December 2021

IN THIS ISSUE:

- We emphasize that in times of business uncertainty, the best line of defense is a well capitalized balance sheet. Either raising equity or restructuring debt can have a material impact on business risk.

- We highlight some of the interesting points relating to the global supply chain which is showing no sign of easing up from high-levelel perspective.

- Inflation will certainly be impacted by the dysfunction in the global supply chain, among other things. We have a quick look at some of the main drivers behind the increase in the CPI with food and energy leading the way higher.

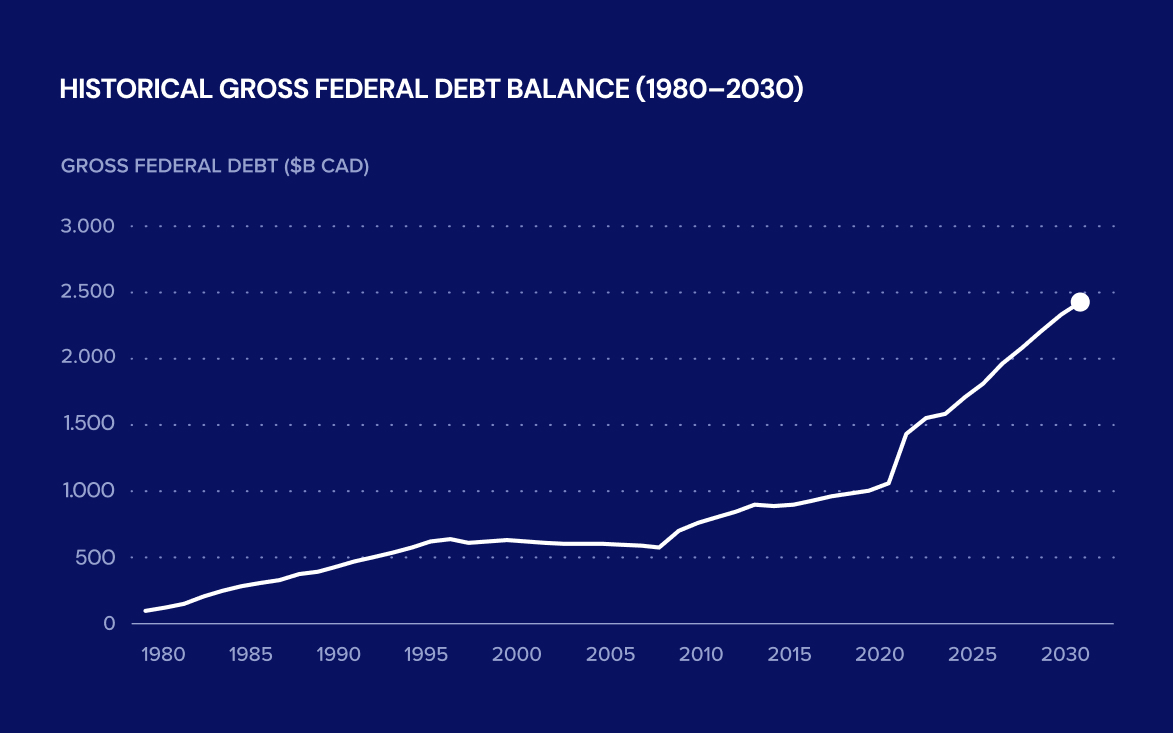

A STRONG BALANCE SHEET WILL HELP NAVIGATE UNCERTAINTY

Whether we are talking supply chain risk, inflation risk, or simply getting enough workers so your business can function normally, there is more than enough uncertainty to go around these days. While we wish we had a crystal ball that could provide us some clarity, no such luck. In times of business uncertainty, the best line of defense is a well capitalised balance sheet. Needless to say, the correlation between the ability to withstand business risk and balance sheet strength is about as perfectly correlated as one can get.

