May 2021

IN THIS ISSUE:

- We emphasize the connection of commodity prices and the Canadian dollar. Since 2018, the correlation between the performance in the Canadian dollar and Bank of Canada commodity index was 0.78.

- Highlight Canada’s key importing and exporting industries with the United States in an effort to show which business may have a headwind or tailwind.

- Lastly, we highlight reasons why a strong Canadian dollar is here to stay as commodity outlook and Central Bank communications continue to favour Canadian dollar relative strength.

HOW TO THINK ABOUT THE RUN IN THE CANADIAN DOLLAR

The lofty loonie seems to be making its way back into the headlines of late with the recent push seeing the Canadian dollar hit $0.83 USD, the highest level in over 6 years. What is missed in the headlines is the steady march of the Canadian dollar relative to the USD; the CAD dollar has run 18% since the depths of the pandemic and 15% over the past year. This has real implications for businesses as it either creates a tailwind or headwind depending on what side of the coin you land on (see what we did there).

Before we get into it, fair warning – we are not foreign exchange experts by any means. The FX market is one of the most complex and efficient markets in the world, making it equally terrifying and interesting as it arguably serves as the best leading indicator for things such as Central Bank interest rate hikes.

Our aim for this debt digest is to highlight main drivers of the Canadian currency exchange rate, flush out those sectors that stand to benefit the most, those that struggle with relative dollar strength and pontificate (yeah, we went there) some of the factors at play that may lead to the Bank of Canada moving on rates before our neighbors to the south.

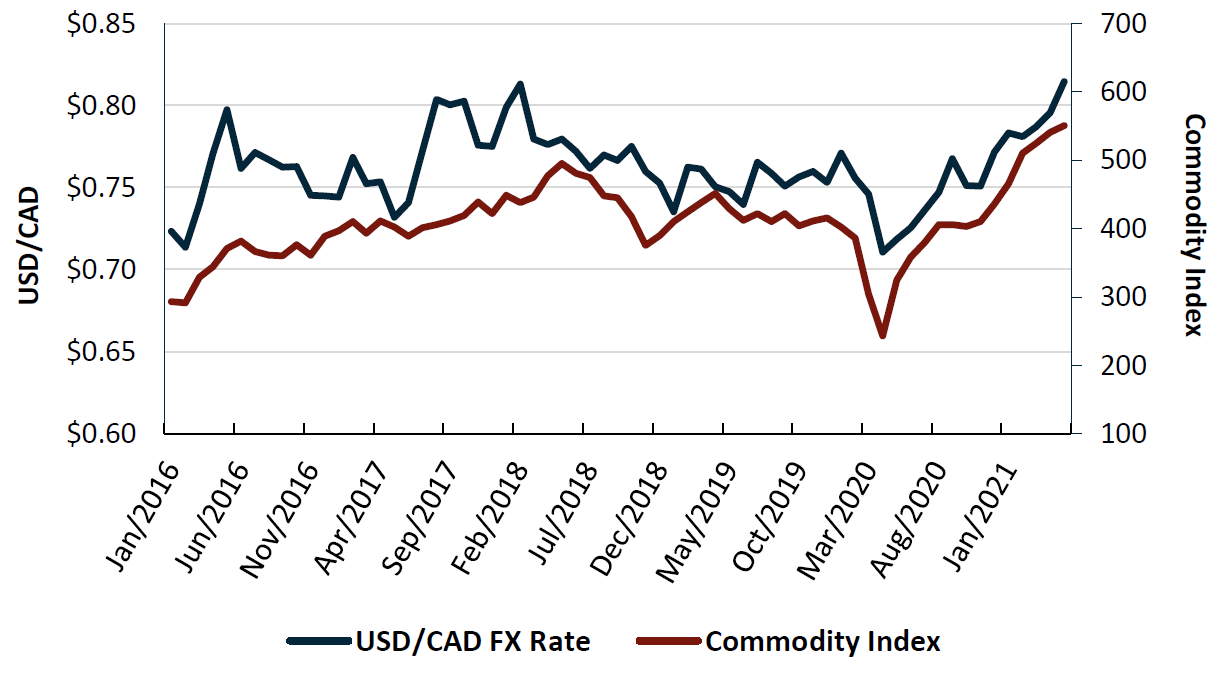

We set the stage by reminding readers the Canadian dollar is still very much driven by relative moves in commodity prices. As shown below, the FX and Bank of Canada commodity price index is HIGHLY correlated (0.63 since 2016 and 0.78 since 2018). If commodity moves explain ~75% of rate moves what drives the rest?

