May 2020

IN THIS ISSUE:

- We revisit impaired loan growth within Canada’s main financial institutions with impaired loans hitting a new peak in Q2/20.

- With credit loss provisions rising nearly 4-fold this quarter, impaired loan growth is set to follow down the road.

- Despite the current pandemic, Q2/20 saw Canadian financial institutions grow their business loan books over 16%, over 4-times the historical growth rate.

CANADIAN BANKS BATTEN DOWN THE HATCHES AFTER A QUARTER OF SIGNIFICANT CREDIT EXTENSION

Today’s edition of DWA debt digest offers a little bit of a Throwback Thursday as we revisit a topic we dug into late last year. For those lucky enough to remember our impaired loans trends analysis, you are in for a treat as we are coming around to dig in again. We are broadening the analysis this go around as we flush out data that provides a glimpse of lending practices from Canada’s main lending institutions.

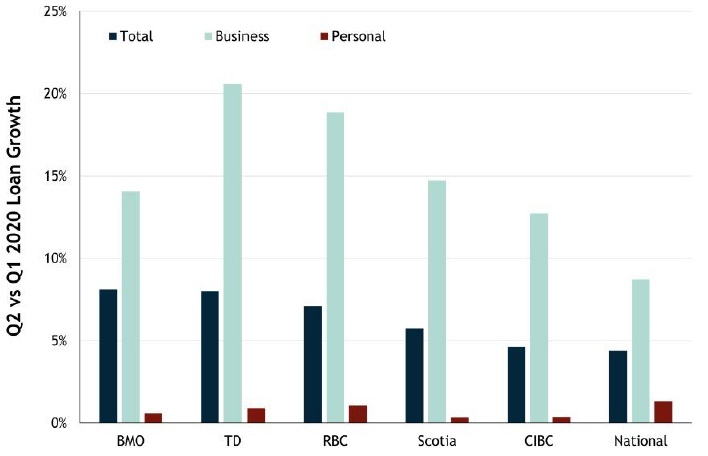

This was another “roll up our sleeves” exercise with some of the results causing a few eyebrow raises, sprinkled amongst instances of “ah, that makes sense.” Noteworthy items include the fact that in Q2 (Feb – April), Canadian banks added new business loans at a growth rate of 16% over the previous quarter, four times larger than the historical run quarter over quarter growth rate, shocking given half the quarter saw the world essentially in shut down mode.