To ground this notion in reality, we are not suggesting all companies rush out and raise equity, as this is unrealistic for many. What we are suggesting is that companies take a hard look at how their business is capitalised and see if there is any wiggle room. More specifically, the path of least resistance might be to restructure debt obligations. Extending an amortisation period or securing an interest only period are two examples that have a significant ability to reduce the cash flow pressure of debt obligations and effectively recapitalise the balance sheet in the process.

Supply chain headwinds and inflation risk are two topics that have been beaten to death and explored by many individuals, who are much smarter than us. Having said that, with all the “research” into the respective topics, there is little clarity on, i) how long they will last and, ii) how severe they will become.

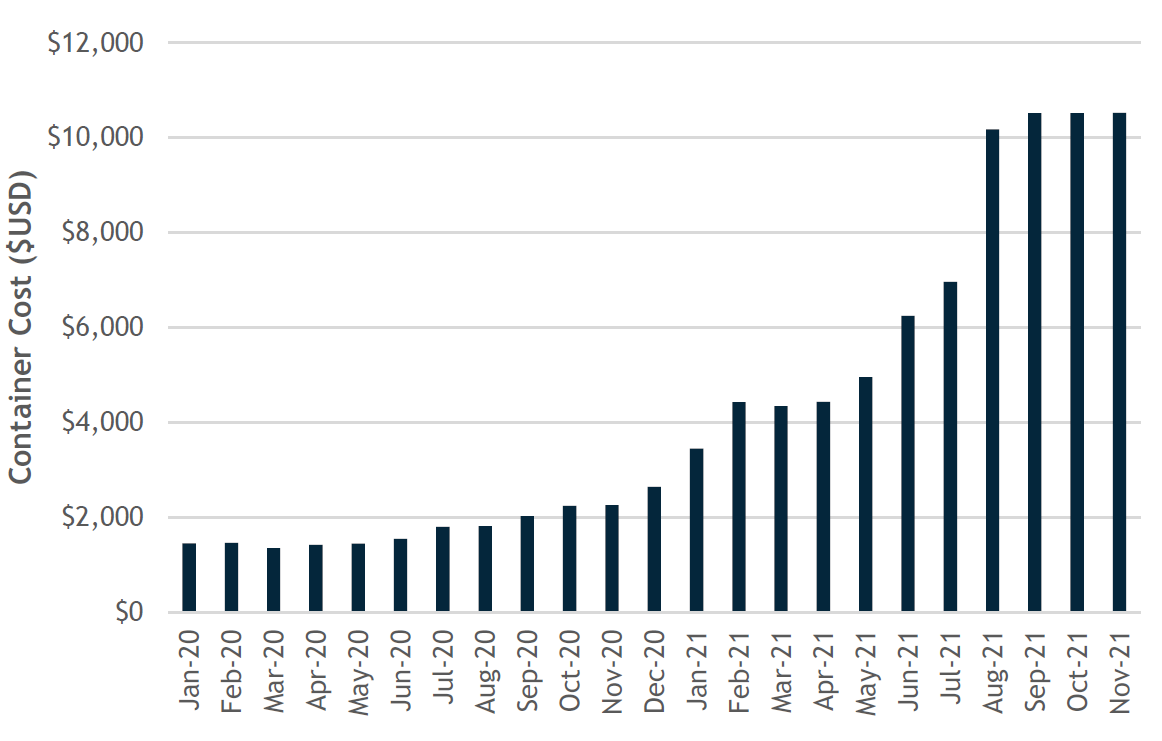

Freightos Global Container Freight Index

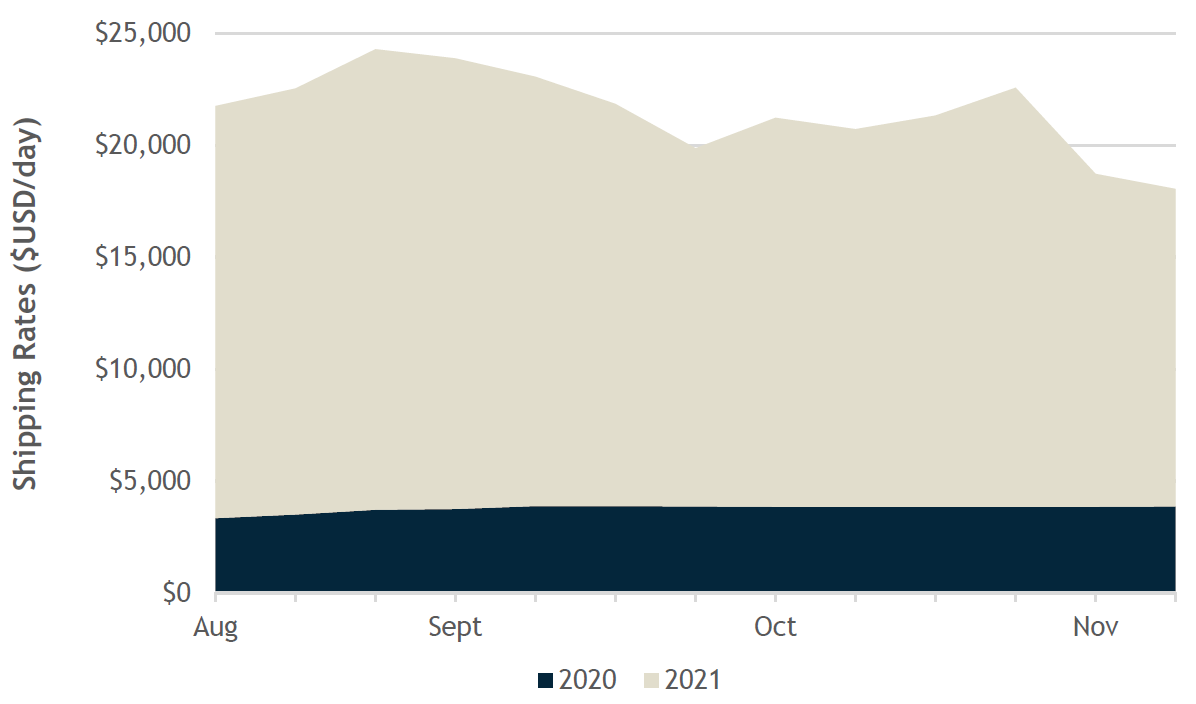

SHIPPING RATES OFF PEAK BUT STILL SCARY HIGH

Comparing year over year shipping rates gives some real perspective on how far away we are from “normal” when it comes to the bulk shipment of goods. The 2020 run rate cost would fall into the USD $2,500 range with peak September 2021 rates coming in nearly 10x higher. Rates have now fallen sub $20,000/day but given the backlog at the ports, its safe to say the absolute costs of moving product on ocean barges is going to remain expensive for a very long time.

