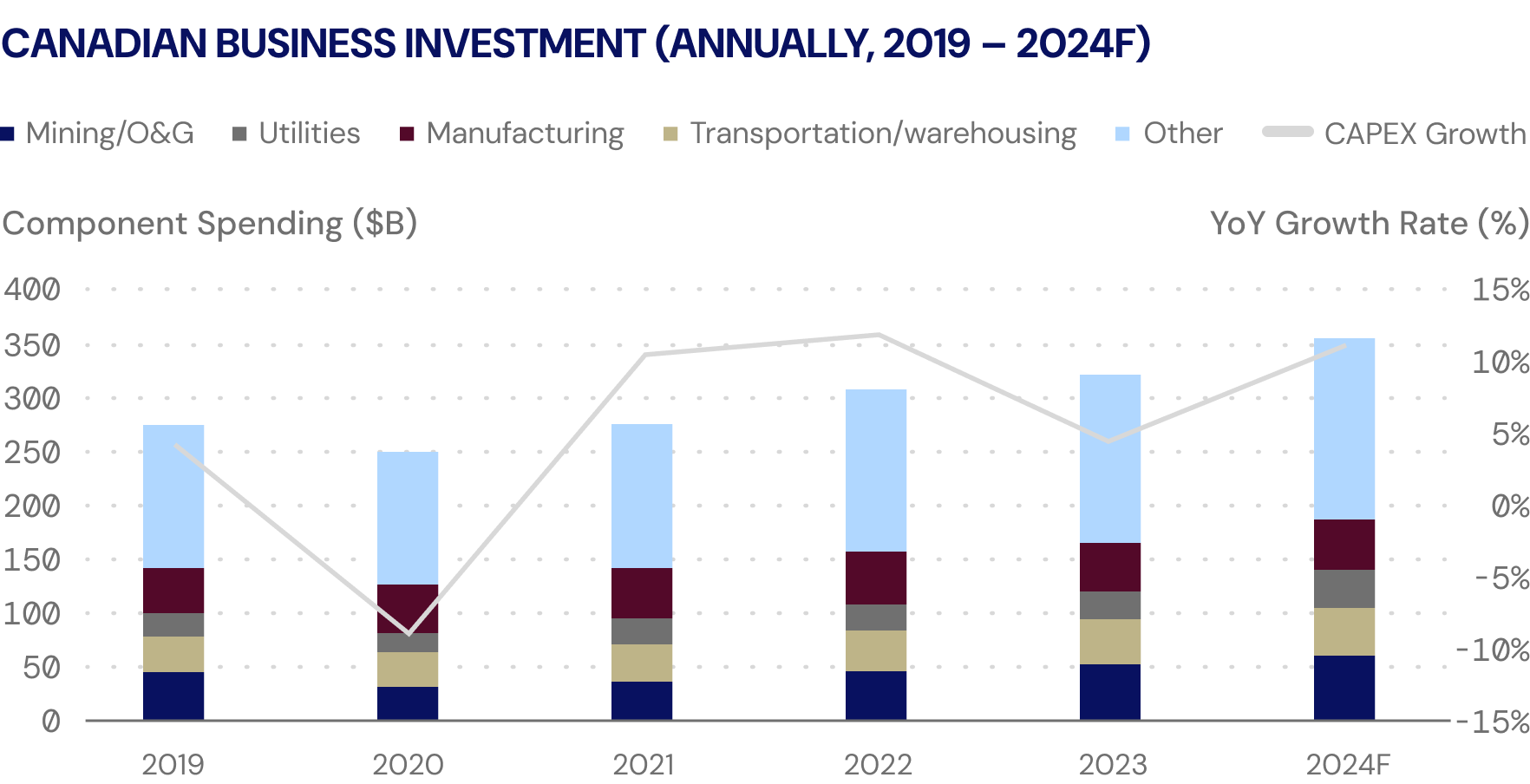

Business investment is expected to increase by 10.6% YoY in 2024F vs. 4.6% in 2023.

Business Investment Is Hot, Hot, Hot: Contrary to popular belief, aggregate business investment in Canada is poised to re-accelerate in 2024 to $354 billion (a growth rate of 10.6% YoY). Substantially all industries are expected to increase their capital expenditures, however Natural Resource Extraction (15% YoY Growth), Manufacturing (33% YoY Growth) and, surprisingly, Public Administration (10% YoY Growth) are leading the growth. We predict that delayed capital expenditures and projects are likely going to play a key role in the growth in business investment as the BoC reduces its policy rate.

Sources: Earning Reports, Statistics Canda, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.