September 2023

THE BIG 6 APPEAR TO BE PREPARING FOR GREATER UNCERTAINTY.

Another round of Canadian bank earnings has come and gone and, while results were mixed, the general messaging from the Canadian Big 6 is that they are positioning for future volatility.

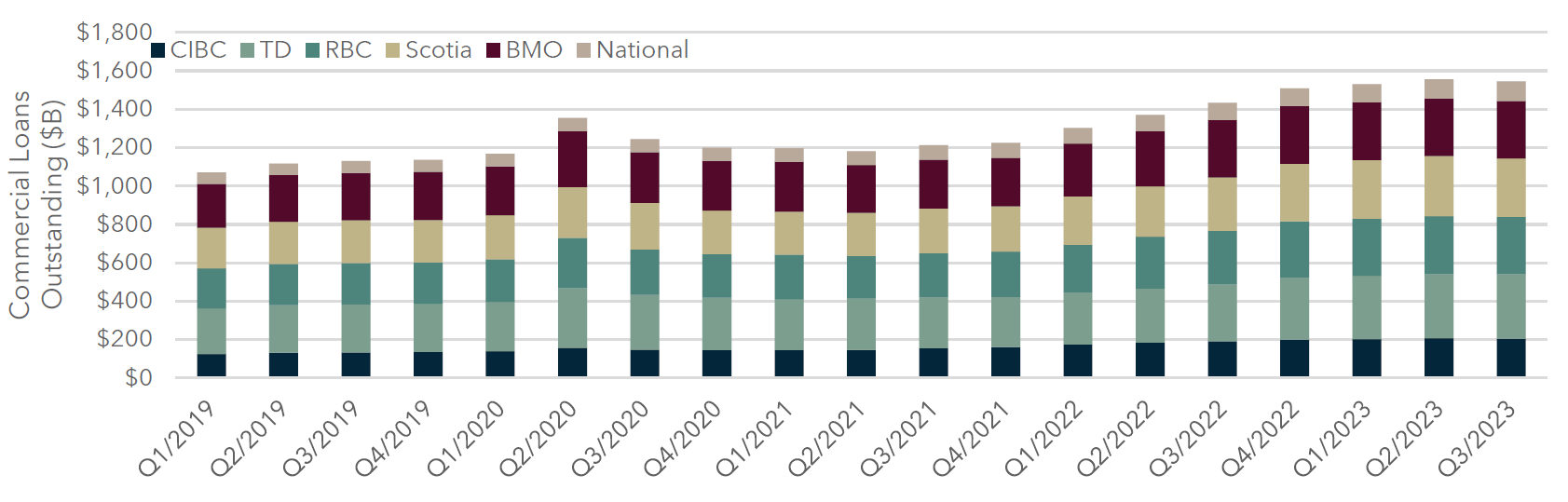

In Q3/2023, the Canadian Big 6 Banks saw total loans outstanding decline on a quarterly basis (-0.7% Q/Q, 7.7% Y/Y) for the first time since Q2/2021. Additionally, there was an acceleration in gross impaired loans (12.1% Q/Q, 42% Y/Y), and a continued increase in credit loan loss provisions (2.2% Q/Q, 129% Y/Y). With economic weakness a primary concern, the reality of higher borrowing costs for borrowers will likely continue to put a strain on commercial loan underwriting. We expect this trend will continue and any borrowers who need more flexible capital are advised to quickly evaluate other lending partners such as the 300 alternative lenders in the DWA network.

KEY TAKEAWAYS THIS MONTH:

