December 2020

KEY INDICATIONS FROM CANADIAN Q4 BANK RESULTS SUGGEST WORST MAY BE OVER FOR CREDIT ACCESS

Call us nerds, but we always look forward to the financial results from Canada’s largest financial institutions. The Schedule A Bank results provide a great indication of the ability for businesses to access the most inexpensive form of capital. Q4 results did not disappoint with our analysis leading us to believe that Canada’s banks are increasingly comfortable with their loan exposure despite the persistent economic headwinds.

The following are some of our key takeaways:

- Total commercial credit contracted – But not as much as we anticipated. Combined commercial credit in Canada (big 6 banks) contracted 3.8%, far better than the 6% we were expecting.

- Loss provisions nearly back to normal – Following suit with Q3’20 results, Q4 saw another significant reduction in provisional credit losses. On a combined basis loss provisions are nearly back to pre-COVID levels.

- Impaired loans reduced for 1st time since Q3/2019 – Reversing a worrying trend, total Gross Impaired Loans contracted for the 1st time in over a year with a meaningful 13% reduction vs Q3’20.

- Deferral programs are done – No real surprise here as it was well telegraphed but good to see the data support the rhetoric as commercial loan deferral programs are down 90% from Q3 levels across Canada.

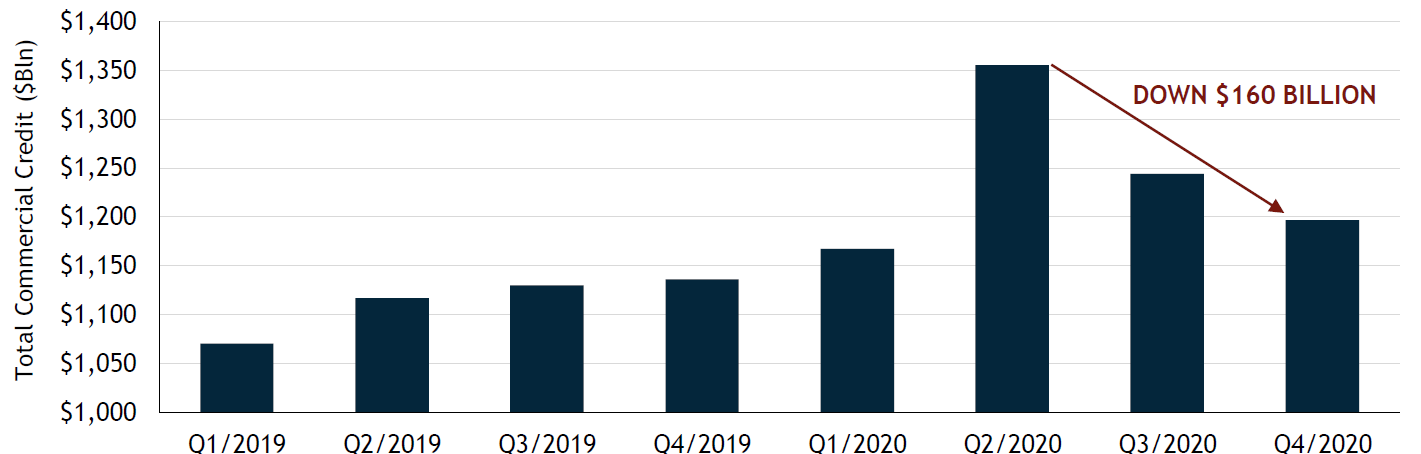

Total Commercial Credit Extended in Canada

TOTAL COMMERICAL CREDIT REDUCED AGAIN - BUT NOT AS MUCH AS EXPECTED

Accessing credit from Canada’s banks is still by no means easy as new clients tend to be those “down the fairway” type transactions. Having said that, we saw a 3.8% reduction in total commercial credit outstanding amongst Canada’s big 6 banks. This reduction amounted to $49 Billion less credit than the previous quarter (we were forecasting a $77 billion reduction), indicating $160 billion less commercial credit out than what we saw in Q2’20.

