June 2023

INSOLVENCY FILINGS ARE UP AND ACCELERATING. WHAT’S NEXT…

After a material decline during the pandemic, it appears the ‘insolvency monster’ has set its sights on Canadian consumers and businesses alike. Continued financial headwinds, such as persistent inflation and increasing debt service costs are the main driving factors behind this trend, but we are also seeing the impacts of the winding down of government aid.

Consumers continue to show resilience as insolvency figures remain below their pre-pandemic levels (-5% below), but insolvencies are accelerating (+26% YoY). Business insolvencies (bankruptcies and proposals) aren’t quite as resilient (+6% vs. pre-COVID levels) and are also demonstrating an accelerating trend (+33% YoY). Read on to find out more.

KEY TAKEAWAYS THIS MONTH:

- Canadian consumers continue to be resilient, but there are early warning signs that insolvencies are likely on the rise. Credit product use, namely credit cards (+14% YoY), is on the rise to combat the increased cost of living.

- Business insolvencies are rising at an even faster rate than consumer insolvencies. Bankruptcies rose across almost all sectors but were more hard-felt in industries hit hardest by pandemic restrictions.

- Looking forward, financial headwinds, namely persistent inflation and a higher interest rate environment, will intensify and likely accelerate insolvencies.

THE BACKUP DATA

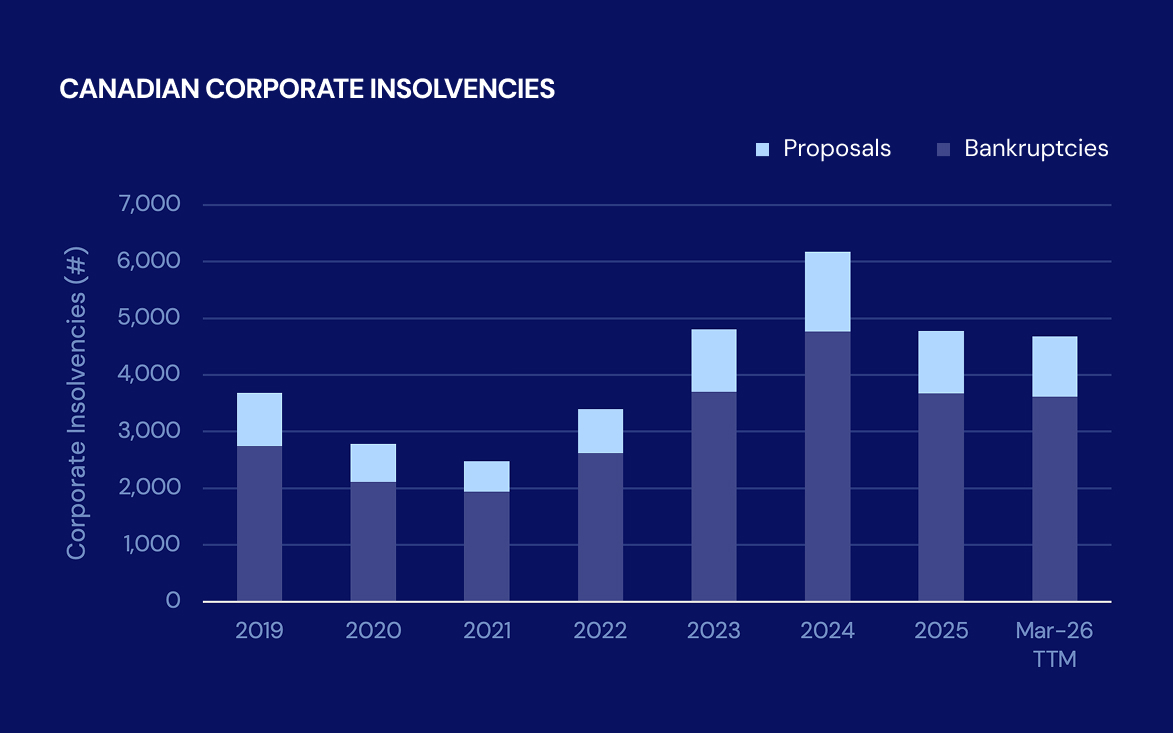

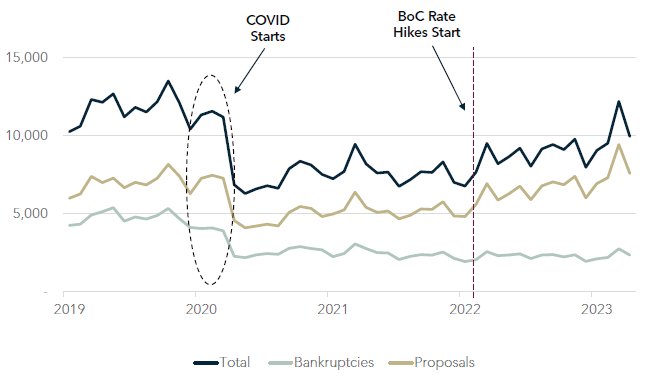

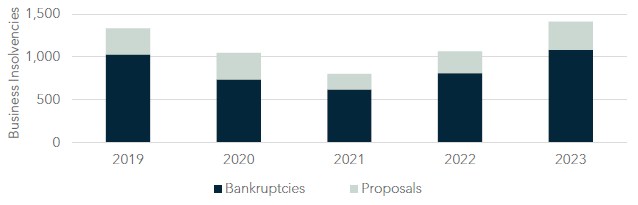

Overall Bankruptcies Remain Low But Primed To Grow: When viewed in aggregate (consumers plus businesses), bankruptcies continue to be well below their pre-COVID levels but have grown +6% YoY. Perhaps more interesting, insolvency proposals are up +35% YoY, signalling that a wave of potential bankruptcies is on the horizon.

Canadian Insolvencies, Annually (2019 - 2023 YTD)

CONSUMER INSOLVENCY INSIGHTS

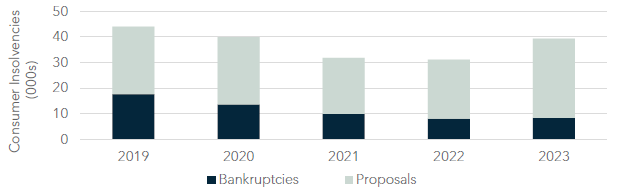

Consumer Insolvencies, Jan - Apr 2019 - 2023

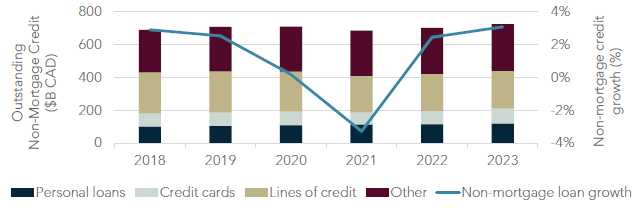

Non-Mortgage Consumer Credit, 2018 - 2023 YTD

CONSUMERS REMAIN RESILIENT… FOR NOW.

