The Silver Tsunami – Canada Needs These Businesses to Transition

Grab a life jacket as the tsunami of businesses for sale in Canada shows no signs of slowing. M&A deal values in Canada were up 43% YoY in 2025 despite the number of transactions being down 7% but still numbering over 3,000.

Canada is built on small–to-mid-sized businesses and to build back Canada we need to find a way to transition these businesses to the next generation. This is a trend we do not expect to slow but AI is creating new risks and opportunities that our friends at IJW & Co join us to provide street level intel on this month. With 76% of business owners indicating plans to retire over the next decade, over $2 trillion of businesses could transact.

Key Takeaways this Month:

- Canadian 2025 M&A Highlights: Mining drove a quarter of Canada’s M&A in 2025, with 803 deals totaling US$ 61.2 billion. While public valuations rose 18% YoY, private valuations stayed relatively flat and cash-at-close metrics fell to 72%, highlighting continued buyer caution and greater use of risk-sharing deal structures.

- Opportunities Are Coming: With over 20% of Canadians aged 55 and over a large wave of small business owners are approaching retirement and are looking for succession-driven ownership transitions.

- AI’s Impact on Software Valuations and Transaction Activity: AI is driving a reset in SaaS, with overall valuations compressing and a widening gap between AI-enabled/native and traditional. Deal activity remains active, but more selective, with buyers focused on more than just growth at any cost. While AI introduces new risks, it also handsomely rewards companies that embed AI into core workflows and align pricing outcomes.

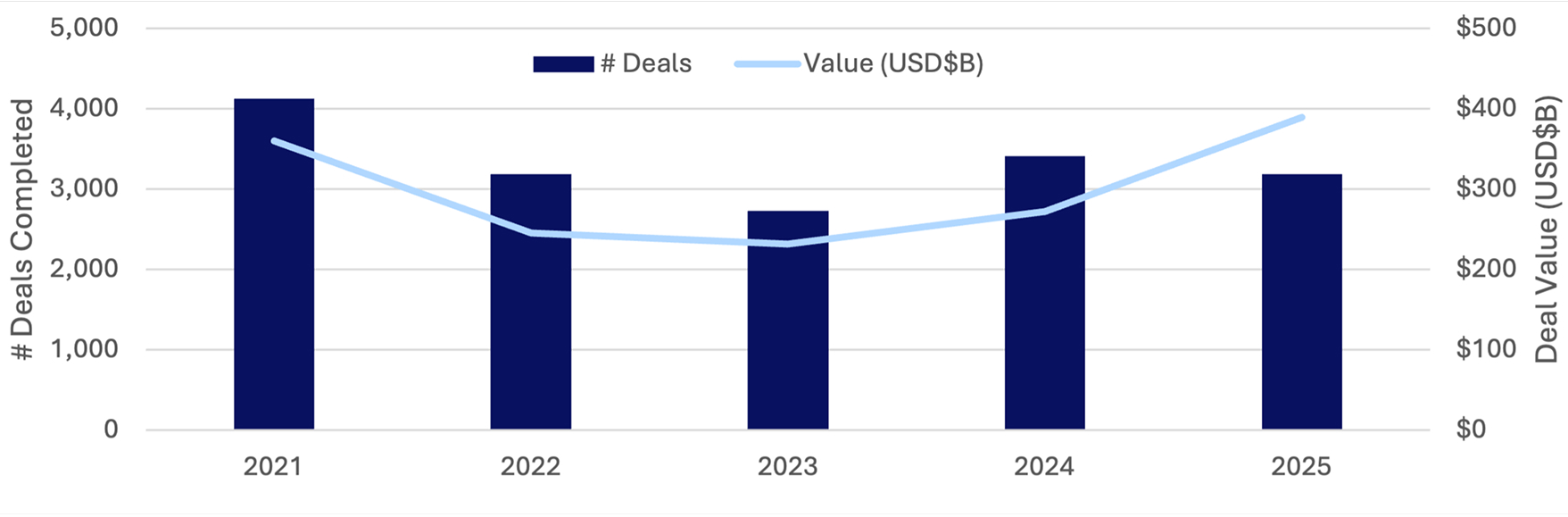

CANADIAN M&A DEAL ACTIVITY

Canadian M&A activity reached USD$390B in value across 3,184 deals in 2025 reflecting a 43% increase in value and a 7% decline in deal volume.