Year over Year Shipping Rates Comparison

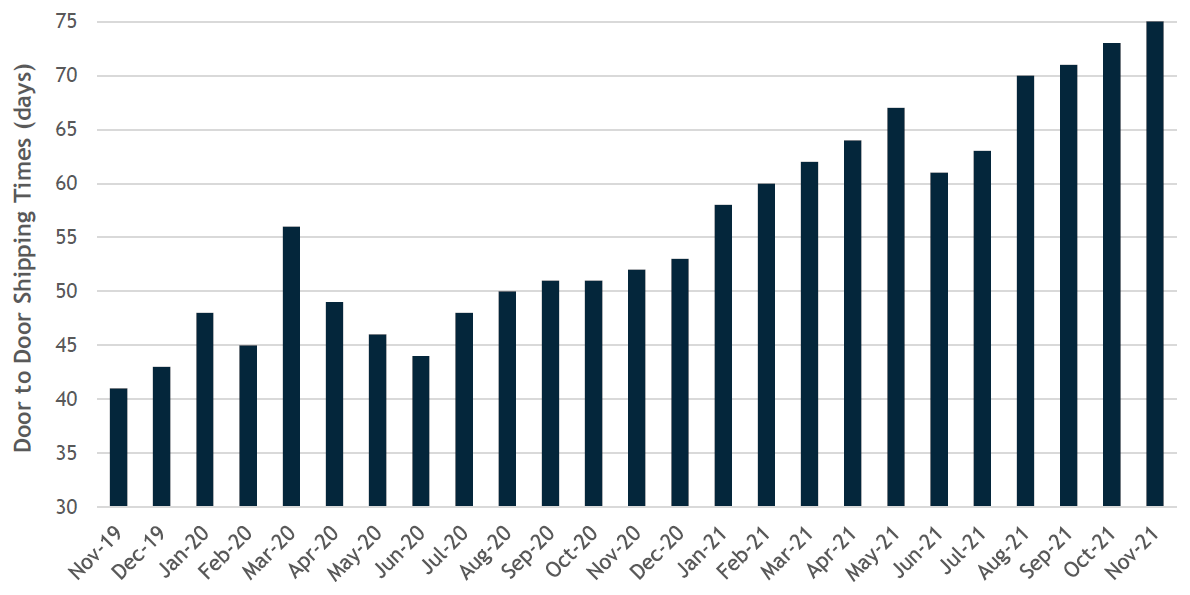

DOOR-TO-DOOR SHIPPING RATES BEST INDICATOR OF SUPPLY CHAIN PROBLEMS

Given everything that needs take place in order for goods to go door-to-door, we see this as one of the best indicators for high level supply chain backlog issues. While this measure is not product specific, it does point to the overall health of the supply chain from Asia.

As indicated in the chart below, door to door shipping times from East Asia to the West Coast U.S.A, is continuing to push higher. While we are starting to see/hear snippets of the supply chain congestion easing in some parts, it seems that is circumstantial as door to door shipping is taking 15% longer than 6 months ago and 47% longer than a year ago. Safe to say, the ability to compress shipping times back to mid 2020 levels will certainty take a herculean effort and will no doubt further contribute to the inflation narrative.

Door-to-Door Shipping Times (East Asia to West Coast U.S.A.)

