June 2021

DIGGING THROUGH THE BANKS LOAN BOOKS

Loan Losses Down, Commercial Credit Flat, Mortgages Continue to Ramp

Another round of quarterly financial results from Canada’s major banks just wrapped up and the Q2/2021 results reiterated that Canada’s main lending institutions continue to get more comfortable with their credit books. We rolled up our sleeves once again and the data supports the conclusion that we are officially through the worst of what was a short lived tight credit market. Here are some of our key takeaways, which are analysed in more detail on the following pages:

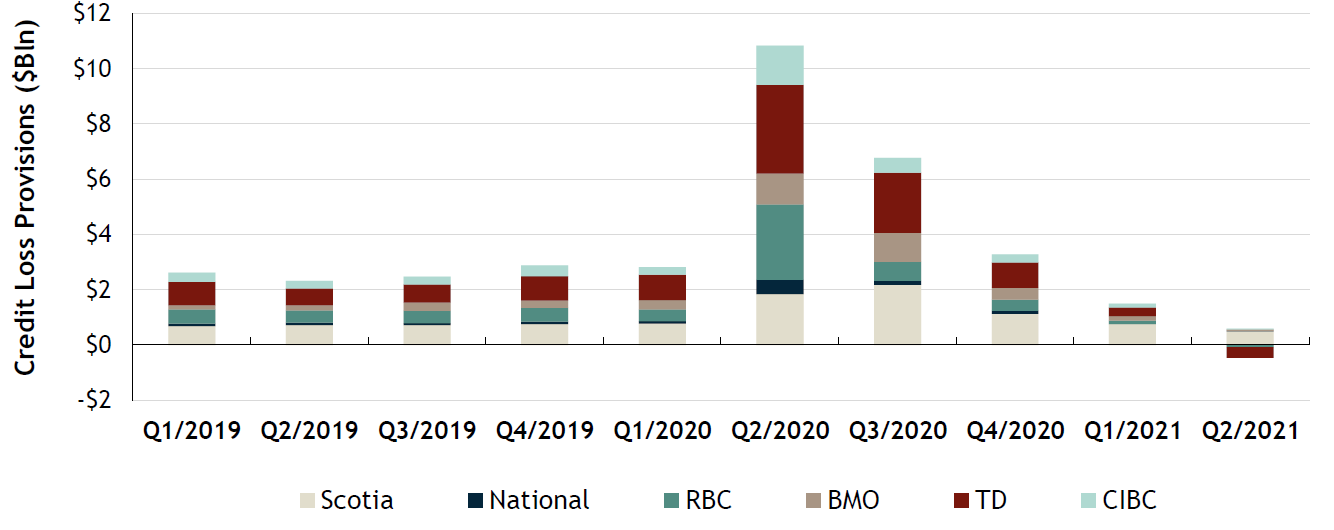

- Loan Loss Provisions Once Again Fall – This one even confused us. At the beginning of the pandemic the banks built up huge allowances for credit losses to offset the anticipated losses from the pandemic. This quarter, one third of the Big 6 saw loan loss provisions go negative.

