April 2023

MACROECONOMIC CONDITIONS MAY BE MIXED, BUT LONG-TERM FUNDAMENTALS LOOK GOOD FOR OWNERS, NOT SO MUCH FOR RENTERS.

There has been nothing ‘normal’ or ‘typical’ about the Canadian real estate market since the start of the COVID-19 pandemic (can we label it ‘crazy’?). More recently, the Bank of Canada’s rapid rate increases had a corrective impact on various regional markets throughout the country – in fact, the aggregate decline in property values in Canada currently stands at approximately -10%.

That said, the Government of Canada’s mandate to increase immigration to ~435,000 people per year is a driving macroeconomic force in the real estate sector that likely supports long-term home values.

KEY TAKEAWAYS THIS MONTH:

- Interest rate raises have had a negative impact on residential home prices but this could be levelling out

- Longer term, demand is outstripping supply as immigration levels continue to remain strong which should be supportive of prices

- Although lenders remain supportive of the real estate market, their appetite for growth is slowing

- The supply/demand imbalance will likely keep rental rates higher for longer

THE BACKUP DATA

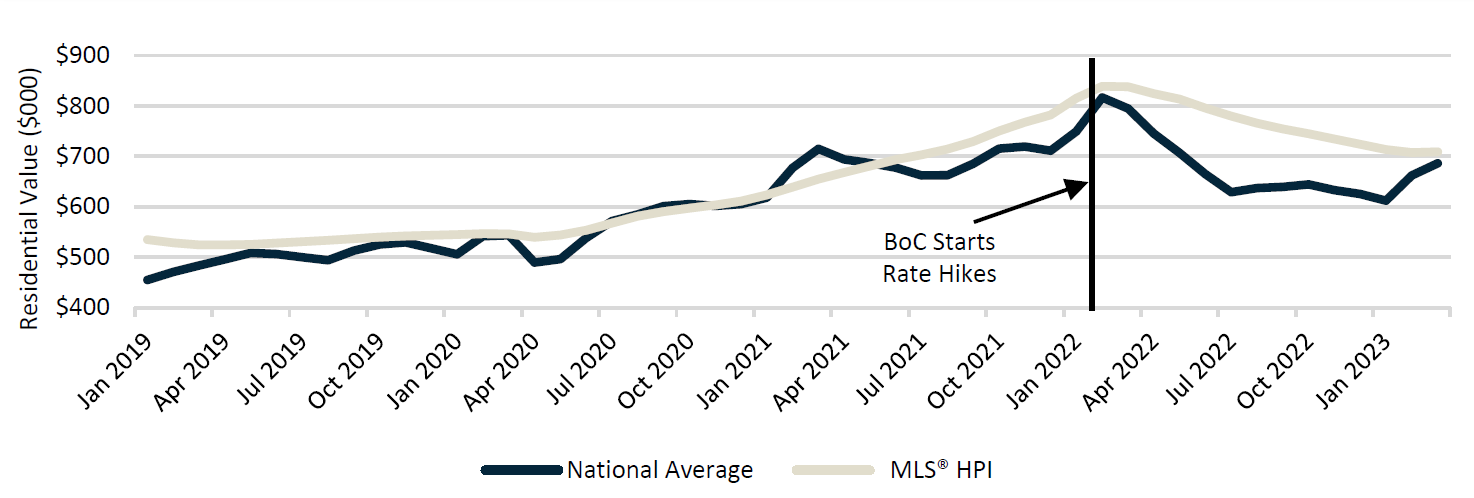

Recent Price Weakness May Be Plateauing: Across Canada, the average reduction in real estate values since the peak in May 2022 is approximately 10%. However, regional markets are mixed. Calgary (+8%), Edmonton (+2%) and Saskatoon (+2%) have shown resilience, while other markets like Toronto (-12%), Vancouver (-5%) and Victoria (-9%) have lagged. Interestingly enough, recent data suggests prices may be plateauing and even increasing in some markets. We believe this is being driven by a lack of supply and lower sales volumes.