Consumer insolvencies are 11% below pre-COVID levels, largely driven by a lack of bankruptcies. This is a testament to the resilience of Canadian consumers throughout COVID and since. However, persistent inflation paired with aggressive rate hikes from the Bank of Canada have begun to take their toll – insolvency proposals, which are a key measure of potential bankruptcy, increased +35% YoY during the January-through-April period and are +17% above pre-pandemic levels. A large contributing factor to this trend is the increased cost of living in Canada and consumers have become more reliant on credit products to make ends meet. Credit card balances have increased +14% YoY (compared to overall consumer credit growth of +3.0% YoY), and monthly payments have increased +9% YoY. Mortgage (+17% YoY) and line of credit payments (+35% YoY) have also increased. Delinquency rates have increased 11%, which may be a potential early warning sign of deteriorating consumer credit. When taken all together, it is evident that Canadian consumers are facing greater financial pressures – this is a trend we will continue to monitor.

BUSINESS INSOLVENCY INSIGHTS

Business Insolvencies, Jan - Apr 2019 - 2023

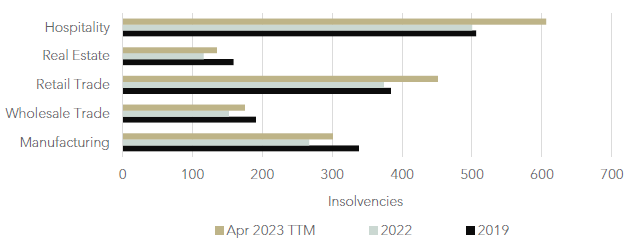

Industry Insolvencies, 2019 vs. Apr 2023 TTM

SOME BUSINESSES SHINE, SOME ARE CLOSING UP SHOP.

Bankruptcies continue to increase at a growing rate, reaching +33% YoY for the January-through-April period (compared with +31% YoY during the same period in 2022). Certain industries, namely service-based industries, were particularly hard-hit by the most recent round of bankruptcies – in particular, the Hospitality Industry continues to have elevated insolvencies (+21% YoY and +20% vs. 2019 levels). Retail Trade was also a victim – insolvencies have grown +21% YoY and +17% versus 2019 levels. Although Canadian business bankruptcies appear to be on the rise, it’s not all doom and gloom – in aggregate, Canadian businesses grew their total operating revenue by +11% YoY (compared with 3-6% pre-COVID). They also remain very conservatively leveraged with an average debt-to-total assets ratio of 44% (compared with 51% pre-COVID).

Sources: Statistics Canada, Bank of Canada, CREA, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.