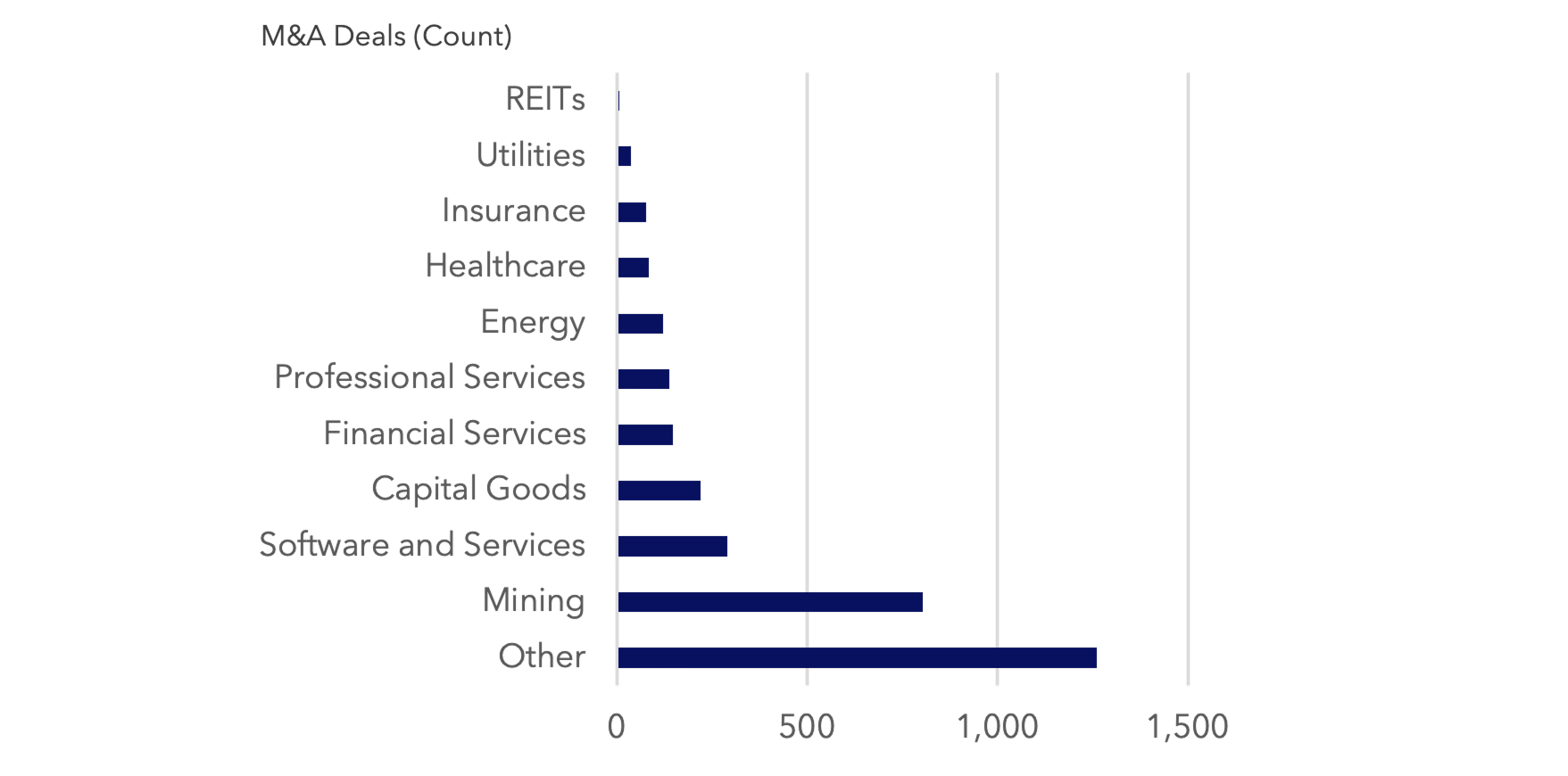

2025 M&A ACTIVITY BY INDUSTRY

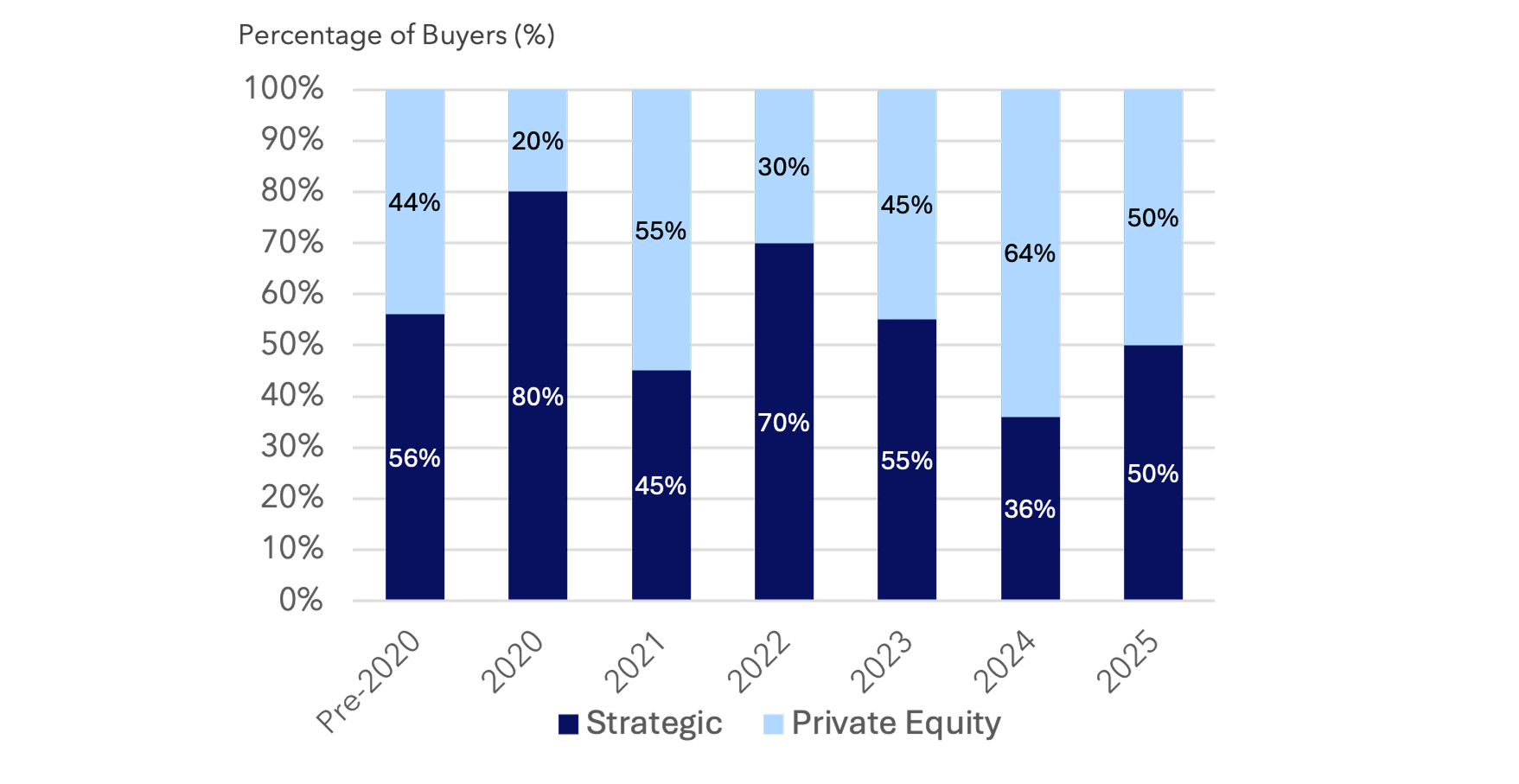

TRANSACTION BUYER PROFILE

Mining made up 25% of Canadian M&A in 2025, with 803 deals totaling USD$61.2B. Buyer activity was balanced, with both PE and strategics deploying capital.