Bank of Canada Commodity Index and USD/CAD Exchange Rate

MAIN DRIVERS OF CANADA’S COMMODITY INDEX AND THEREFORE THE CANADIAN DOLLAR

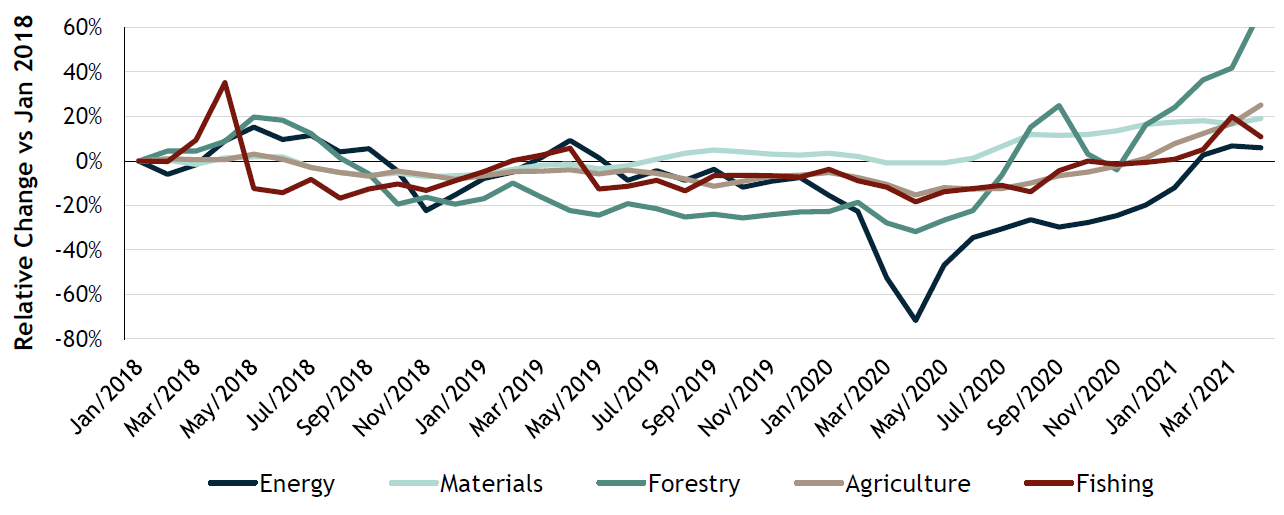

Commodity Index Components – The Bank of Canada’s commodity index can be broken out into five components: Energy, Materials, Forestry, Agriculture and Fishing. What can be seen from the chart below is that all five components have shown relative strength since the depths of the pandemic with Energy and Forestry leading the way. This is no surprise but given the respective positive outlook in each of the sectors highlighted, we suspect continued strength in the relative index performance.

Given movements in these commodity-based industries drives 60-70% of the Canadian dollar performance, we are not taking a leap of faith by saying the dollar will continue to outperform.

Segments of Canada’s Commodity Index - Relative Performance vs Jan 2018

WHO IS THE STRONGER CANADIAN DOLLAR HURTING? WHO IS IT HELPING?