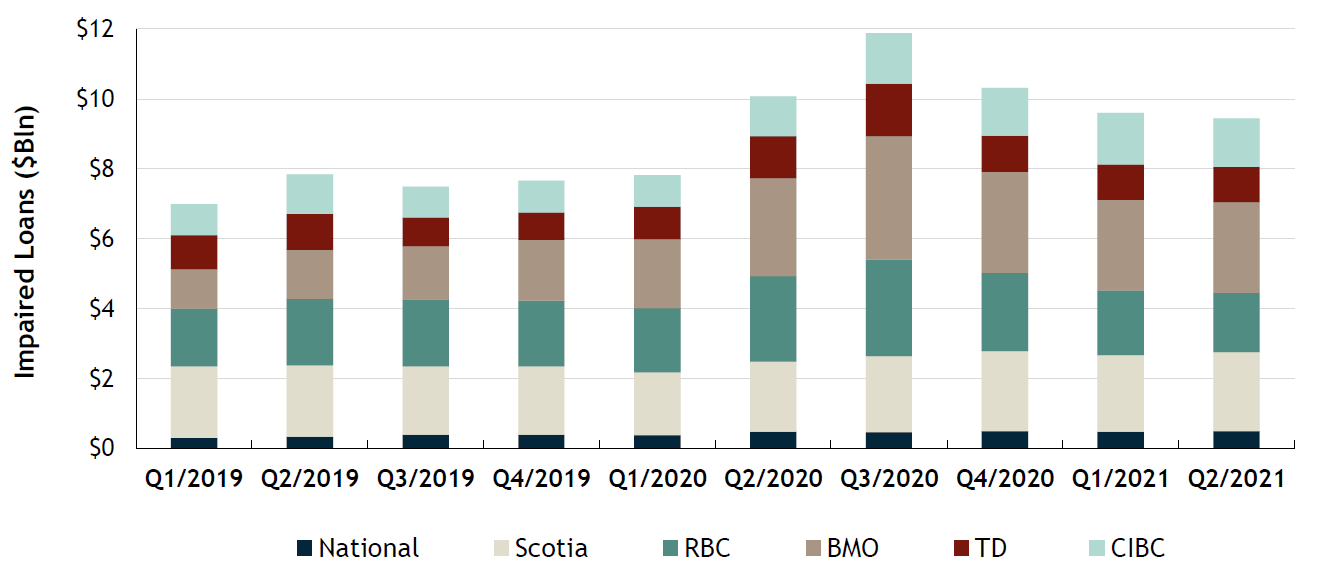

- Gross Impaired Loans Continue Downward Trajectory – Further reinforcing comfort levels of Canada’s lending institutions, total gross impaired loans dropped another 2% this quarter, which followed a 7% drop in the previous quarter.

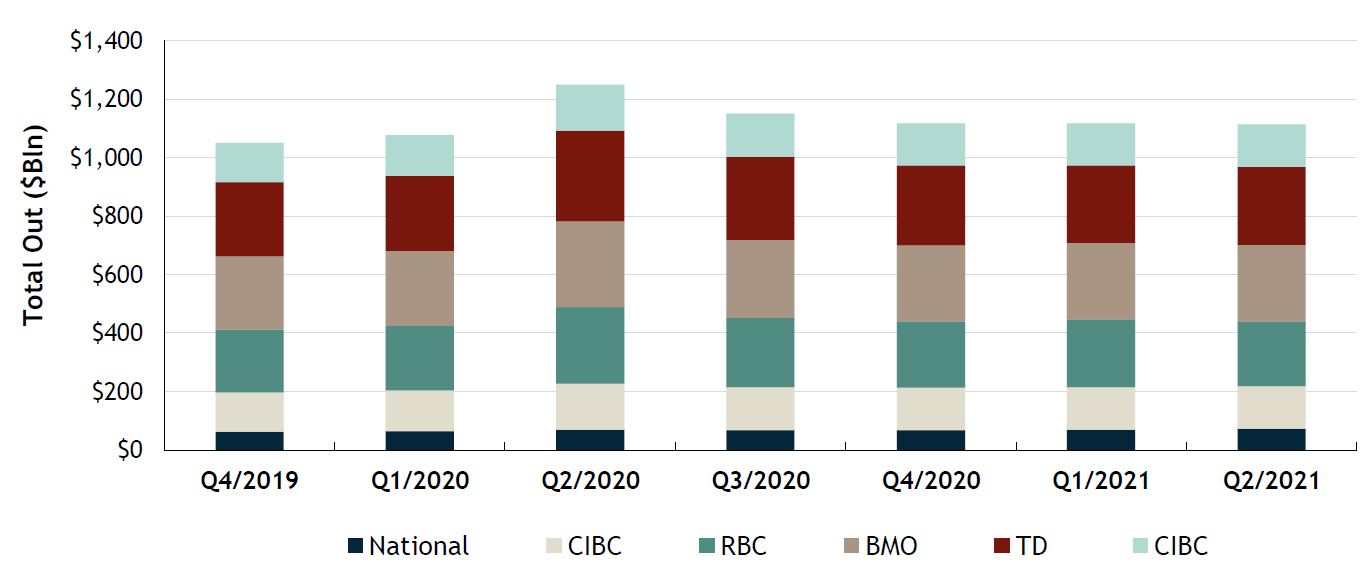

- Total Commercial Credit Out Is Flat – Surprisingly, even though loss provisions and impaired loans are decreasing commercial credit remained flat.

