January 2021

IN THIS ISSUE:

- We have a look at how the events of 2020 increased the amount of sidelined private capital (dry powder) and suggest this will drive a material increase in 2021 transactions (both equity and debt)

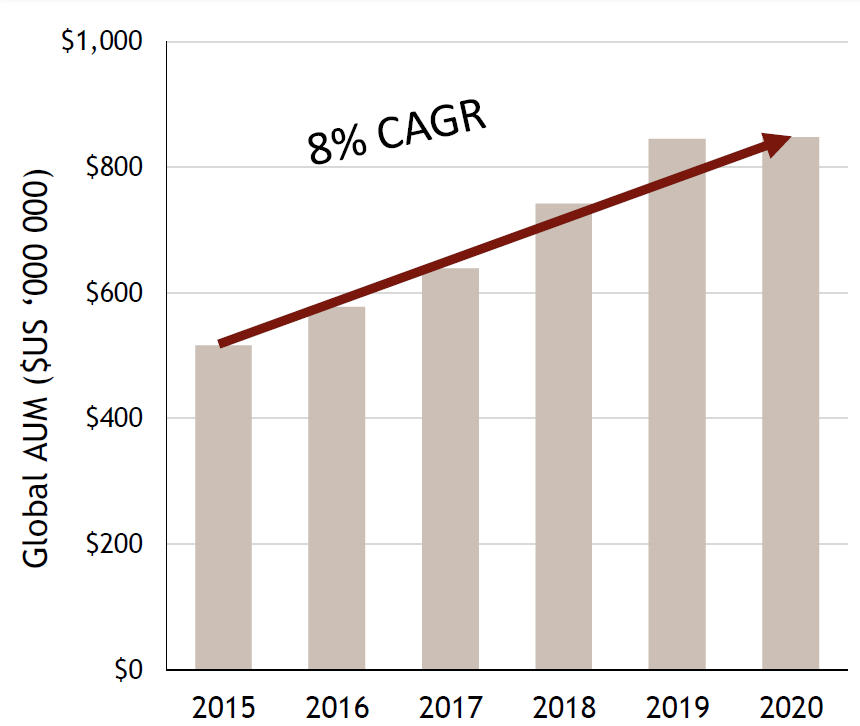

- Highlight the continued growth expected in the Assets Under Management (AUM) of both Private Equity and Private Debt), which have grown on a 11% and 8% CAGR respectively.

- Have a look at Canadian Private Equity activity, where the number of transactions on Canadian soil has trended down in recent years – but we expect that to change.

PRIVATE CAPITAL & DRY POWDER

A term coined back in the 1600’s when soldiers at war used to rely on gun powder to fire cannons, “dry powder” is now most commonly used in the capital world, referring to the amount of sidelined capital ready to be put to use. Dry powder, from a capital deployment standpoint, can be both a blessing and a curse.

Private capital providers (venture capital, private equity and private debt) need to carry a certain amount of capital that allows deal execution in order to deliver returns for their investors. Having a certain level of dry powder is a good thing as it increases deal certainty, enables faster execution, and minimizes financing risk. Dry powder becomes problematic when the amount of that sidelined capital grows to the point of negatively impacting fund performance as it sits there (known as cash drag), waiting to be deployed, not earning a return.