Canadian Average Residential Price and MLS HPI: Jan 2019 - Mar 2023

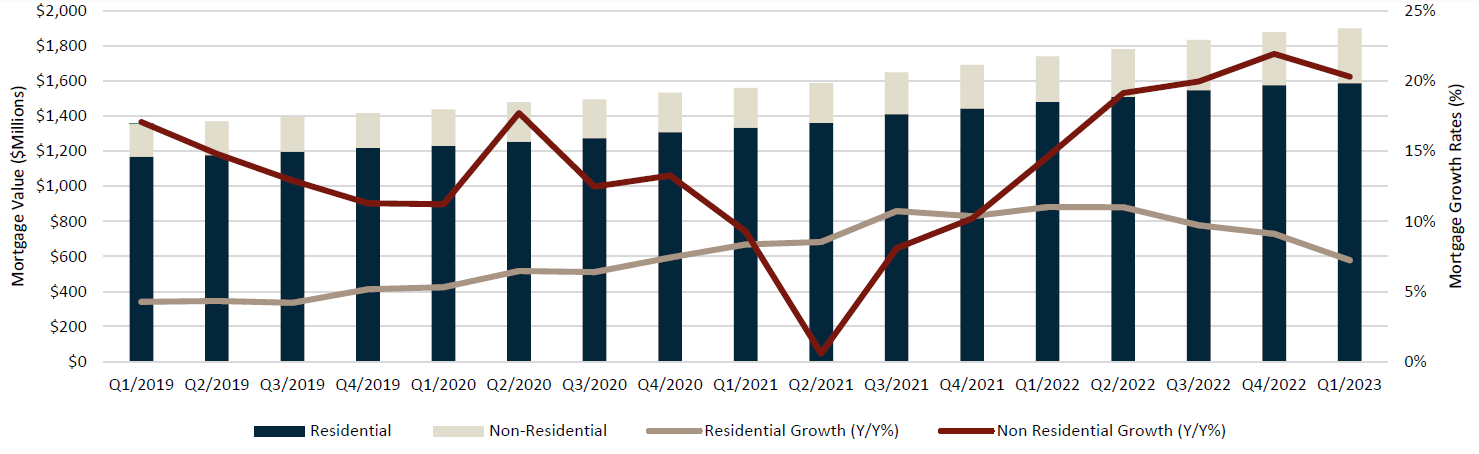

Canadian Residential and Non-Residential Mortgage Markets: Q1 2019 - Q1 2023

CANADIAN CREDIT MARKETS CONTINUE TO EXPAND, BUT AT A DECLINING RATE.

Similar to their commercial loan book, lenders across the nation are tightening their belts when it comes to mortgage underwriting activity. During Q1 2023, there was approximately $12B (+7% Y/Y, +0.7% Q/Q) in residential mortgages underwritten, while there was approximately $10B (+20% Y/Y, +3% Y/Y) in non-residential mortgages underwritten. Although still growing, the declining trend in residential mortgages is likely a result of both a reduction in price (-10% across Canada) and sales volume (-19% compared to pre-Covid). Non-residential mortgage growth has been robust since 2021 but is showing signs of slowing.

A NOTE ON CONVENTIONAL MORTGAGE RATES vs. CANADIAN PRIME.

During December 2022, the Canadian Prime Rate (currently 6.7%), which measures the interest rate charged to individuals of the highest credit quality, overtook the 1, 3 and 5-year conventional mortgage rate (currently 6.3%, 6.1% and 6.5%, respectively). The last time this phenomenon occurred was leading up to the housing crash in the early 1990 –we will be keeping a close eye on this trend.