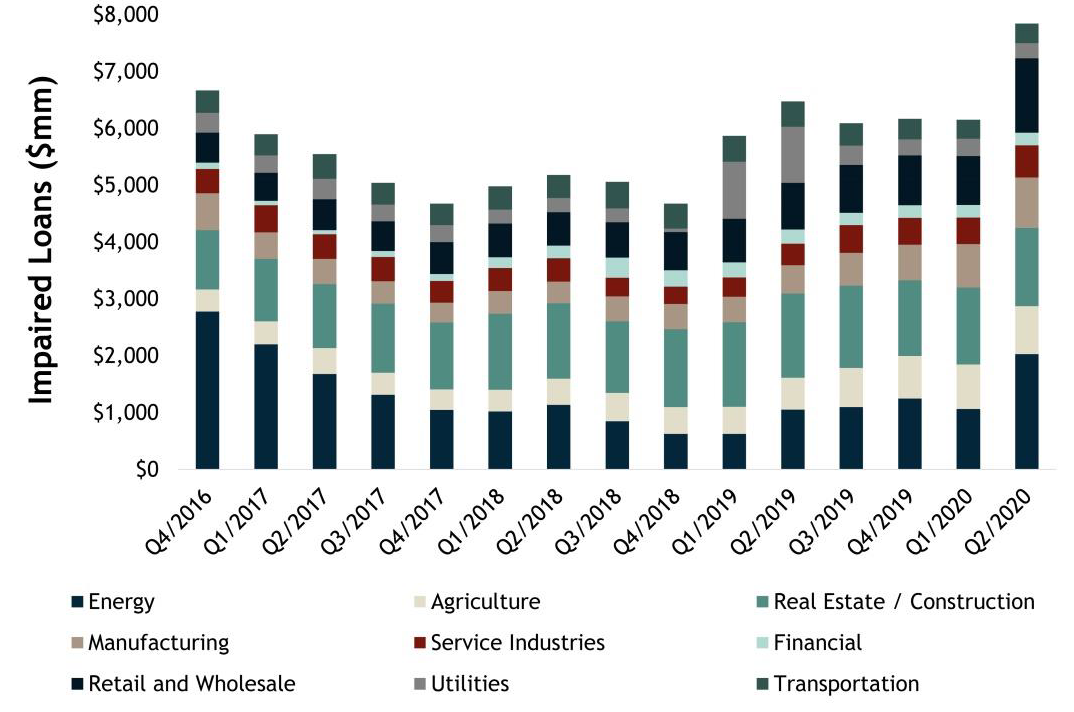

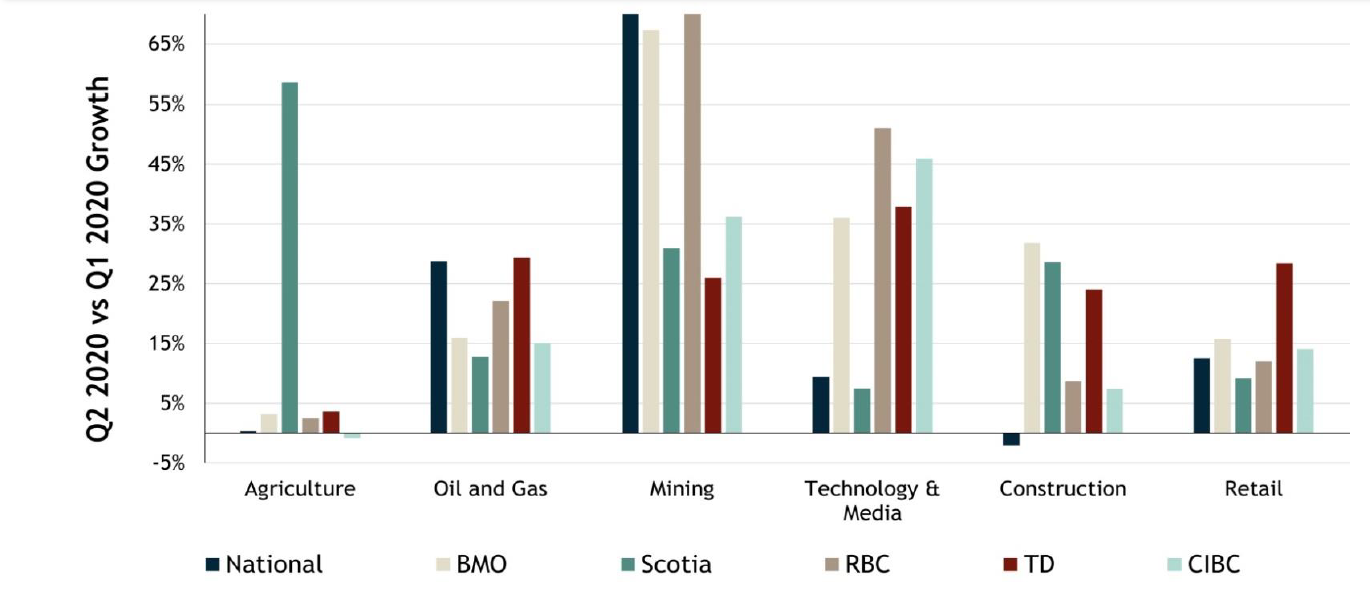

On the impaired loans side of the ledger no real surprise that the energy and retail sectors saw the largest increase in impaired loans with manufacturing close behind. Canadian banks seem to be preparing for rainy days ahead as credit loss provisions were bumped four fold to $10.5 billion (up nearly $8 billion).