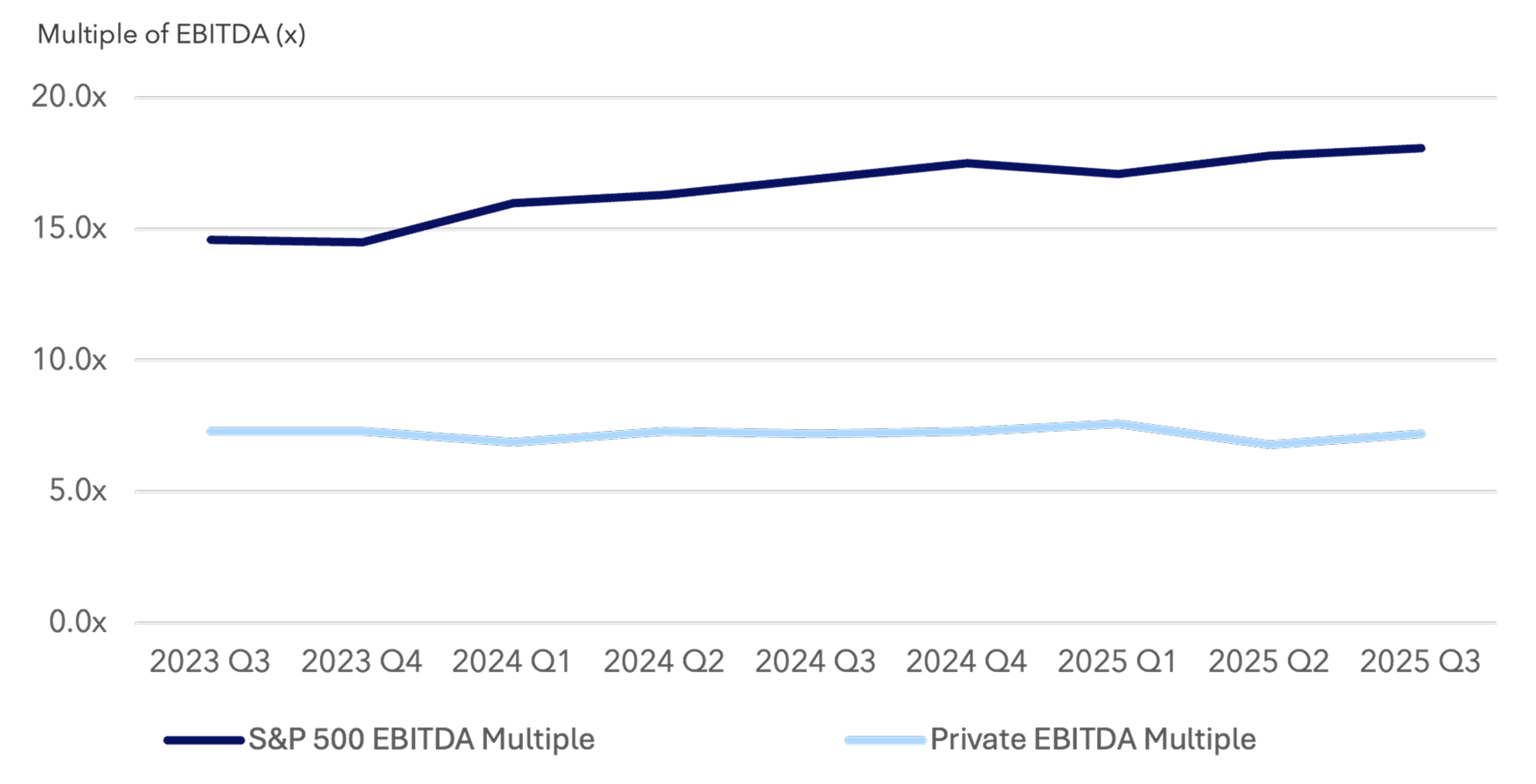

PUBLIC VS PRIVATE VALUATIONS

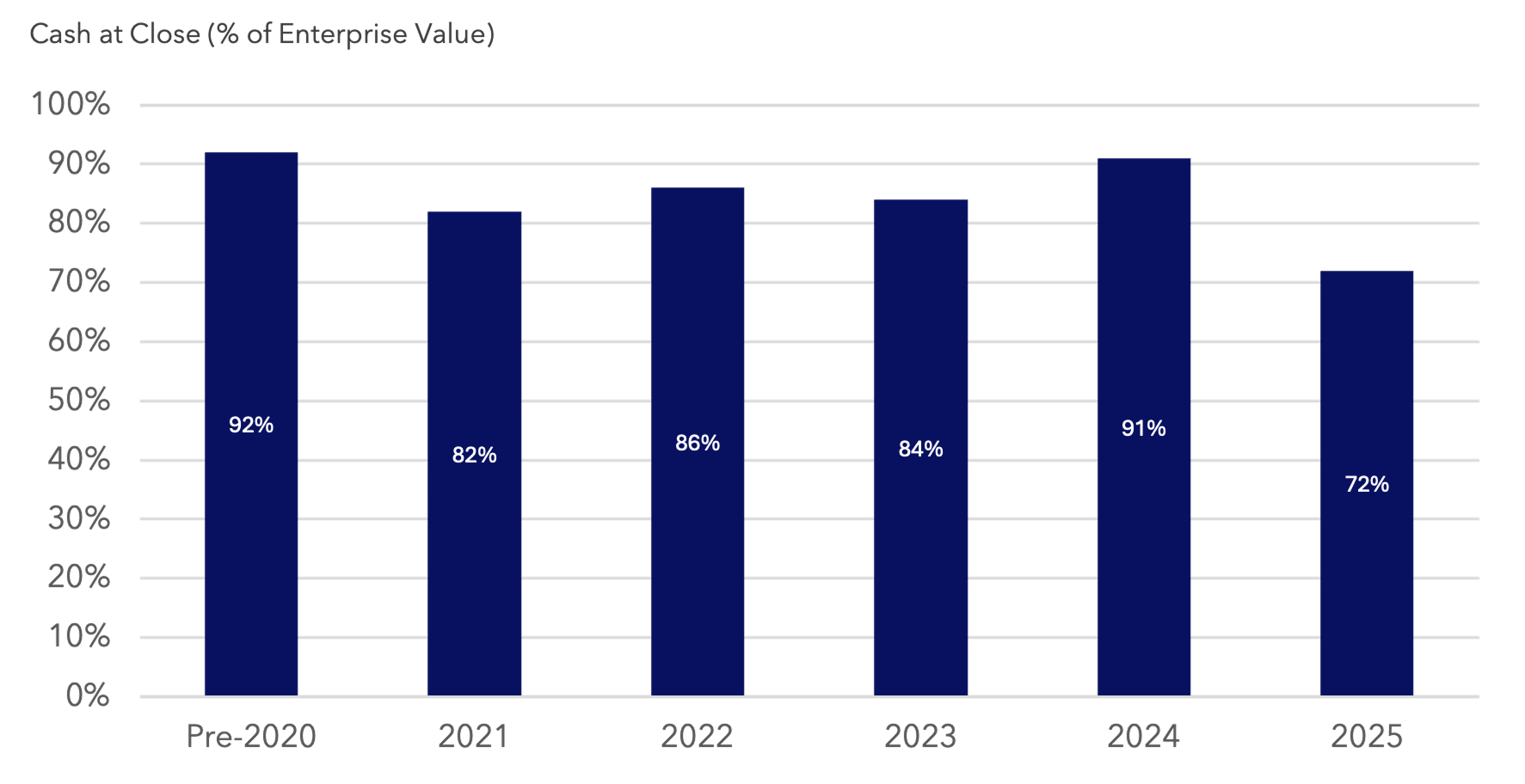

CASH AT CLOSE ON COMPLETED DEALS

While public valuations continue to climb (up 7% YoY), private valuations were flat YoY. Interestingly, cash-at-close declined to 72%, underscoring heightened risk mitigation priorities for buyers and an increase in the use of risk-sharing structures.

Street Intel From IJW & Co onAI’s Impact on Software Valuations and Transaction

IJW & Co is an investment bank focused on software and consumer services businesses who have agreed to provide the below insights on the current impacts of AI in the software space.

- Valuations: Valuations are compressed overall, but a clear divide is emerging between AI-enabled tech (commanding premiums) and traditional, seat-based SaaS businesses. While deal activity remains robust, buyers are placing greater emphasis on usage, defensibility, and margin durability.

- New Risks: Pricing model disruption (shift to usage-based), margin pressure from AI costs, and faster commoditization. These are all risks playing out in real-time, creating downward valuation pressure.

- New Opportunities: Companies that embrace outcome-based pricing, leverage proprietary data, and automate workflows are best positioned to drive growth and outperform in a more disciplined valuation environment.