Industries With a Headwind

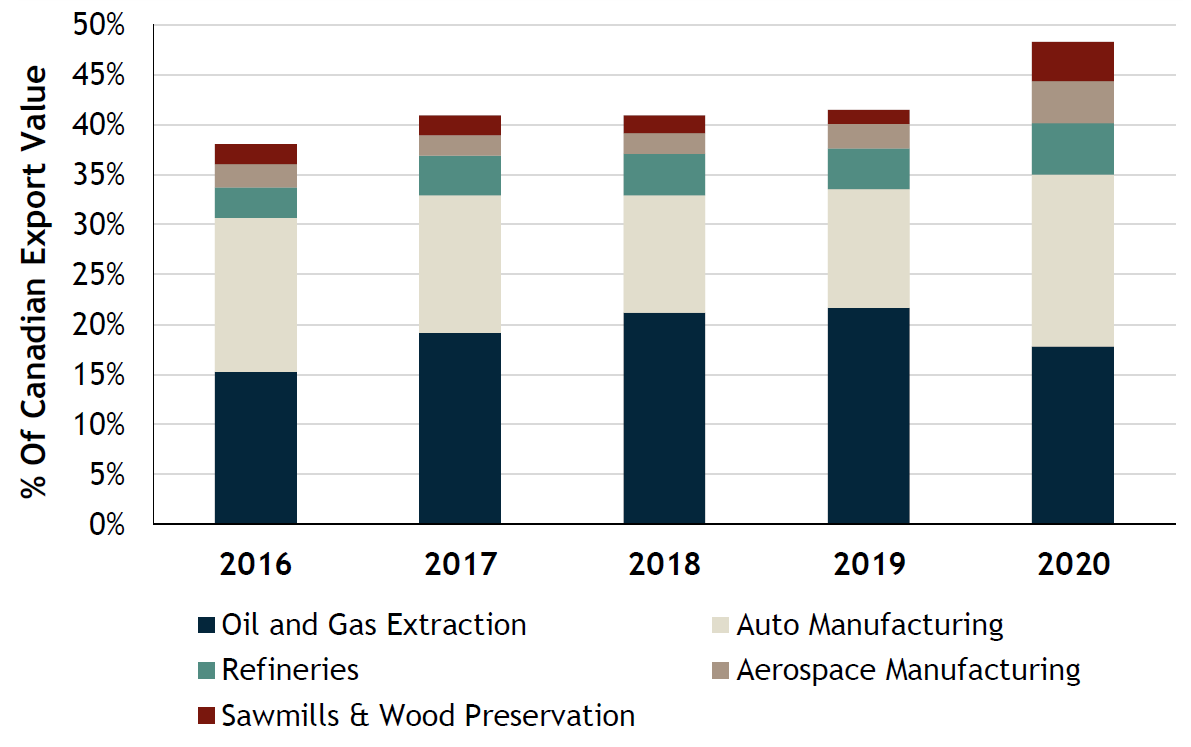

When looking at Canada’s top 5 exporting industries, energy and manufacturing are most exposed to the negative impacts of a stronger Canadian dollar.

The irony around oil and gas (i.e. energy) being most exposed to a stronger Canadian dollar, is that as shown in the previous charts, the Canadian dollar is stronger thanks to higher energy prices. In this sense it is a bit of a natural hedge. In 2020, the top 5 exporting industries made up nearly 50% of Canada’s total export value, a significant jump from 2019 despite a lower contribution from the oil and gas extraction sector.

Headwinds: Canada’s Top 5 EXPORTING Industries to the United States

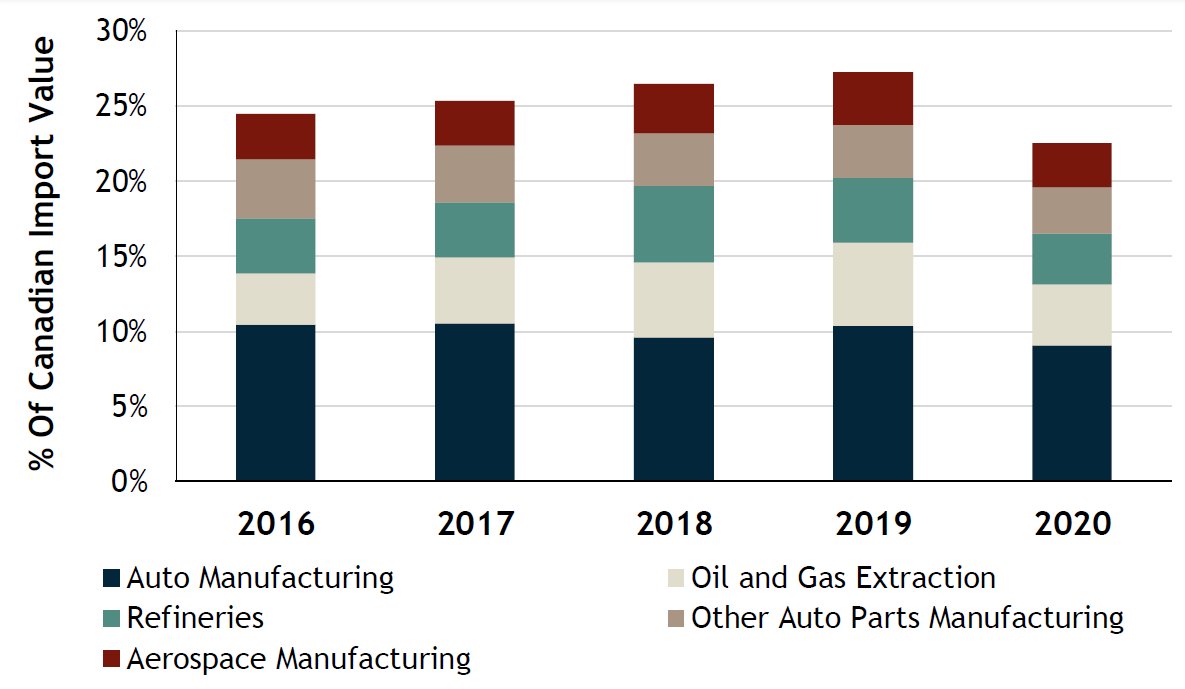

Industries With a Tailwind

In terms of import value from the United States, Canada’s top sectors are much less concentrated than what we saw in export values.