Canadian Banking - Impaired Loans by Major Sector

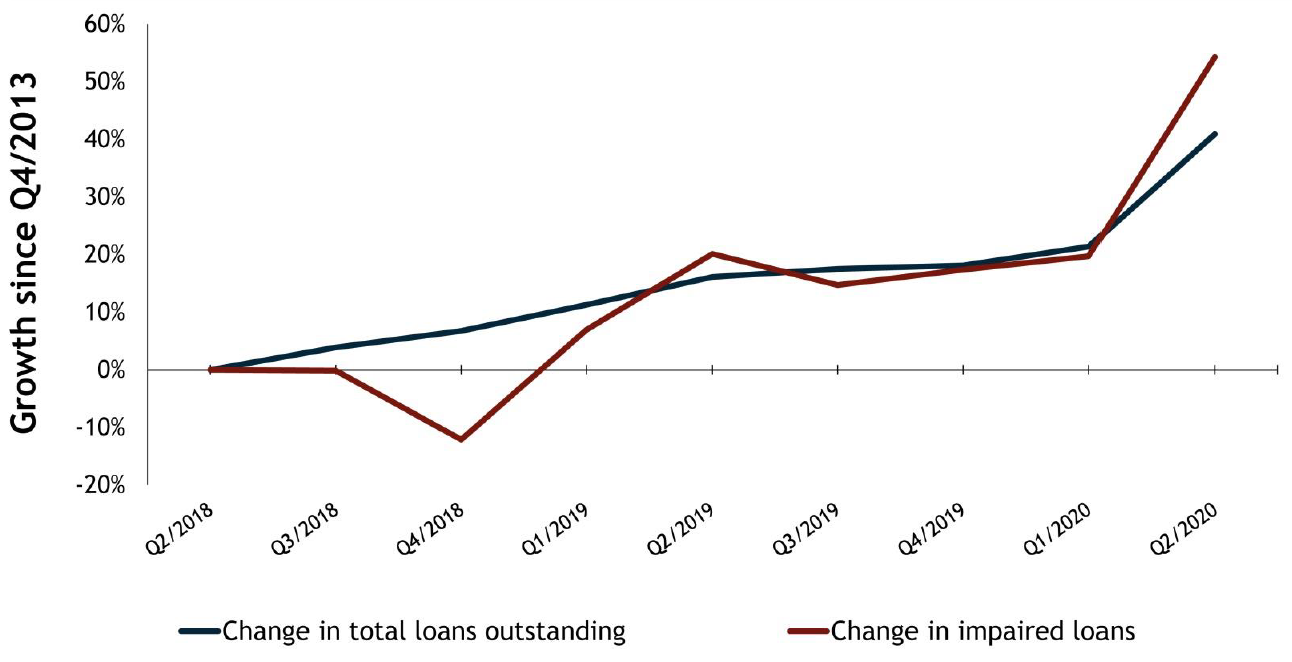

Total Accepted Loans and Impaired Growth since Q2/18

Are the days of easy credit over?

- The growth rate in non performing (impaired) loans over the past 2 years reached 50%, with Q2 data showing the growth rate has eclipsed that of new loans in a meaningful way. With banks setting aside a material amount of money for future impaired loans (via loss provisions) we expect loans deemed impaired to move meaningfully higher in the coming quarters.

- Thankfully, the Canadian financial institutions entered this current economic crisis in prime fighting shape as loans deemed impaired make up less than 1% of total loans outstanding. Having said that, conversations suggest access to Schedule A Bank credit is getting increasingly difficult, ultimately clearing the path for incremental deal flow to the alternative lenders.