CANADA HOUSING SUPPLY METRICS: Q1 2018 - Q4 2022

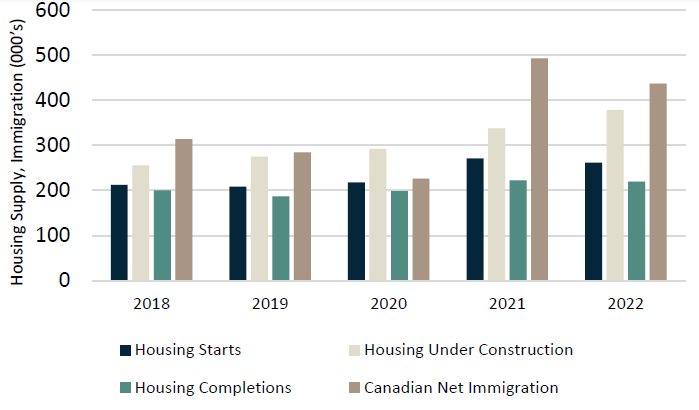

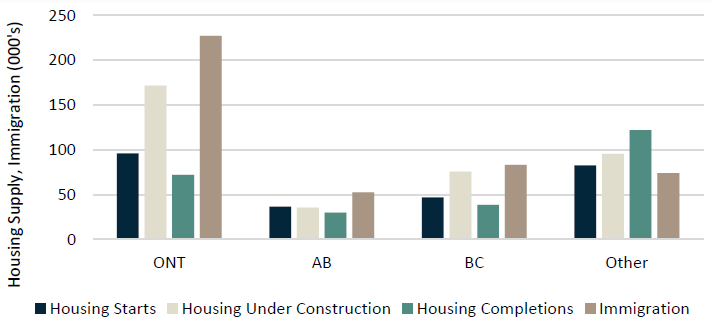

Housing Supply Metrics vs. Immigration, Annual

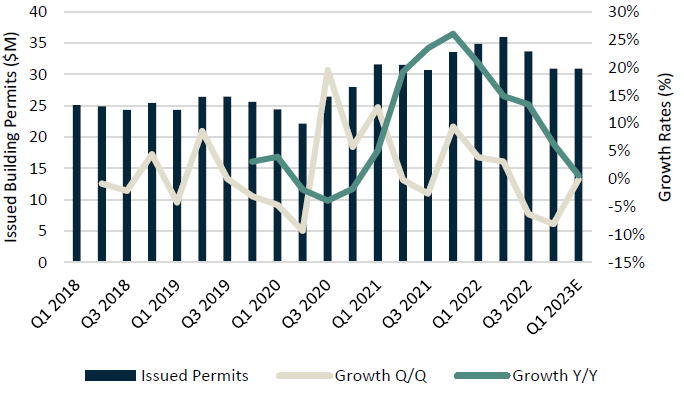

Canadian Building Permits Issued, Quarterly

HOUSING SUPPLY GROWING, BUT STILL BELOW DEMAND ON NATIONAL LEVEL.

At a high-level, immigration continues to grow at a CAGR of 8.7%, while the housing supply (starts, under construction and completions) is only growing at a 6.5% CAGR. In the short term, this inequality appears to be continuing with immigration levels, which stood at approximately 437,000 in 2022, far outweighing housing completions, which stood at approximately 220,000 in 2022. There are some early signs/successes to address this inequality. Housing projects under construction grew at a rate of 12% in 2022, while immigration growth remained largely flat –this will likely help normalize housing dynamics in the national market, and we will continue to monitor this trend. Further, building permits issued for residential and non-residential projects reached a cumulative value of $135 million (approximately +6% Y/Y). However, there are two interesting trends to monitor: (1) it appears that issuance of building permits has stalled and (2) building permits for non-residential projects are beginning to outgrow residential projects.

REGIONAL HOUSING SUPPLY / DEMAND SNAPSHOT, SELECT MARKETS

Housing Supply Metrics vs. Immigration, 2022

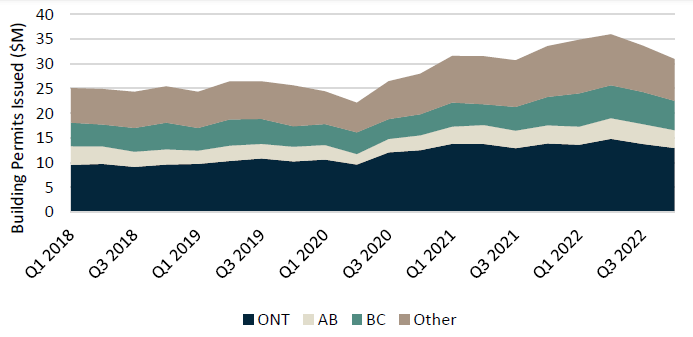

Building Permits Issued by Province, Quarterly

REGIONALLY, THERE ARE STRUGGLES AND OPPORTUNITIES.