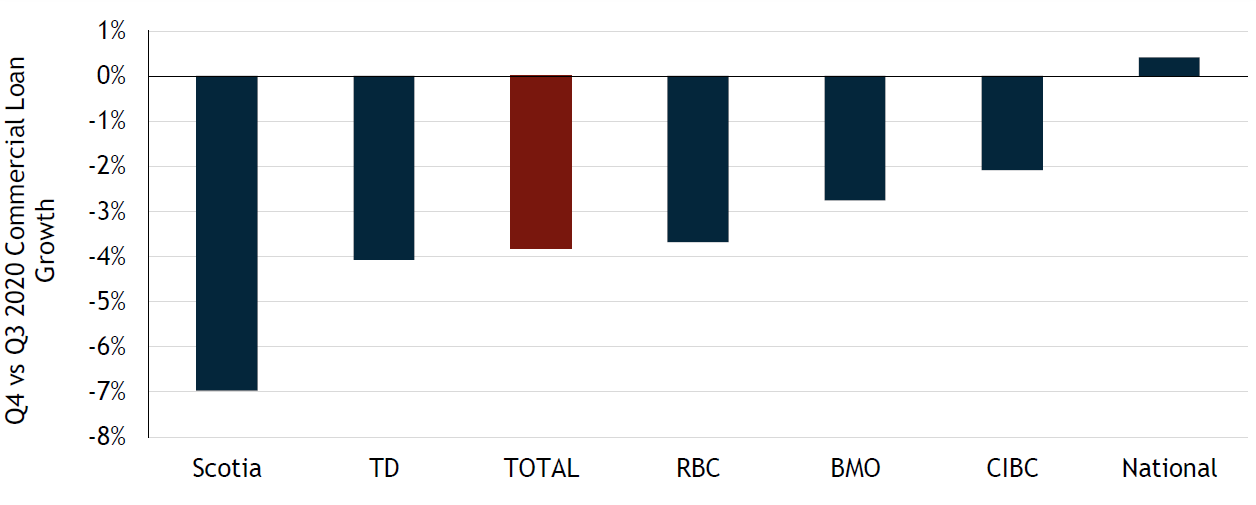

Q4 2020 vs Q3 2020 - Reduction in Commercial Credit

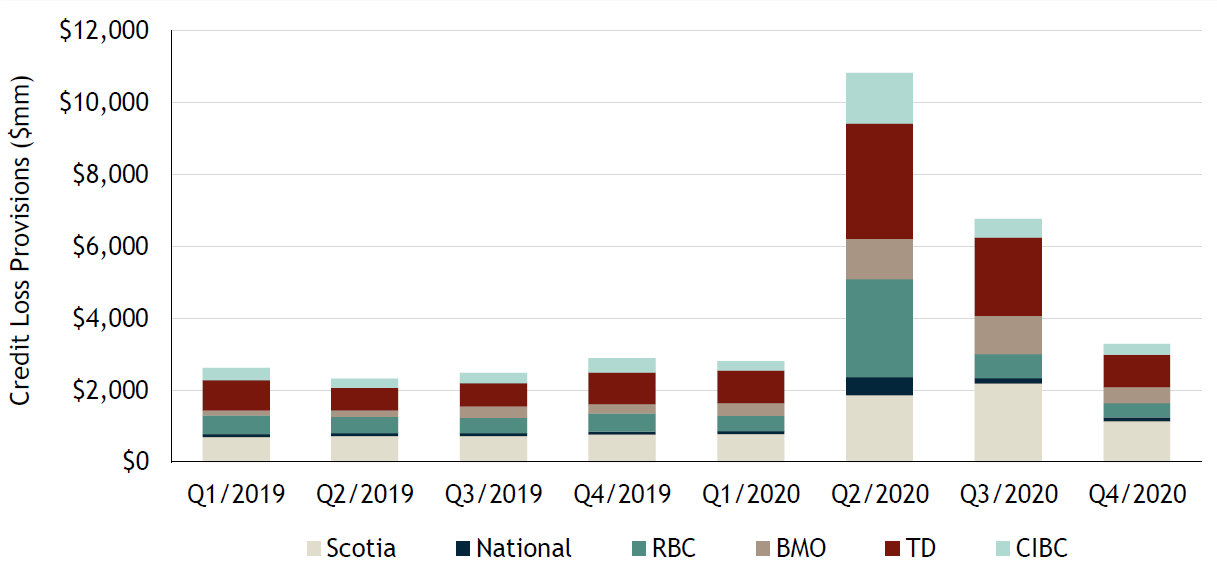

LOAN LOSS PROVISIONS NEARLY BACK TO PRE-COVID LEVELS

If there is any indication of the underlying comfort level from Canada’s top lenders, this is it. We were amazed to see combined credit loss provisions nearly back to pre-COVID levels on an absolute basis. It appears only ScotiaBank is remaining somewhat conservative with their loss provisions as the other lending institutions are largely back to normalised levels (in terms of loss provisions vs total credit outstanding).