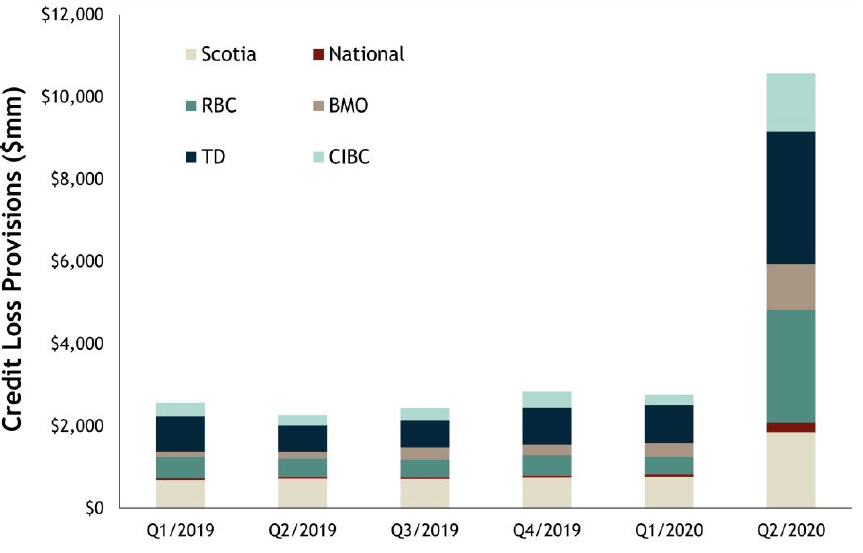

Canadian Banks - Provisions for Credit Losses

Credit Loss Provisions go Hyperbolic

- Providing an indication of how nervous financial institutions are of their loan books, combined credit loss provisions reached $10.5 billion this quarter, nearly 4 times the run rate over the last 5 quarters.

- Energy and retail were reoccurring themes where banks are preparing for an increase in non-performing loans. Institutions also increased provisions in health care and manufacturing.

- Provisions for credit loss of currently performing personal loans made up nearly half the Q2/2020 increase.

A GLIMPSE BEHIND THE CURTAIN

Given the depth of disclosure, quarterly results offer up a chance to dig deeper into the lending trends amongst Canadian banks. Who is being more aggressive, more conservative, and lending to what sectors are top of mind questions for alternative lenders and competitor banks alike. A massive surprise this quarter offered up was the material growth in business loans, with exposure increasing 16%, over four times the historical run rate, this despite COVID-19 having related shutdowns for half the quarter.

Who Grew their Loan Book the Most?

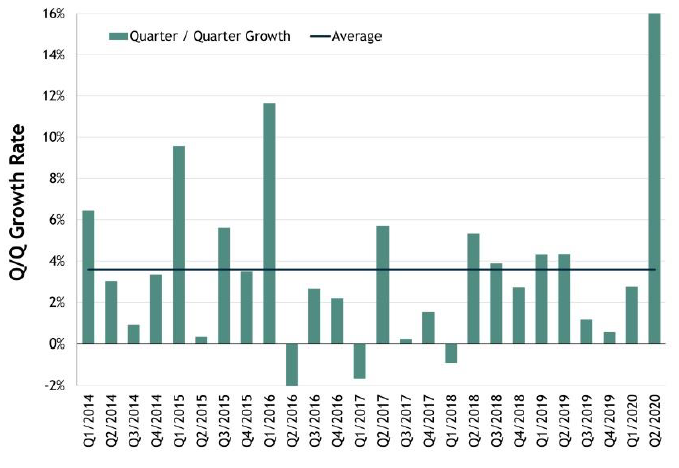

Combined Business Loan Growth

Change in Sector Exposure Amongst Canada’s Banks

HAS THE MUSIC STOPPED?

Even prior to the current pandemic, which has crippled the economy, the growth in impaired loans was already a red flag. Thankfully, Canada’s financial institutions were in great shape so lending practices were clearly not impacted, but we see this changing dramatically. With over $10 billion set aside for future credit losses, it’s not a stretch to think accessing bank credit is going to be increasingly difficult, which once again leads us to believe the debt financing gap will be filled by alternative lenders. To help fill the gap Diamond Willow has been diligently expanding our alternative lending network (now in excess of 200) positioning us to help provide solutions to nearly every financing need.

Sources: Company reports, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.