Regional markets vary across the nation, as reflected in recent price action. At a high-level:

- Ontario: Considerable immigration continues to put a strain on housing, however there is a large backlog of approximately 171,500 units currently under construction as of Q4 2022. While this figure is still below the level of immigration (227,000), it does demonstrate some efforts to create equilibrium in the housing market compared to the past. Interestingly, Ontario is also following the trend of declining housing starts (down approximately 3.5% Y/Y and 12% Q/Q) which may reflect a supply constraint to not oversupply the market, or perhaps lack of building opportunities. We will continue to monitor this trend.

- Alberta: Alberta is in a state of growth, with an increased level of immigration (52,500 in 2022) beginning to put some strain on the housing market. Housing starts (36,500), housing under construction (35,500) and completions (7,800) reflect the need to build new housing to support immigration. This makes sense given Alberta was one of the only markets in Canada to not experience a material decline in housing prices, however it will be interesting to monitor this trend as housing units begin to appear on the market.

- British Columbia: BC is facing a similar situation to Ontario, whereby the current level of immigration (83,000 in 2022) is greater than new completions, but there is a backlog of housing units under construction (75,700). Housing starts are down 2.3% Q/Q and 1.9% Y/Y.

- Rest of Canada: Other regions in Canada are facing an over-supply of housing, with completions growing at a CAGR of 13% between 2018 and 2022. This trend has slowed down and construction of new projects are likely to subside in the near future with housing starts down approximately 10.5% Y/Y.

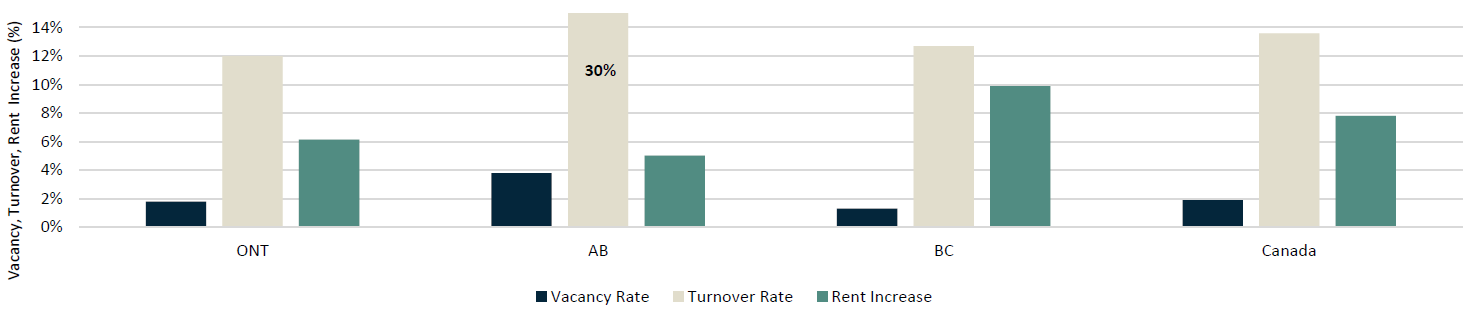

Canadian Rental Market, as of October 2022

IN A WORD, RENTAL MARKETS ARE ‘TIGHT’ ACROSS CANADA.

There is no relief in sight for renters –vacancy and turnover rates have declined in 2022, which was paired with a material (7.7%) increase in rental rates across the country. On a regional level, Ontario and BC continue to have historically tight markets as large levels of immigration impact vacancy and turnover, but Alberta is in an interesting state. Currently, Alberta’s vacancy rate has declined to 3.8% (compared to 6.8% during the prior year) while turnover has increased to 29.4% (compared to 28.4% during the prior year). There doesn’t appear to be any particular reason behind this deviation, aside from the fluctuations in migration and immigration to Alberta over the course of 2022 to match the ebbs and flows of the economic cycle. Rental rates have also increased, reflecting an increased cost to sheltering Canadians (+6.1%, 5.0% and 9.9% in Ontario, Alberta and BC, respectively.

Sources: Statistics Canada, Bank of Canada, CREA, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.