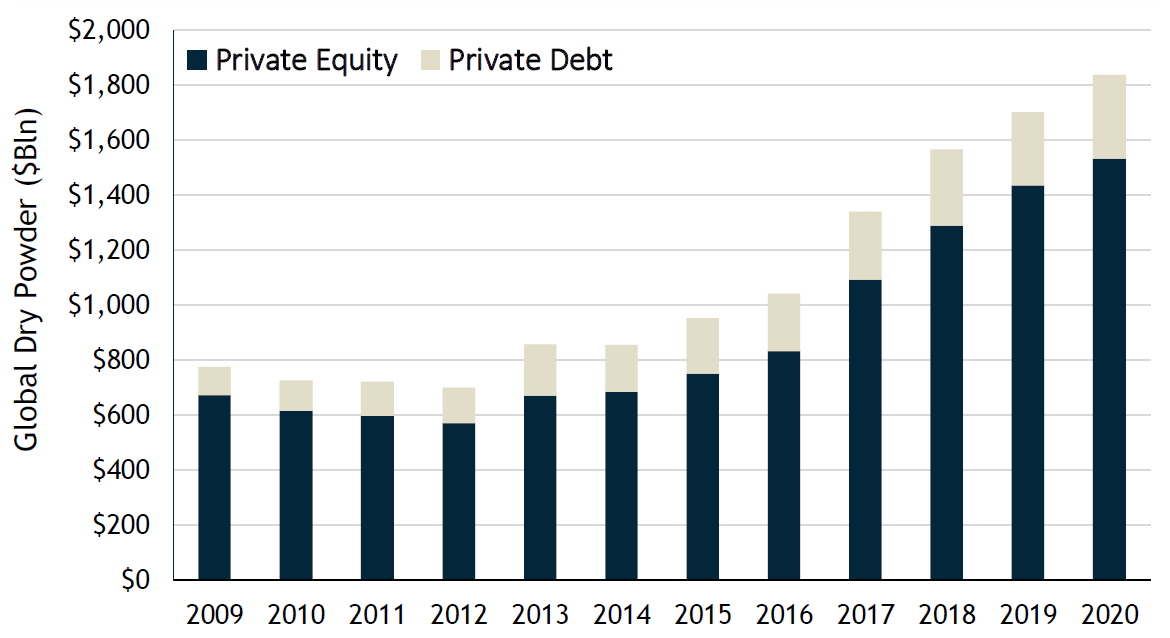

The amount of dry powder in the private capital space has always been relatively robust, but the combination of continued fundraising and fewer transactions, as a result of the pandemic, sets up what we expect to be a very robust 2021 in terms of number and size of transactions (both equity and debt).

Global Private Equity and Private Debt - Dry Powder

2021 IMPLICATIONS

While dry powder isn’t quite the equivalent of money burning a hole in your pocket, this setup suggests 2021 could see a significant uptick in deal flow as capital providers need to put money to work. It also likely means increased competition for higher quality transactions such as acquisitions and/or private loans.

2020 FUNDRAISING DOWN, DRY POWDER UP

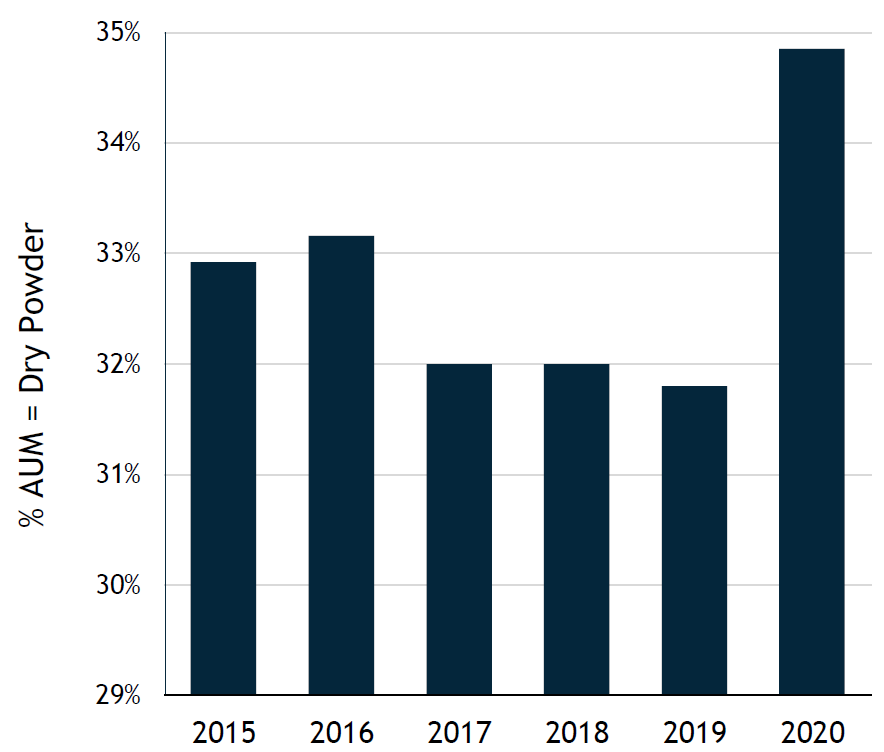

Despite the underlying appetite for the private equity and private debt asset classes, early indications suggest 2020 was a tough year for fundraising as private debt appears to have hit a 6-year low from a funds raised perspective. Typical fundraising efforts require extensive travel, meetings and entertaining (AKA shaking hands and kissing babies) and given the pandemic, traditional fundraising methods were put on ice. Despite this, it appears that dry powder has moved higher, particularly for private equity where dry powder as a percentage of Assets Under Management (AUM) currently sits in the 35% range, up nearly 5% from 2019 levels. In absolute dollar terms, despite flat AUM, dry powder is up a total of US$135 bln ($97 bln Private Equity, $38 Bln Private Debt).

This likely gives more urgency to those funds looking to deploy capital. From what we can tell, those funds who were successful in securing new capital, typically carried an establish track record that gave comfort to investors they could navigate the current environment.