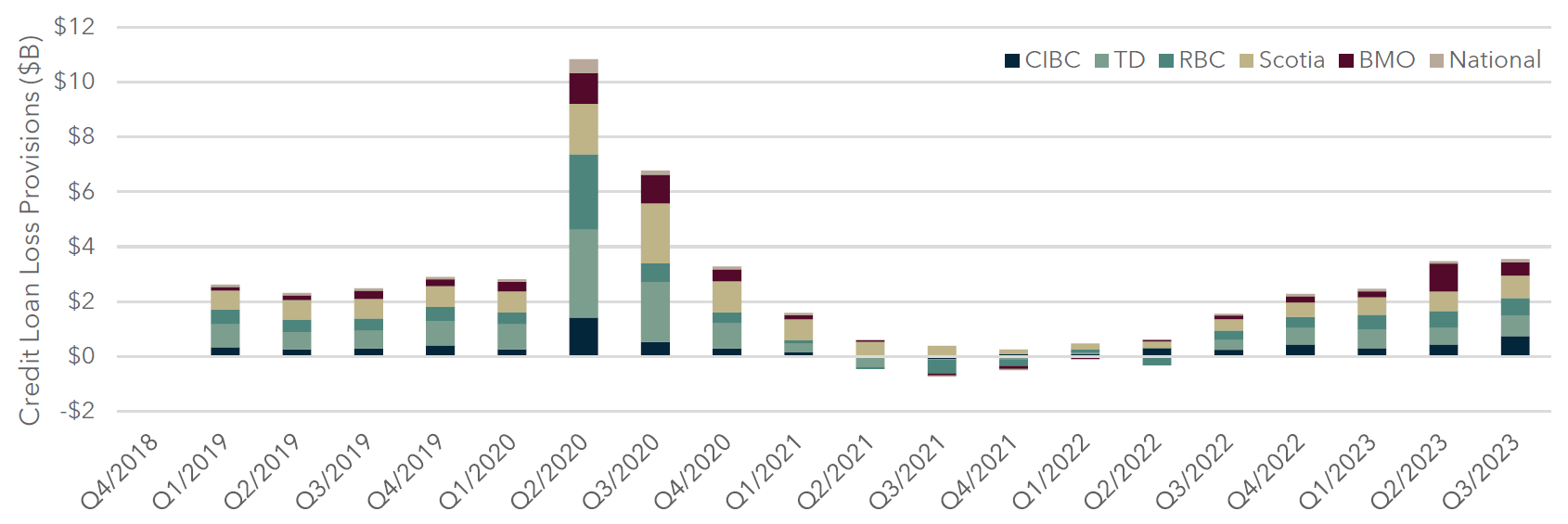

- Bring in the sandbags: A material increase in gross impaired loans (12.1% Q/Q, 42% Y/Y) and credit loan loss provisions (2.2% Q/Q, 129% Y/Y) signals that the Big 6 banks are expecting future borrower weakness and, as a result, credit conditions are likely to tighten. This matches the ‘higher-for-longer’ trend messaging from the Bank of Canada regarding interest rates.

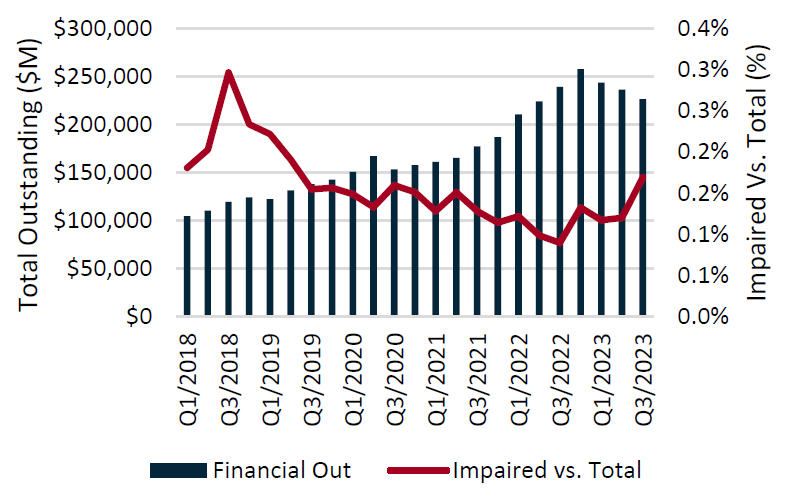

- Loan activity has slowed: Total commercial loans outstanding has slowed on a quarterly basis (-0.7% Q/Q) but continues to expand on an annual basis (7.7% Y/Y). This trend appears to be industry agnostic, apart from Energy which increased 6.6% Q/Q. Financial Services (loans outstanding down 4.2% Q/Q), Manufacturing (loans outstanding down 3.8% Q/Q) and Retail (total loans outstanding down 3.2% Q/Q) were sectors that had the largest impact, as well as largest growth in impaired loans.

Total Commercial Loans Outstanding, Quarterly (Q1/2019 – Q3/2023)

COMMERCIAL LOAN UNDERWRITING SLOWS… ACTUALLY, DECLINES.

Quarter-over-quarter commercial loans outstanding have declined for the first time since Q2/2021 at a rate of -0.7% Q/Q (but have grown 7.7% Y/Y, which is comparable with the historical norm). Most industries, apart from Energy (up 6.6% Q/Q), generally followed this trend – notably, Financial Service commercial loans outstanding have declined 4.2% Q/Q and 5.4% Y/Y. Given the aggressive monetary policy of the Bank of Canada, we expect that this flat/moderate declining trend will continue in the near-term and continue to reflect tight credit conditions.