Similar names end up on both lists with the Auto and Aerospace Manufacturing buffering some of the headwinds from the export side of their business. Lenders need to dig into the details to understand the velocity of export versus import business at the borrower level. It’s safe to say that many players in these respective sectors are seeing a decrease in costs associated with imported goods, which likely partially offsets the rise in recent commodity prices.

Tailwinds: Canada’s Top 5 IMPORTING Industries from the United States

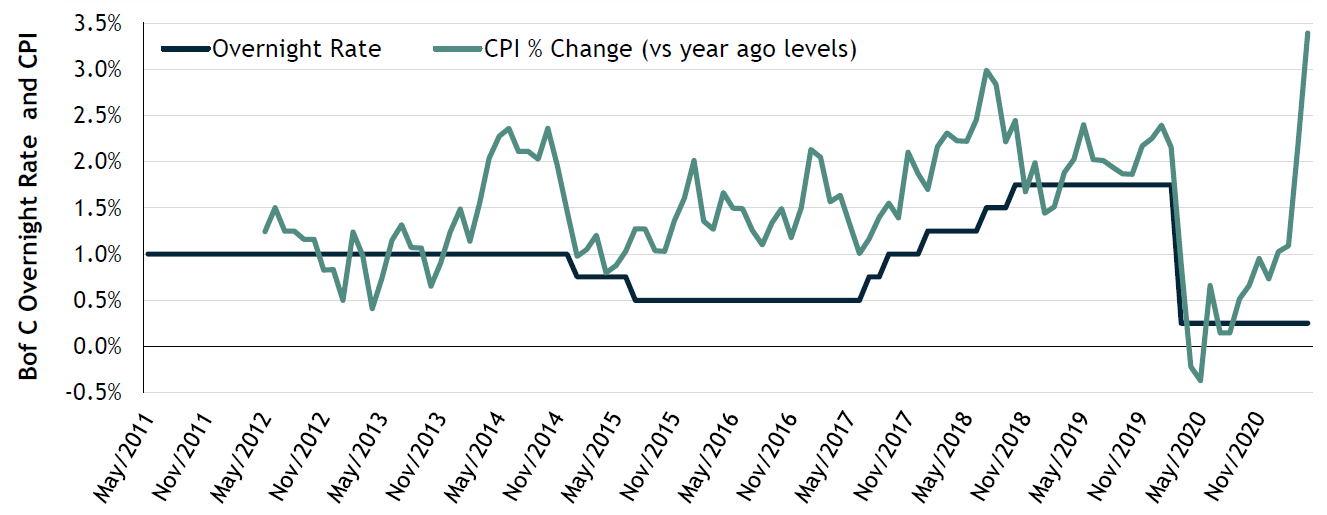

HOW THIS TIES INTO THE INTEREST RATE OUTLOOK

As displayed, a large driver of the relative strength in the Canadian dollar is commodity performance but if we are to think about what is driving the CAD/USD exchange rate beyond this, it tends to fall on central bank messaging. In late April, the Bank of Canada announced adjustments to the quantitative easing program signalling confidence in the economic rebound. This helped push the Canadian dollar through the $0.80 USD mark as the discussion also touched on inflation targets, which the Bank of Canada appears much more sensitive to than the US Federal Reserve. By all measures, it appears the market is indicating the Bank of Canada will increase the overnight rate before the US Federal Reserve.

Why a Stronger Canadian Dollar is Here to Stay:

- Significant underlying support for the commodities and industries that are key drivers of the Canadian dollar.

- Bank of Canada appears to be more focussed on inflation targets than the United States.

- The United States could arguably be trying to use a weaker dollar to stimulate the economy in the near term as they are focused on full employment.

Bank of Canada Overnight Rate and Consumer Price Index

Sources: Bloomberg, Bank of Canada, Capital IQ, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.