% AUM sitting as Dry Powder (combined Private Equity & Private Debt)

PRIVATE EQUITY AND PRIVATE DEBT GROWTH EXPECTED TO CONTINUE

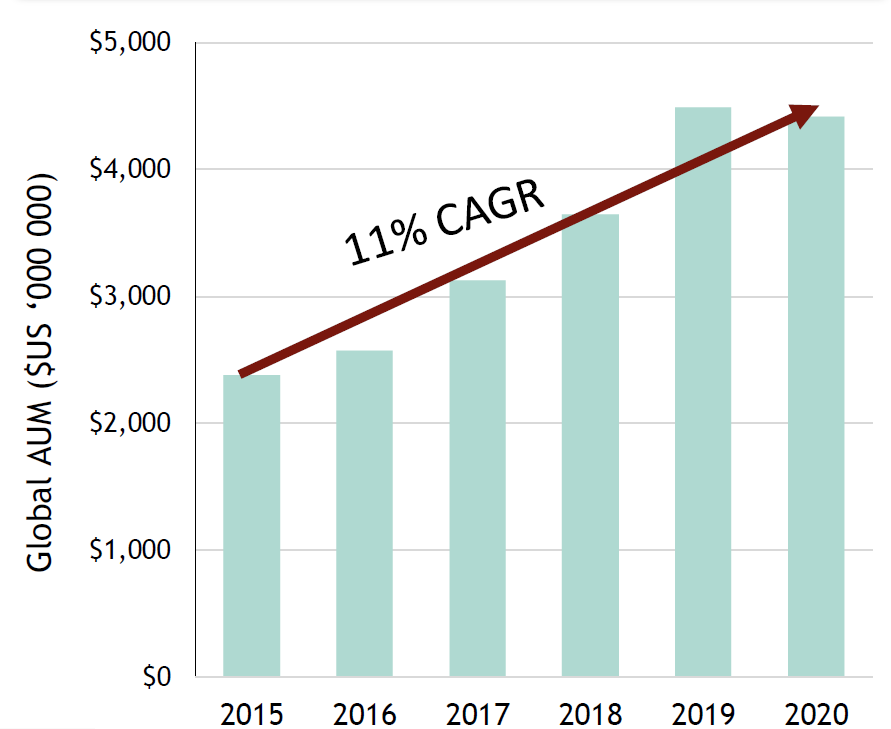

While the private equity and private debt sectors pale in comparison to their public counterparts in terms of AUM, their respective growth rates are nothing to scoff at. Longer term, this likely drives an increase in capital access for private companies (a good thing) and ultimately less need for those companies to become public entities. Industry experts expect the growth rates to continue with Private Debt expected to be a $1.5 Trillion asset class by 2025, representing 11.5% Compound Annual Growth Rate (CAGR), while Private Equity is expected to add another US$4.5 Trillion, representing a CAGR of over 15%.