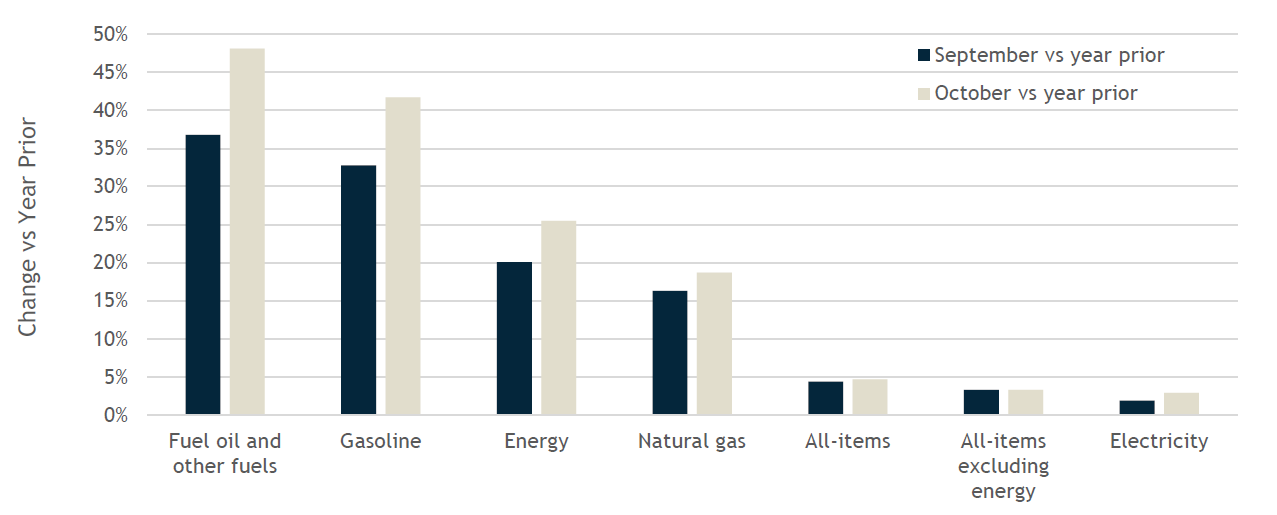

SUPPLY CHAIN AND INFLATION ARE TIED AT THE HIP

Inflation headlines never seem to reflect how we actually feel when we get the sticker shock of a price that has increased far more than the “ inflation index” suggests. The basket of goods contained in the CPI is wide ranging, as it should be, but, like most things the devil is in the details. Isolating individual components does a far better job highlighting what is really going on when it comes to the ins and outs of the inflation data.oks.

CPI Component Price Increases

DRIVING AND EATING CONTINUE TO GET A LOT MORE EXPENSIVE IN CANADA

Buried in the transportation section of the CPI data are energy costs that are up over 25% (on average) from 2020 levels. Mind you, we are comparing to a low data point but the fact that gasoline costs are up nearly 50% from 2020 sure stings, and is certainly going to hit the bottom line of transportation-heavy businesses.

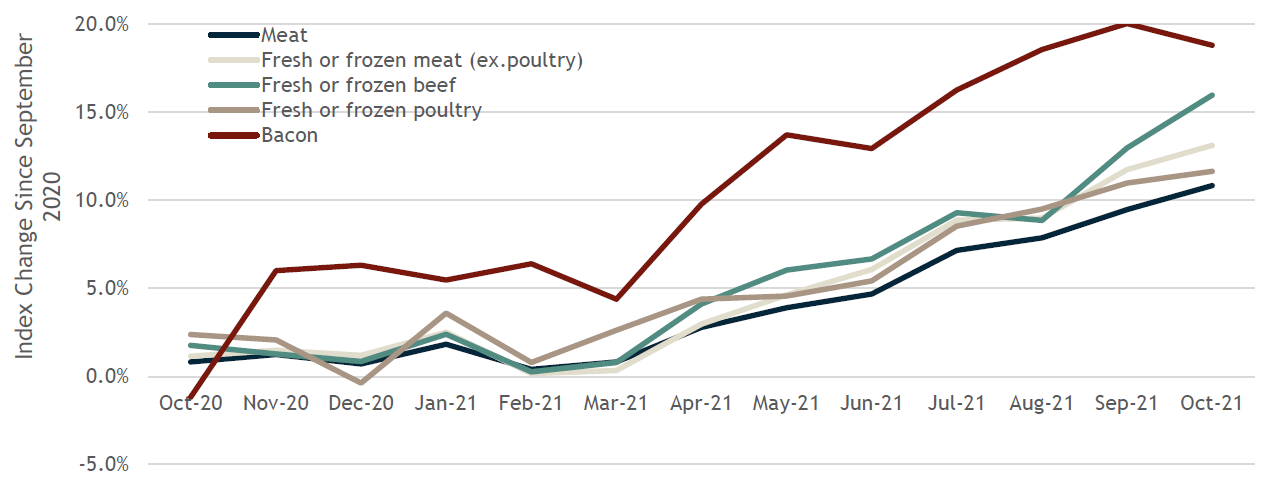

What about the food side of the equation?

- While the food basket, on average is up roughly 5% from year ago levels, there are offsetting components playing outside roles.

- Fresh vegetables are roughly flat to 2020 prices, but meat is up over 10%. Drilling further down, for the brunch lovers in the crowd, bacon has seen a 20% increase from last year.

CPI Index Change Since September 2020

Sources: Freightos Data, Paynet, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.