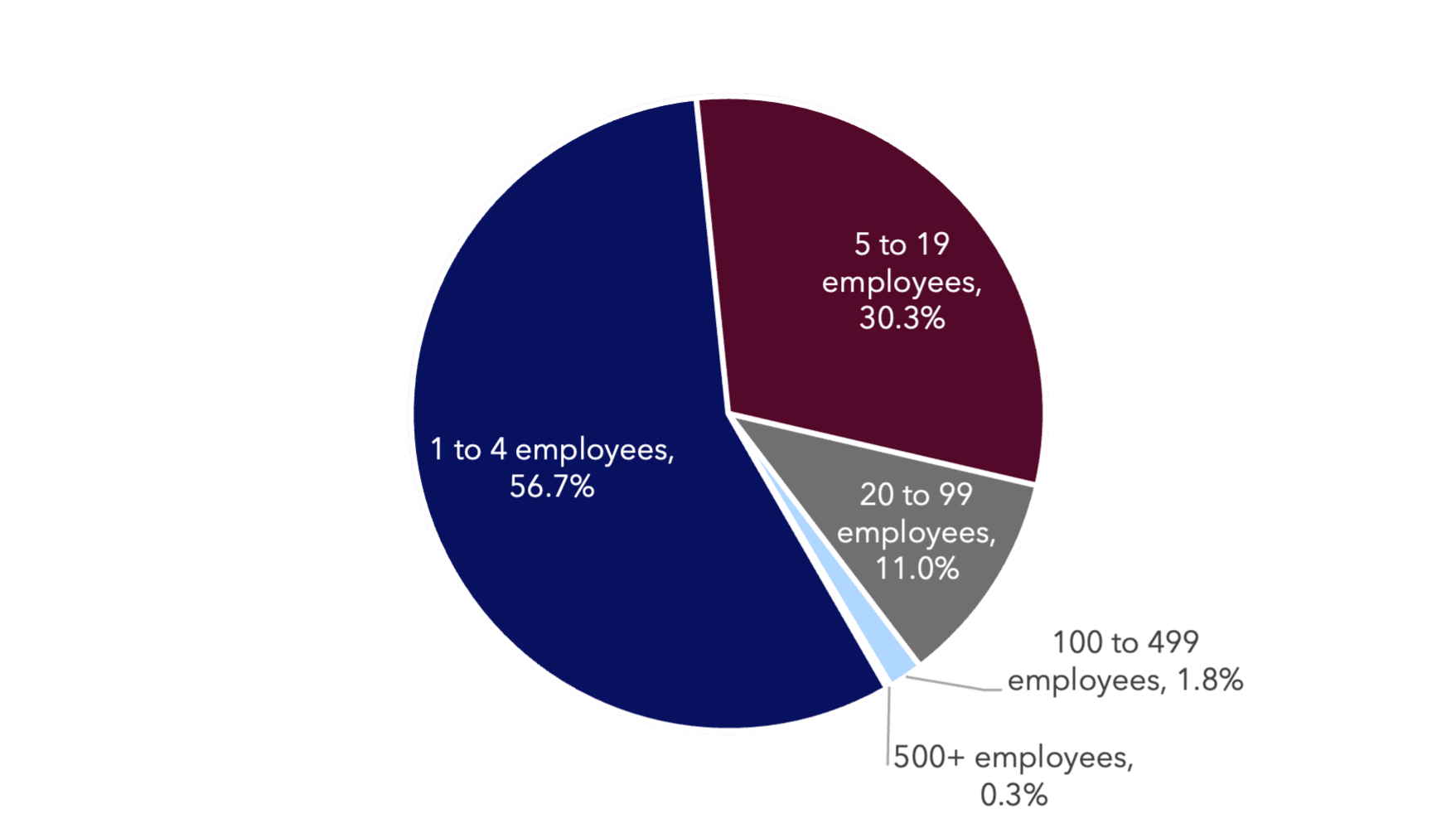

CANADIAN ACTIVE BUSINESSES BY EMPLOYEE COUNT

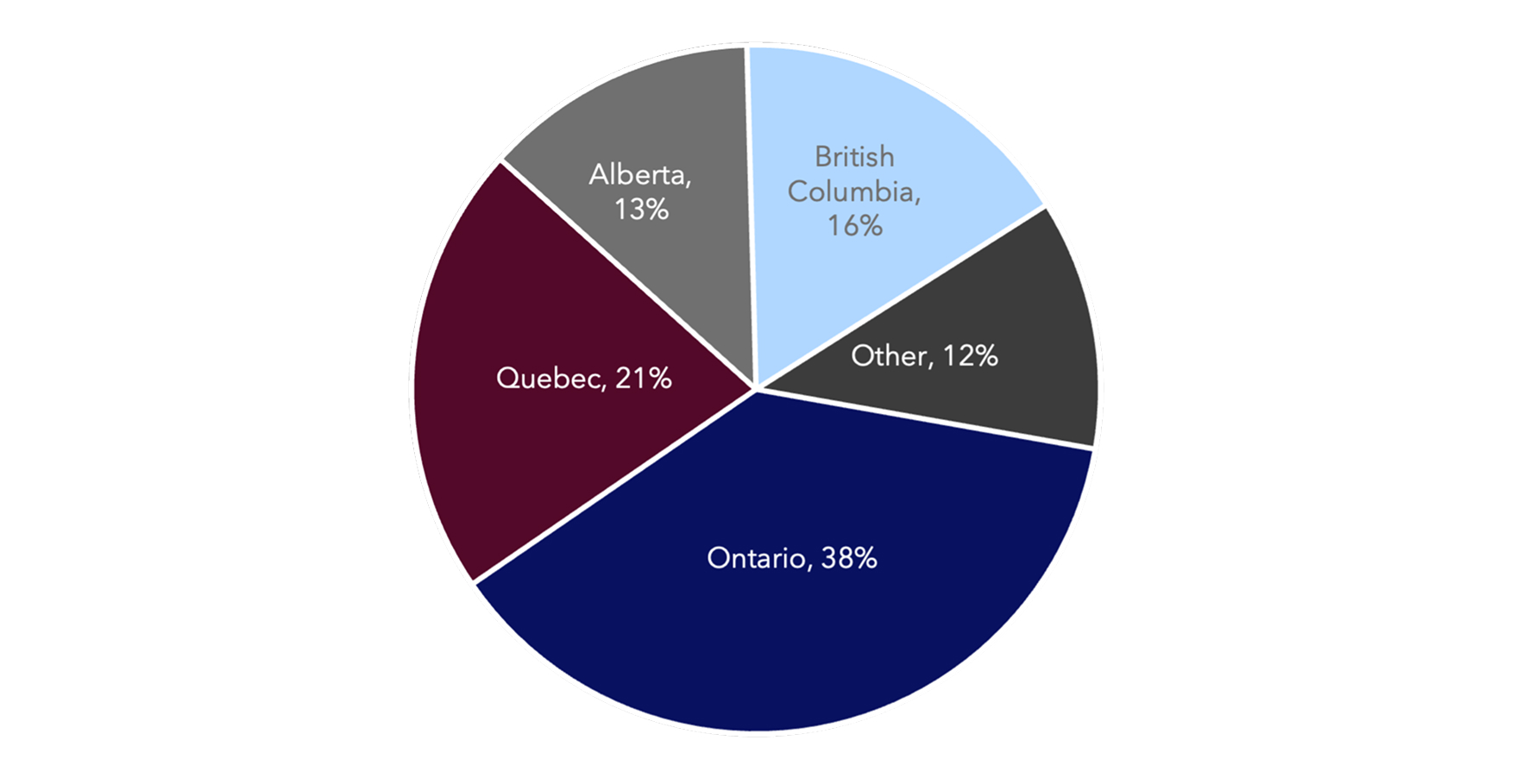

CANADIAN ACTIVE BUSINESSES BY PROVINCE

Approximately 98% of active businesses in Canada are between 1-99 employees, with AB, BC, ON and QB being key geographies for M&A as they hold 88% of all active businesses