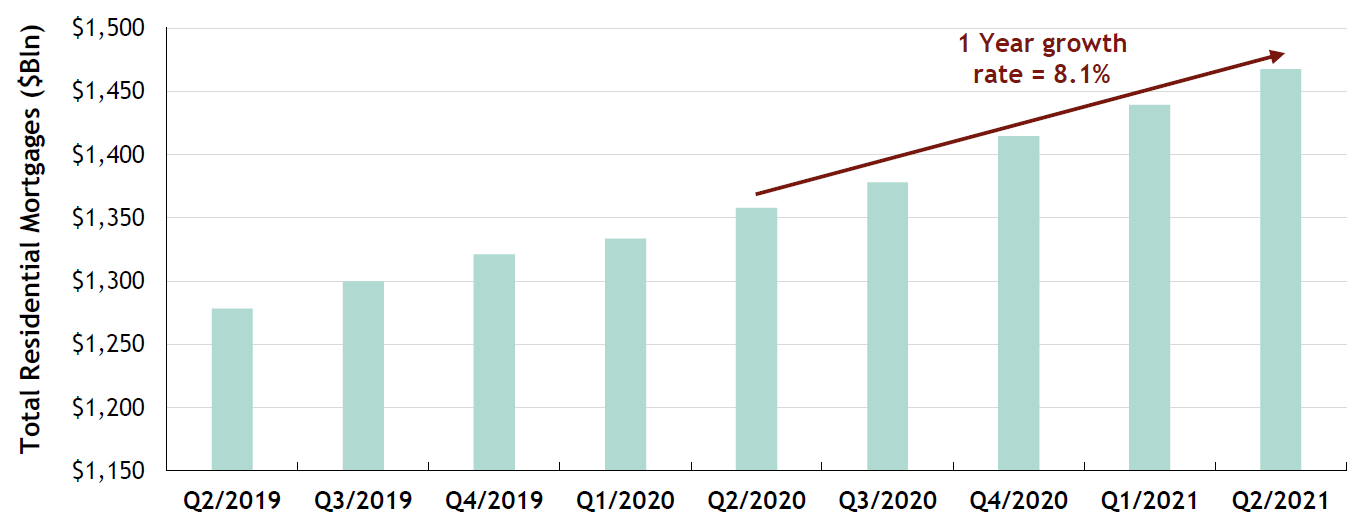

- The Banks Continue to Fund Residential Mortgages – As we all hear about flaming hot housing market across the country we wanted to look at how big a part the banks were playing. Mortgage credit is up 8% over the past year.