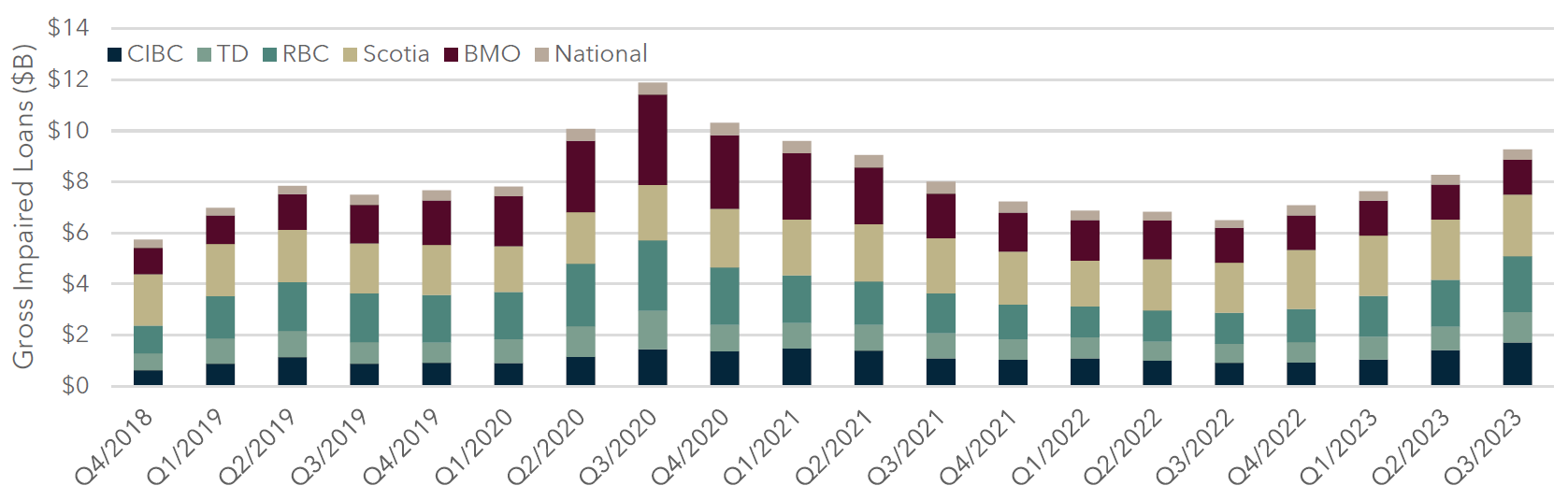

Total Gross Impaired Loans, Quarterly (Q1/2019 – Q3/2023)

GROSS IMPAIRED LOANS CONTINUE TO ACCELERATE.

Gross impaired loans have continued to accelerate in recent quarters (notably increasing 12.1% Q/Q) as credit conditions continue to tighten in response to the Bank of Canada’s aggressive monetary policy. In numerical terms, gross impaired loans increased by $1 billion Q/Q, mostly attributed to industries such as Real Estate (36% Q/Q increase) and Financial Services (35% Q/Q increase). We expect this trend will continue in the near-term before leveling out, similar to the trend experienced in COVID. Notably, gross impaired loans only account for 0.6% of the national commercial loan book, which is well-below COVID and pre-COVID levels, which were 0.8% and 0.7% respectively. This will be a crucial trend to monitor going forward.

Credit Loan Loss Provisions, Quarterly (Q1/2019 – Q3/2023)

LOAN LOSS PROVISIONS UP, BUT DECELERATING.

The Canadian Big 6 Banks appear to continue to be ‘stacking sandbags’ (an old finance proverb) in anticipation that more loans will default in the near-term. On a quarter-over-quarter basis, credit loan loss provisions increased by 2.2% compared to 41% in Q2/2023. Interestingly, this trend occurred in Q4/2022 (47% increase) and Q1/2023 (8% increase), so we are unsure if this is a signal that the Big 6 are adjusting their credit loan loss provisions upwards or more indicative that another large increase will occur. Overall, credit loan loss provisions account for 0.2% of the national loan book, which is in line with the historical pre-COVID level (0.2%). We will continue to monitor this trend going forward.

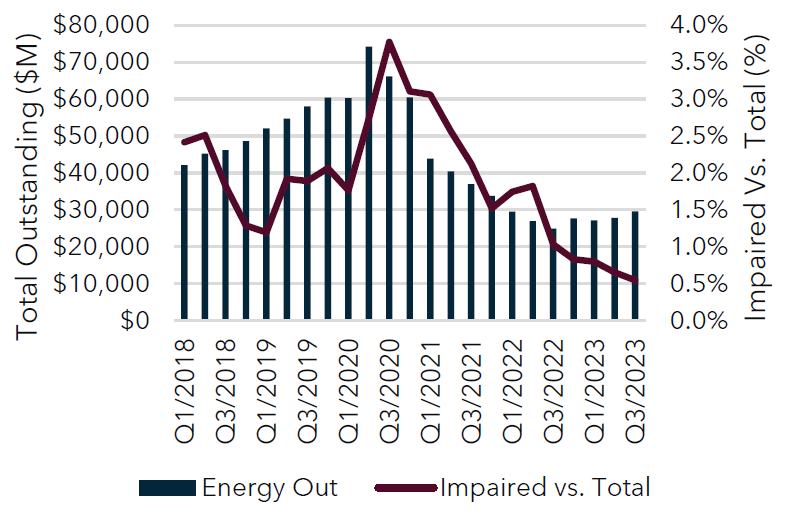

Industry Highlight: Energy

Industry Highlight: Agriculture

OTHER TOPICS WE ARE KEEPING TRACK OF AT DWA.

- Canadian Consumer credit has hit a record high in Q2/2023 at $107.4 billion, while total consumer debt has reached $2.4 trillion according to Equifax.

- JM Smucker Company announced that it will acquire Hostess Brands, the manufacturer of Twinkies, for $5.6 billion.

- Cracks are starting to show in the auto lending business with BMO recently closing its retail auto finance business in Canada. Could this be the next big financial crisis?

Sources: Earnings Reports, Statistics Canada, Bank of Canada, Equifax, Diamond Willow Advisory.

The Debt Digest lands in your inbox each month.