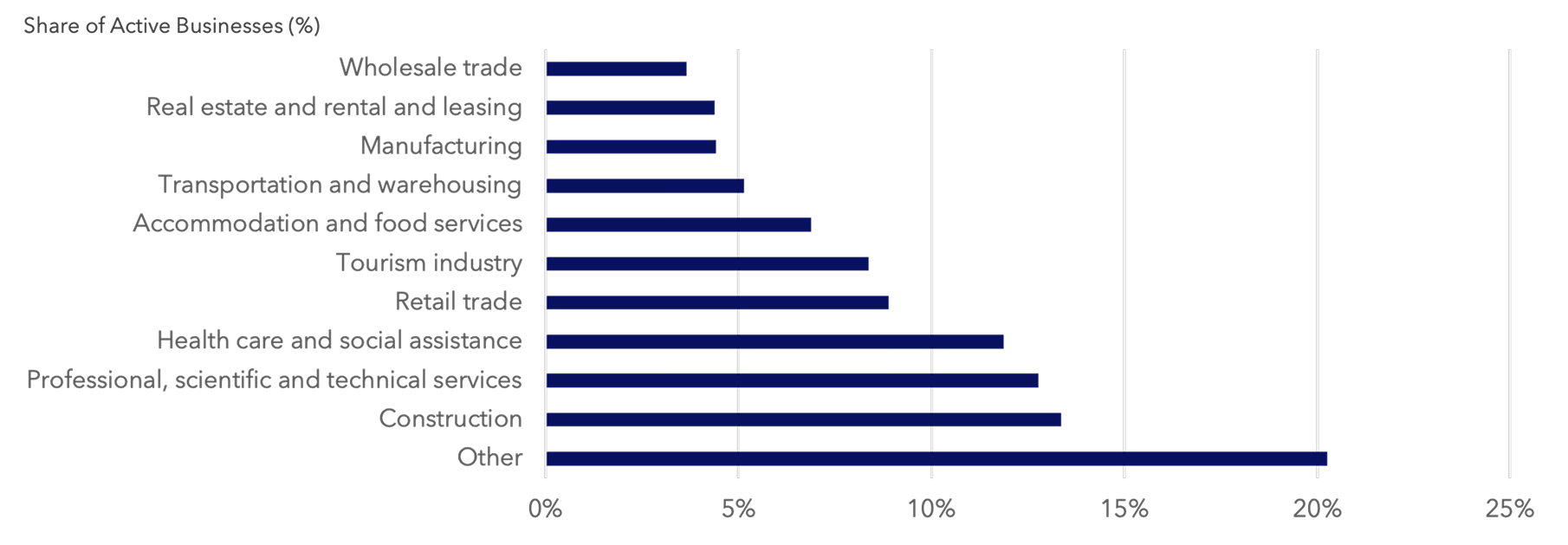

SHARE OF CANADIAN ACTIVE BUSINESSES BY INDUSTRY

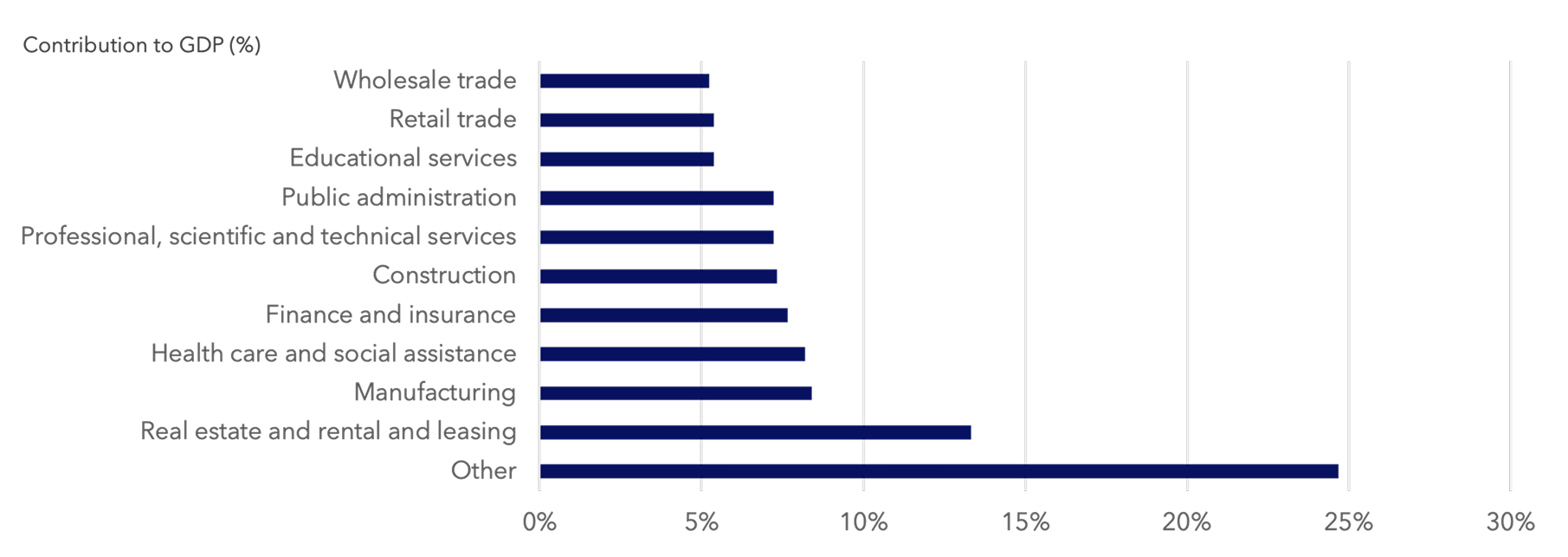

CONTRIBUTION TO GDP BY CANADIAN INDUSTRY

While construction, professional services and healthcare account for 38% of active businesses in Canada, the real estate, manufacturing and healthcare industries account for 30% of GDP.