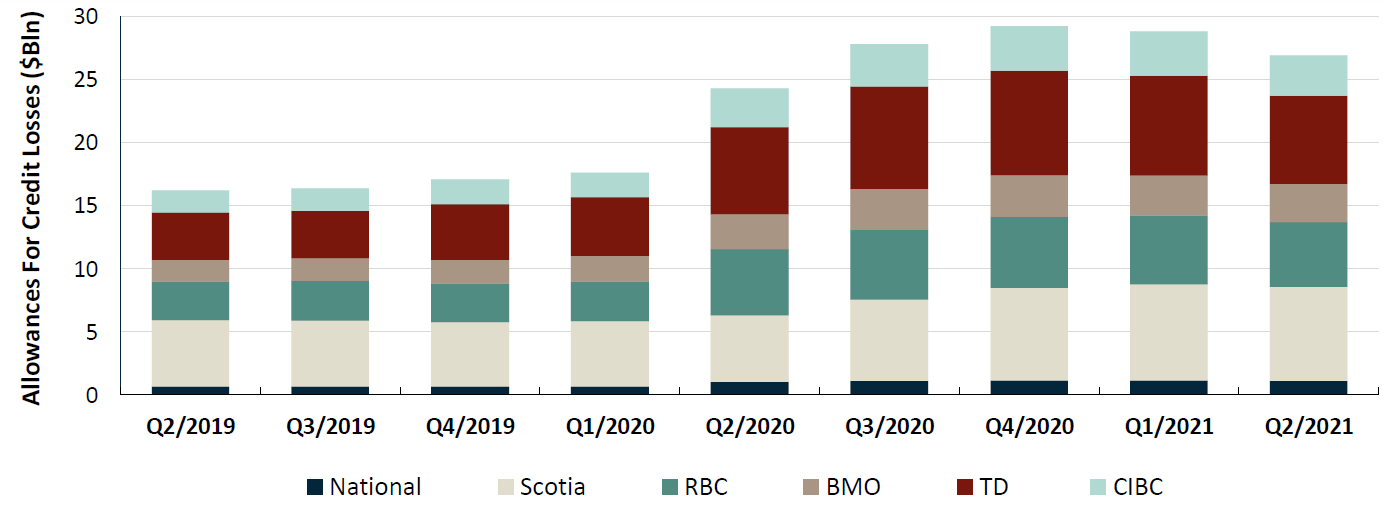

Allowances For Credit Losses From Canada’s Largest Banks

MAYBE A LITTLE BIT OF NEGATIVITY IS A GOOD THING - LOAN LOSS PROVISIONS FALL ONCE AGAIN

We have often said that loan loss provisions provide the strongest indication of the comfort level from Canada’s top lenders. Continuing the reduction trend we first saw in Q3/2020, loan loss provisions saw another decline this quarter. TD and RBC Loan Loss Provisions were negative and every bank’s stage one and two Provisions were negative. As mentioned at the beginning of the pandemic the banks built up huge Allowances for Credit Losses to offset the anticipated losses from the pandemic. The actualized credit losses were far smaller then anticipated so the banks are using negative provisions to unwind the previously anticipated losses.

Loan Loss Provisions Go Negative

MIGHT BE GROSS BUT IT SHURE IS PRETTY TO LOOK AT - GROSS IMPAIRED LOANS CONTINUE DOWNWARD TRAJECTORY

The combined Gross Impaired Loans (GIL) amongst Canada’s largest banks fell 2%, again reaffirming the confidence in current credit facilities. It should be noticed that it looks like the rate of decline is slowing down from the 7% decrease in Q1. However that shouldn’t be a surprise as the current impaired loans are already down ~20% from pandemic highs.

Another Reduction in Impaired Loans Across Canada’s Banking Sector

WHY WON’T YOU GROW - TOTAL COMMERCIAL AMOUNT IS OUT FLAT

After seeing both a decrease in Loan Loss Provisions and Gross Impaired Loans we expected an expansion in total commercial credit out however quarter over quarter it remained flat. From there we decided to take a look back to 2008 to try and get a better idea about the future might look like. After the crash of 2008 it took about 5 quarters of low Loan Loss Provisions before the banks started increasing their loan books.

Total Commercial Amoutn Out Flat To Q1/2021

HOME SWEET HOME - THE BANKS CONTINUE TO FUND RESIDENTIAL MORTGAGES

As house prices across country spike and incomes remain stagnant, the banks are continuing to pick up the slack. This might be the last quarter of expansion however. Regulatory agencies across Canada are fearful that if rates rise Canadians won’t be able to debt service. Because of this, individuals now have to prove they can debt service at an interest rate of at least 5.25%, previously they had to prove they could service at 4.79%.

Another Increase In Total Residential Mortgages (Canada’s Big 6 Banks)

Sources: Company Reports, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.