Global Private Equity AUM

Global Private Debt AUM

A QUICK LOOK CLOSER TO HOME - CANADIAN PRIVATE EQUITY ACTIVITY

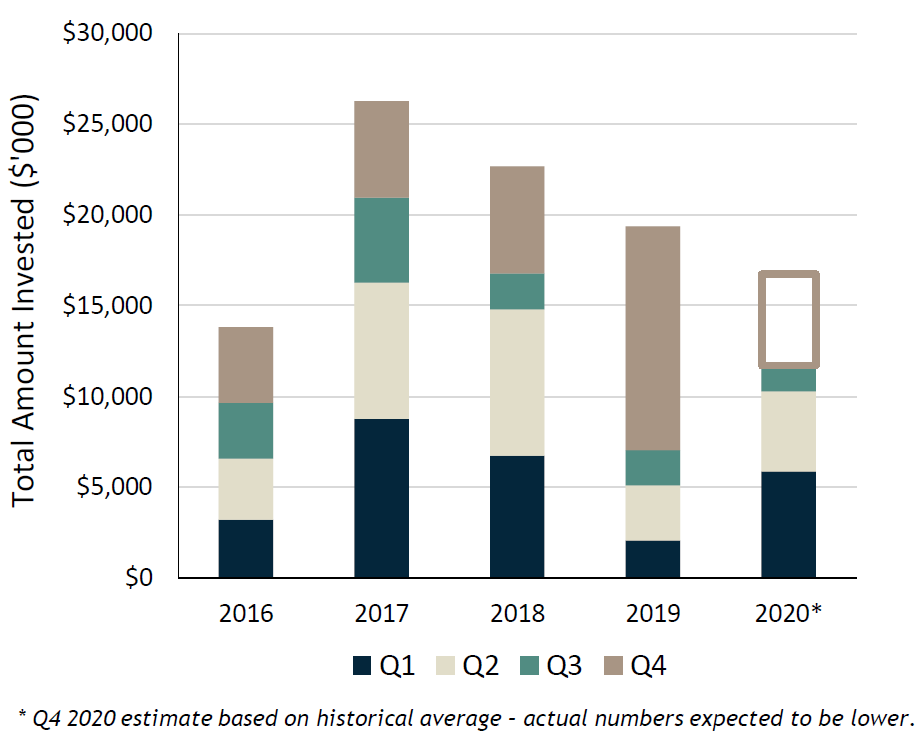

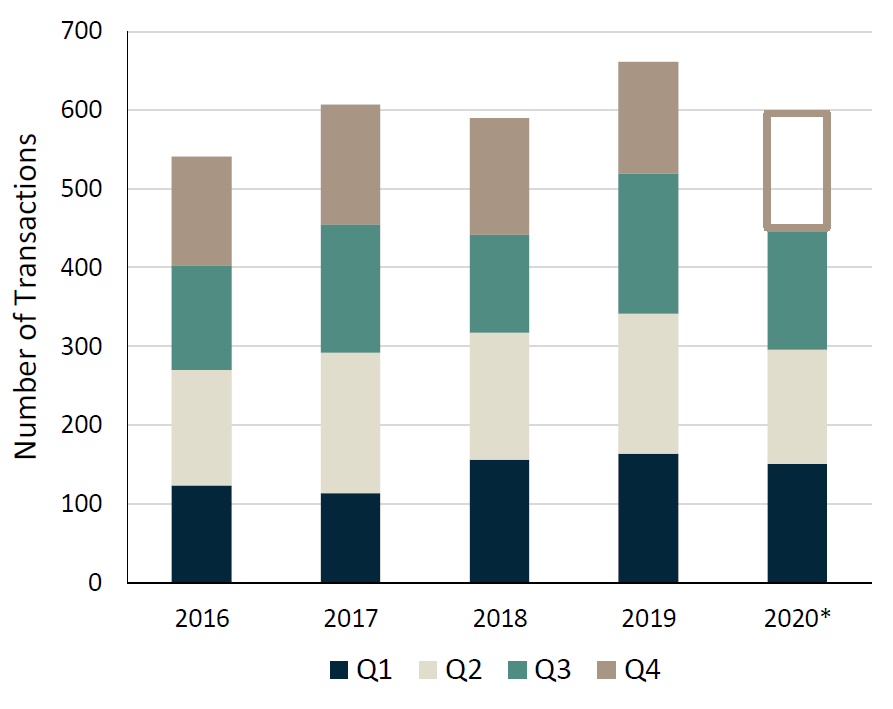

Unfortunately, acquiring Canadian specific data on private capital dry powder is hard to come by, but we can extrapolate based on Canadian Private Equity activity. Assuming Canada is following the global trend of roughly 10% annual growth in Private Equity AUM, and indications that annual deal activity (displayed through the total amount invested) has been on a downward trend, leads us to believe the stockpile of dry powder in Canada is rapidly expanding. This, combined with the increase in direct lending Private Debt fundraising activity we have witnessed in Canada, suggest we will see an increase in the number of private capital transactions on home soil.

Canada - Total Private Equity Investments ($)

Canada - Total Private Equity Transactions (#)

OUR KEY TAKEAWAYS

Dry powder in the private capital market is not a new topic of discussion by any means, but we do think the events of 2020 will force some of that excess capital off the sidelines and be put to work. Not only have we seen a jump in the relative amount of dry powder when compared to total AUM, dry powder, in its simplest form is kept to take advantage of opportunistic situations, which the pandemic has certainly created.

What we expect to see in 2021 as a result:

- Increase in Small/Medium enterprise acquisition activity – dry powder, combined with pent-up demand thanks to deals that were shelved due to the pandemic, sets the stage for an increase in private equity-driven transactions that will bring along complimentary debt solutions.

- “Good” deals get highly competitive – deals that screen well from a risk/return standpoint are going to be very competitive as capital providers are eager to get low-risk capital to work. Capital providers need to come to the table with real competitive advantages to win transactions. These include speed, flexibility and the ability to be creative.

- More non-Canadian capital put to work in Canada – Whether it be in the form of debt or equity, we suspect 2021 will bring more foreign capital into Canada as capital providers look to bring their respective competitive advantages and compete for deals here.

All of this goes to say that we anticipate an increase in the amount of private capital to be put to work. Despite the long road remaining to get through the other side of this pandemic, the consensus is that we are through the period of highest uncertainty. That view alone, along with the market dynamics reinforce our belief that 2021 will be a significant year for the private capital space.

Sources: Prequin, Diamond Willow Advisory, CVCA Intelligence.

The Debt Digest lands in your inbox each month.