Loan Loss Provisions Nearly Back to Normal

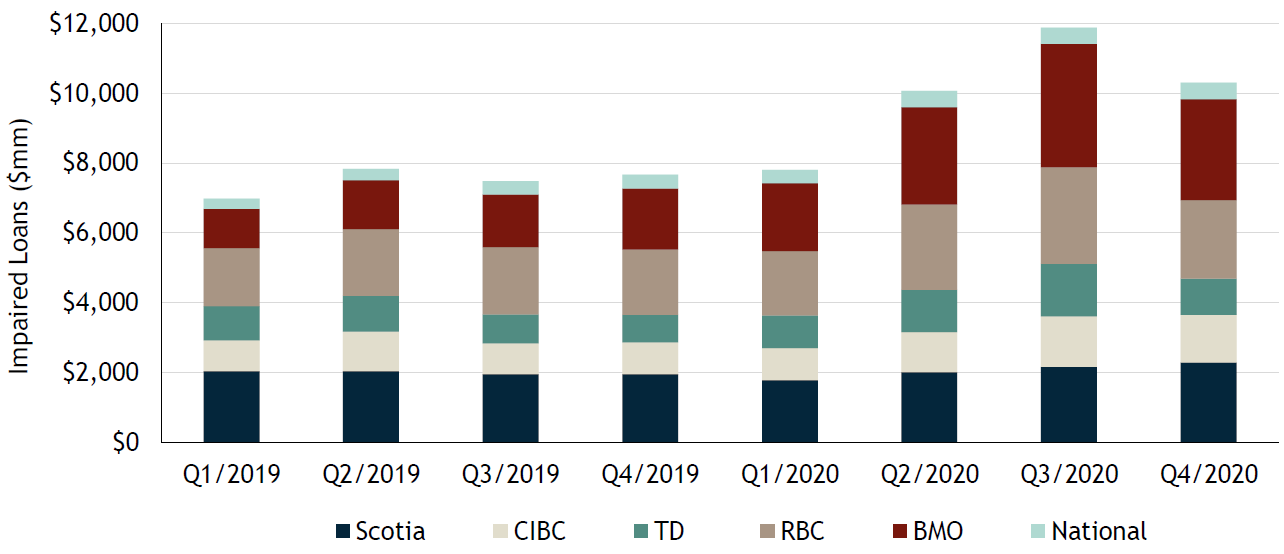

A NICE REVERSAL FOR IMPAIRED LOANS

Nice to see the reversal of a worrying trend as Gross Impaired Loans (GIL’s) contracted for the first time in a year with a 13% reduction versus what we saw in Q3’20. While the more “COVID Exposed” sectors such as accommodation, retail and some wholesale business are not seeing a material decrease in impaired loans. On the flip side, this quarter did see a significant drop (25%) in energy sector loans deemed impaired.

Impaired Loans Across Canada’s Banking Sector

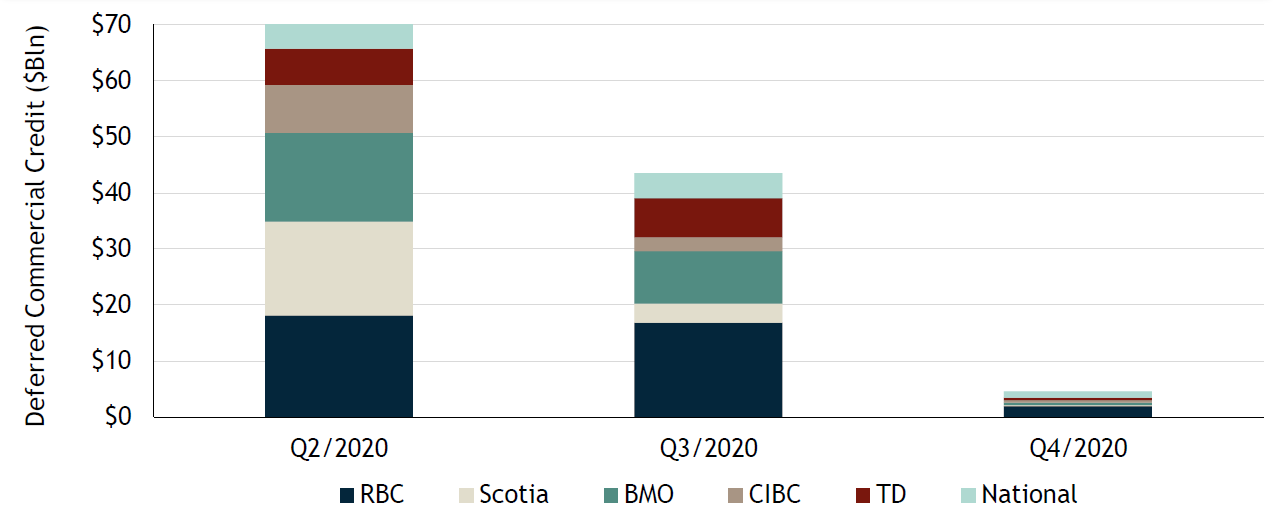

CREDIT DEFERRAL PROGRAMS ALL BUT DONE

In Q4, Canada’s banks indicated a total of $4.6 billion of commercial loan payments were still in the deferred category, representing a 90% decrease from Q3’20. This is a far cry from the $70 billion of commercial loans that were under a deferral program in Q2/20 suggesting Canada’s banks, in combination with Federal government support have successfully transitioned borrowers back to meeting their normal (i.e. Pre –COVID) debt servicing obligations. From what we can tell, of those that have transitioned back, only ~2% are delinquent on their payments.

Commercial Credit Deferral Comparison

Sources: Company Reports, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.