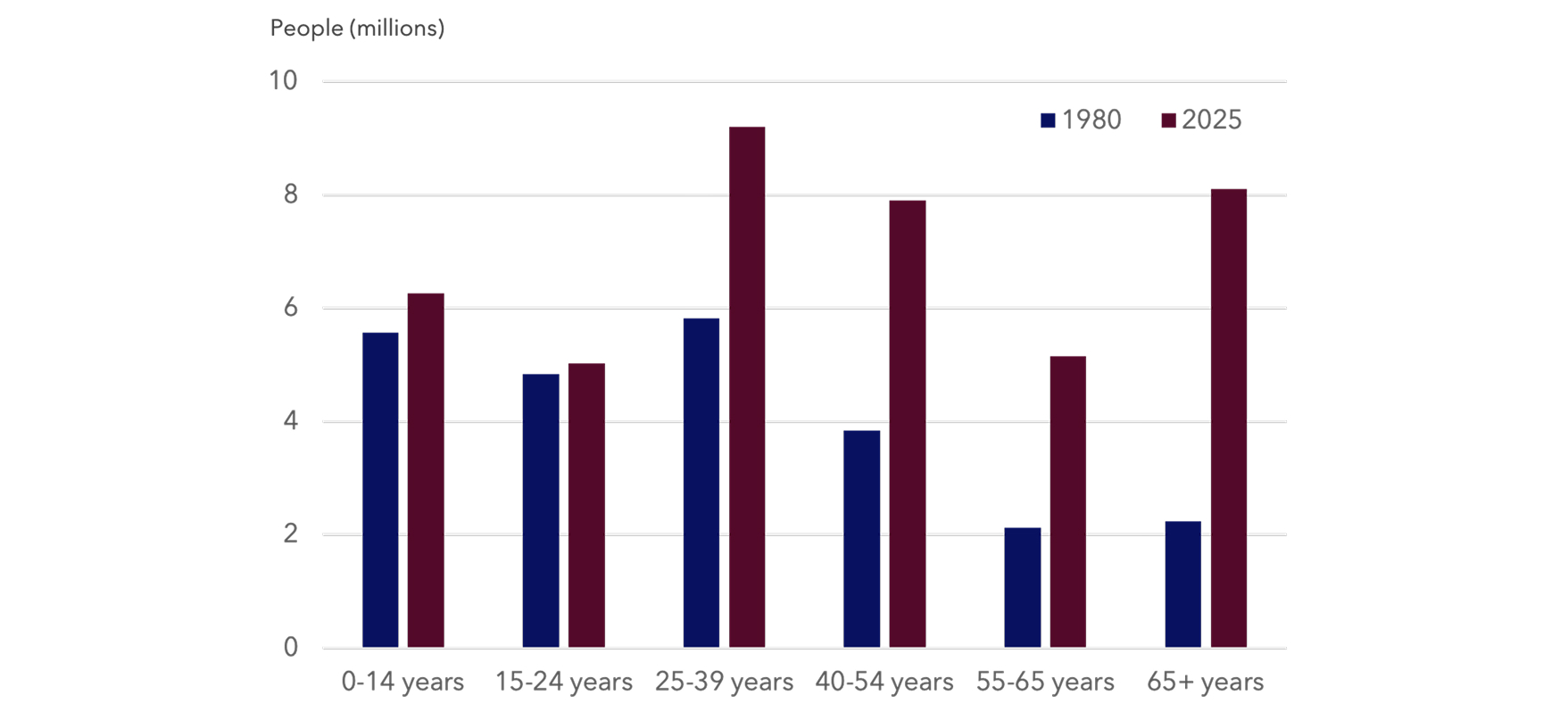

CANADIAN POPULATION BY AGE

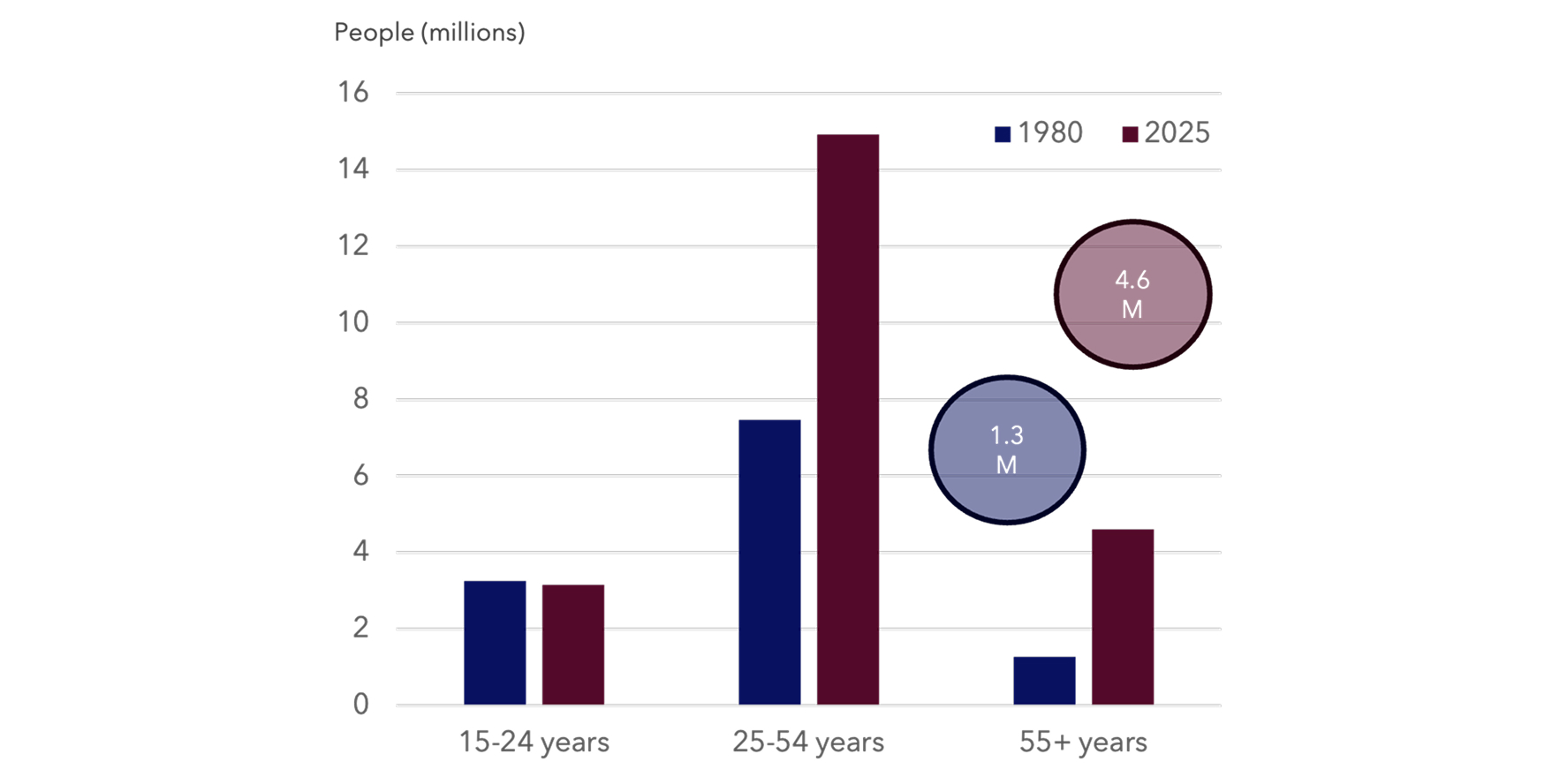

CANADIAN LABOUR FORCE

With over 20% of Canadians aged 55 and up, many small businesses are set for ownership transitions setting the stage for continued strength in the Canadian M&A market.

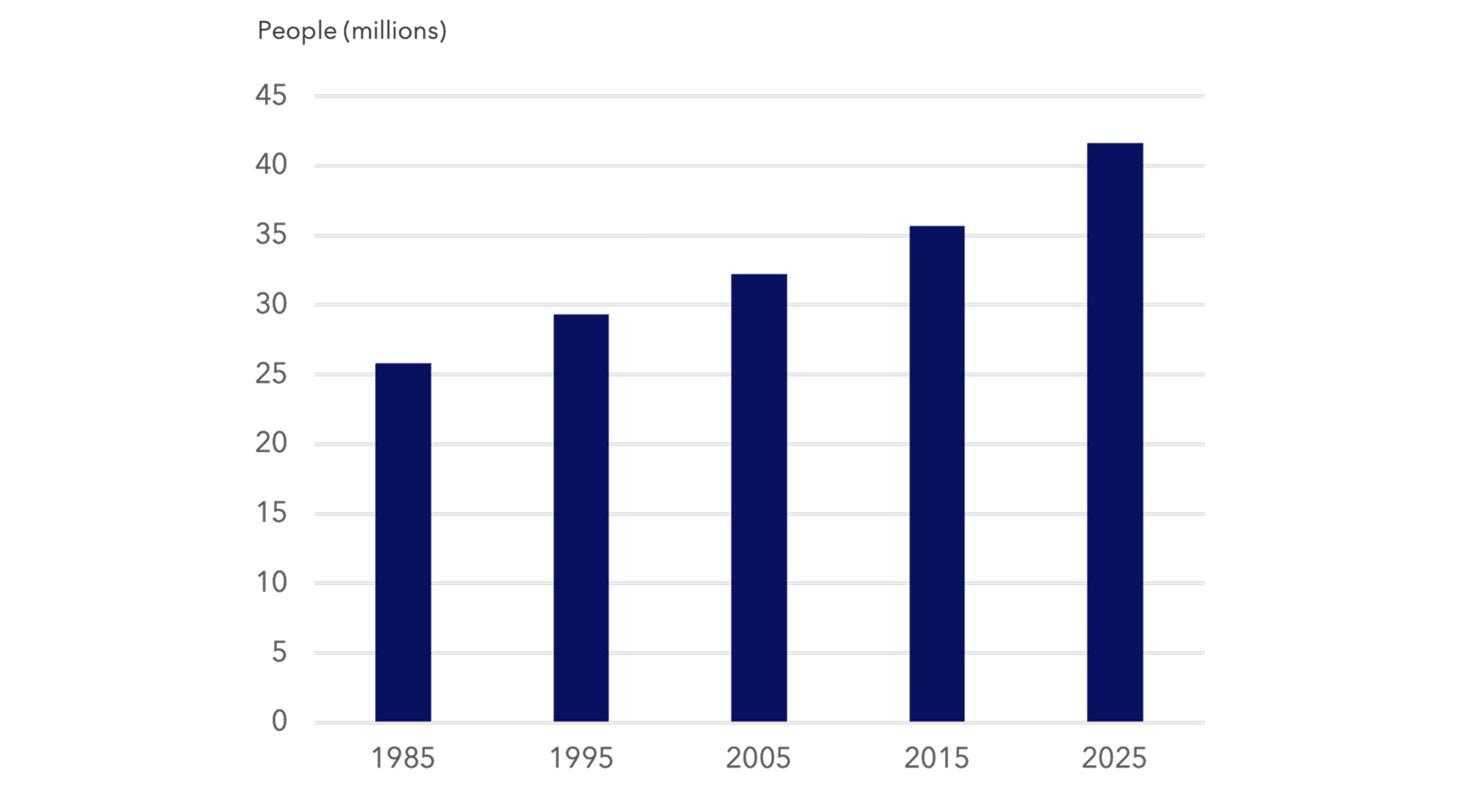

CANADIAN POPULATION

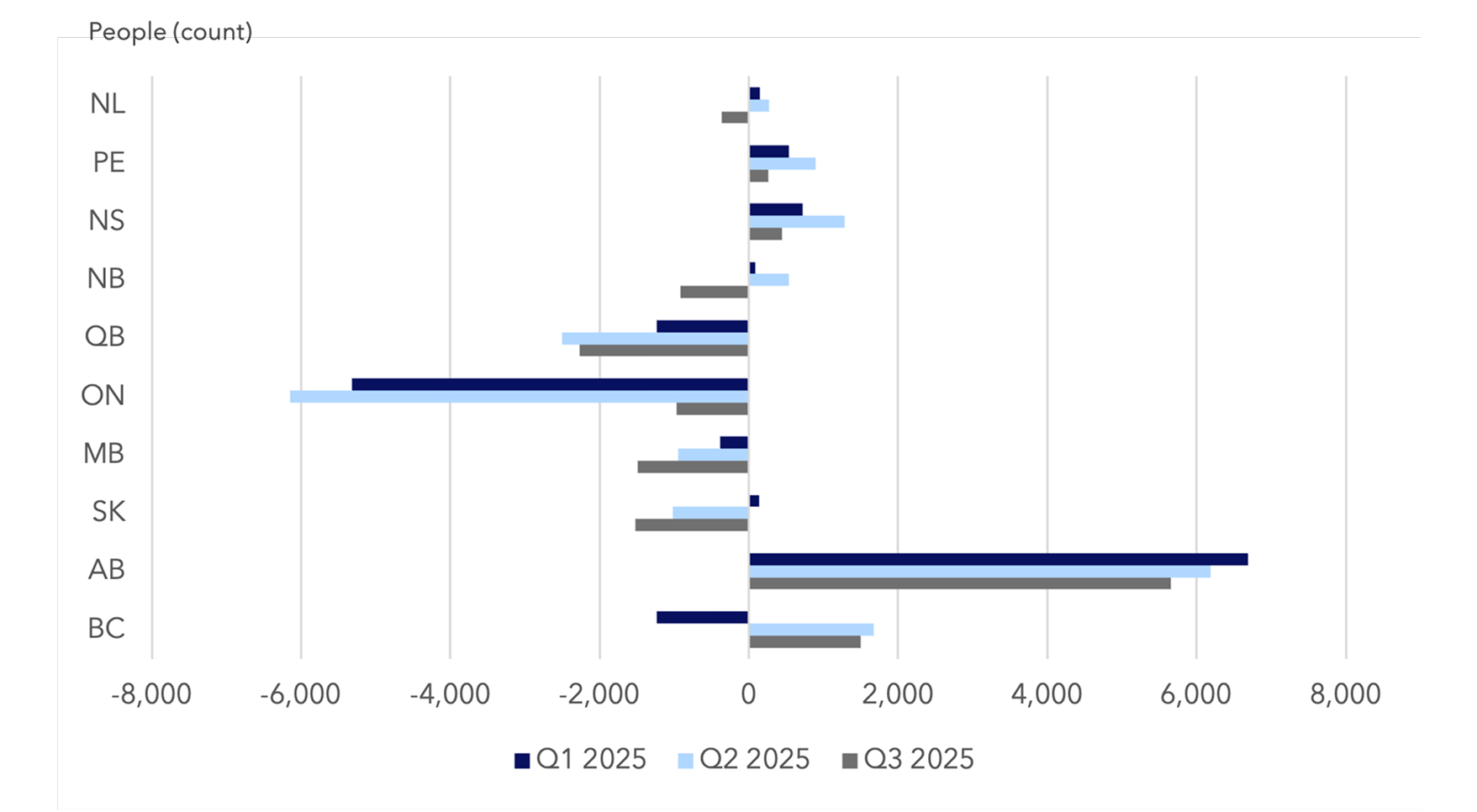

WHERE IS EVERYONE GOING: ALBERTA

Recent Government initiatives aim to slow the rapid population growth in Canada. Alberta continues to see the greatest growth, but service levels have been negatively impacted.

Additional Resources on M&A, Debt Financing, Software, & Consumer Products Can Be Found Here.

Source: RBC, CapIQ,GF Data, Statistics Canada, Diamond Willow

The Debt Digest lands in your inbox each month.